What Is a Moratorium Period? Meaning, Benefits and Examples

Moratorium meaning explained simply: a pause on your EMIs that does not stop your interest. See real examples, benefits, hidden costs, and when to use it.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A moratorium period is a temporary pause on your loan EMI payments, allowed by your lender.

During this period, you do not pay your EMI, but interest usually continues to accrue.

It is not free money. The interest that builds during the moratorium gets added to your outstanding loan.

It is genuinely useful in a financial crisis, but it should not be used casually.

Understanding the full cost of a moratorium before you opt for one can save you from a bigger debt burden later.

What Is a Moratorium Period?

The word moratorium comes from Latin, it means a temporary pause or delay.

In the context of loans, a moratorium period is a specific window of time during which your lender allows you to stop making EMI payments.

You are not asked to pay your monthly instalments during this period.

But and this is the critical part most people do not read carefully- your loan does not go on pause entirely.

Interest keeps accruing. The clock keeps ticking. The money you owe keeps growing quietly in the background.

When the moratorium ends, you resume your EMI payments, but now your outstanding loan amount is higher than it was before.

Think of it like a pause button on your TV. The screen freezes. But electricity is still being used.

A moratorium pauses your payments. It does not pause your debt.

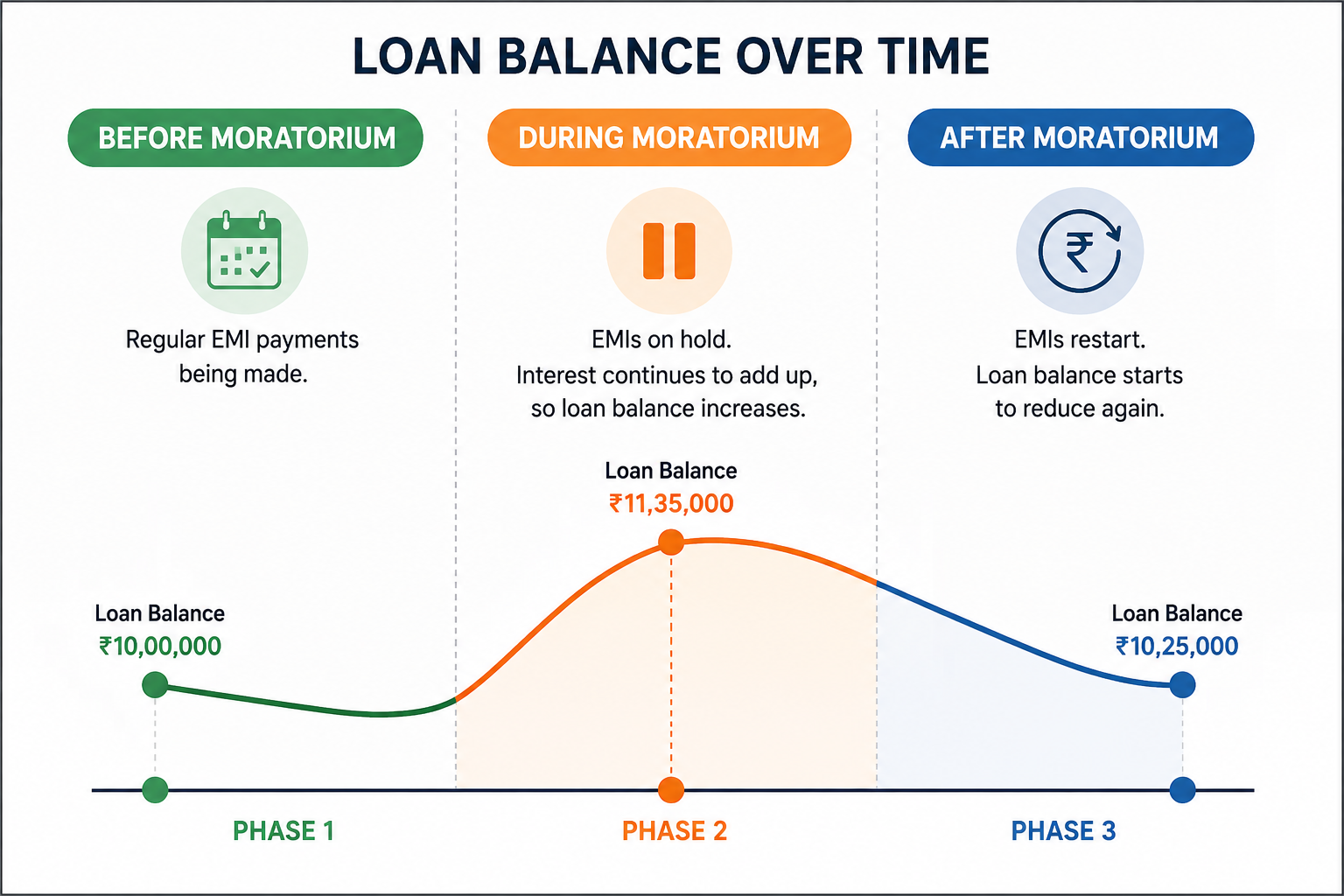

How Does a Moratorium Period Work?

The mechanics are straightforward once you understand the basic structure.

Before the moratorium: You have a loan with a certain outstanding principal. You pay a fixed EMI every month. Each payment reduces your principal slowly.

During the moratorium: Your EMI payment is paused, either fully or partially, depending on the lender's terms. Interest continues to be calculated on your outstanding principal. This interest is not waived. It is either added to your principal or collected later.

After the moratorium: Your EMI payments resume. But because interest was added during the pause, your outstanding balance is now higher. This means either your EMI increases, or your loan tenure extends, or both.

The lender does not lose money during a moratorium. They simply defer when they collect it and, in many cases, they end up collecting more.

FREED Expert Tip

Before accepting a moratorium offer from your lender, always ask one simple question: how much extra will I end up paying in total because of this moratorium? Get the number in writing. If the lender cannot tell you clearly, that is a problem.

Enroll Now

Types of Moratorium Periods in India

Not all moratoriums are the same. Here are the main types you will encounter in India.

- 1

EMI Moratorium on New Loans

Most loans in India come with a built-in moratorium period at the start. Drag Drag When you take a home loan or an education loan, there is often a window at the beginning, sometimes 6 to 24 months, where you are not required to pay the full EMI. Drag Drag This is designed to give borrowers time to set up

- 2

Hardship Moratorium

This is the type most people are searching for. When a borrower is facing genuine financial difficulty like job loss, medical emergency, business failure, they can approach their lender and request a temporary payment pause. The lender evaluates the request and may grant a moratorium of 3 to 12 months, depending on the situation and the lender's policy. This does

- 3

RBI-Mandated Moratorium

During national crises, the RBI has the authority to direct all banks to offer moratoriums to borrowers. The most recent large-scale example was during the COVID-19 pandemic in 2020, when the RBI announced a six-month moratorium for all term loan borrowers. This was available across all categories like home loans, personal loans, vehicle loans, and business loans. These are rare

- 4

Partial Moratorium

Some lenders offer a middle ground; you do not pay the full EMI, but you continue paying the interest portion only This keeps the principal from growing while still giving you some relief on monthly outflow. It is less common, but it is worth asking if you are in a tight spot.

Real Examples to Understand It Better

Numbers make things real. Here are two examples that show how a moratorium actually plays out.

Example 1- Home Loan Moratorium During Construction

Priya takes a home loan of Rs. 30 lakh at 9 percent interest for 20 years.

The property is under construction and will be ready in 12 months.

Her lender offers a 12-month moratorium, no EMIs during construction.

During those 12 months, interest accumulates on the Rs. 30 lakh principal at 9 percent per year.

That is roughly Rs. 2,70,000 in interest added to her outstanding amount.

When construction ends, her outstanding is now Rs. 32,70,000, not Rs. 30 lakh.

Her EMIs are calculated on this higher amount. She pays more each month, and for longer.

The moratorium gave her 12 months of breathing room. But it came with a real cost.

Example 2- Hardship Moratorium After Job Loss

Arun has a personal loan of Rs. 5 lakh at 18 percent interest. His EMI is Rs. 12,700 per month.

He loses his job and cannot make payments. He approaches his bank and is granted a 3-month moratorium.

During those 3 months, interest accrues at 18 percent per annum on Rs. 5 lakh.

That is approximately Rs. 22,500 in interest added to his outstanding amount.

When he resumes payments, his outstanding is now Rs. 5,22,500 instead of Rs. 5 lakh.

His EMI increases slightly, or his tenure extends to cover the additional amount.

The moratorium gave him 3 months to stabilise and find a new job. That was genuinely valuable.

But he knew going in that it was not free. He planned accordingly.

What These Examples Teach Us

A moratorium is a tool. Like any tool, it is useful when used correctly, and costly when misused.

The key is to go in with eyes open, knowing exactly what the moratorium will cost you before you opt for it.

Use This Tool: FREED Debt Calculator Want to know exactly how much a moratorium will add to your total loan cost? Use the FREED Debt Calculator to run the numbers for your specific loan. Free. Takes 2 minutes.

Benefits of a Moratorium Period

When used in the right situation, a moratorium period has genuine, meaningful benefits.

- 1

Immediate Cash Flow Relief

If you are going through a difficult period financially like job loss, a medical emergency, a business slowdown, a moratorium gives you immediate breathing room. The money you would have spent on EMIs can now go toward essentials, rent, food, medical bills, or basic family needs. This is not a small thing. For many families, 3 to 6 months of

- 2

It Does Not Hurt Your Credit Score

This is one of the most important benefits and one that most people do not know about. A moratorium that is officially approved by your lender is not reported as a missed payment. Your credit score is not negatively impacted during the moratorium period as long as it was formally granted by the lender before the due dates passed. This

- 3

It Buys You Time to Recover

Financial setbacks like job loss, illness, and business failure are often temporary. A moratorium gives you a window to recover to find a new job, to heal, to restructure your business without the added pressure of monthly EMI payments bearing down on you.

- 4

It Prevents Default

Default where a borrower stops paying entirely, and the lender marks the account as non-performing is far more damaging than a moratorium. A moratorium, used proactively, can prevent a situation from escalating to default. It keeps the relationship with your lender intact. It keeps your credit record clean. And it gives you a structured path forward.

- 5

It Is Available for Most Loan Types

Home loans, personal loans, vehicle loans, education loans, business loans, most loan types in India have some provision for a moratorium. You are not limited to one category. If you have multiple loans and are struggling, you can approach multiple lenders simultaneously.

The Hidden Costs That Most People Miss

The benefits are real. But so are the costs. And many people opt for a moratorium without fully understanding what it will cost them.

- 1

Interest Does Not Stop

This is the most important thing to understand. Even though your payments pause, your loan continues to accrue interest every single day. Depending on your interest rate and the length of the moratorium, this can add a significant amount to your outstanding balance.

- 2

Your EMI or Tenure Increases

After the moratorium, the accumulated interest has to be recovered somehow. Your EMI goes up, which may be unaffordable given that you were already struggling. Or your loan tenure extends, which means you are in debt for longer and pay more total interest over the life of the loan. Neither option is free.

- 3

It Can Create a False Sense of Relief

Some people use a moratorium as a way to avoid dealing with a deeper financial problem. The debt does not go away. It grows. If you use the moratorium months without taking any steps to improve your financial situation, you will emerge from it in a worse position than you started.

- 4

Compound Interest Can Be Brutal

On high-interest loans, especially personal loans and credit cards, interest compounds quickly. A 6-month moratorium on a high-interest personal loan can add tens of thousands of rupees to your outstanding balance. Always calculate the compound interest impact before opting in. A Simple Cost Comparison

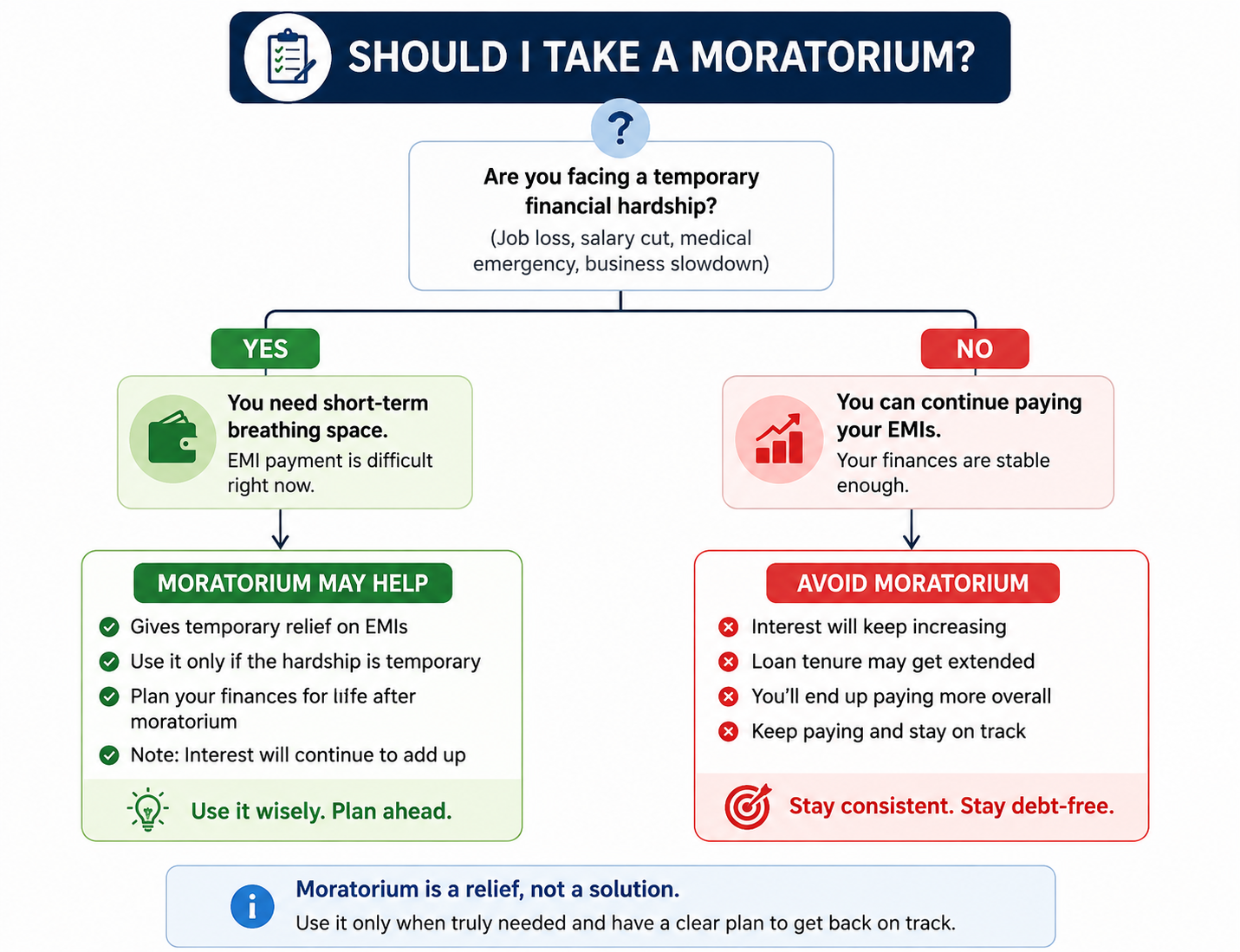

When Should You Use a Moratorium and When Should You Not?

This is the practical question that matters most.

Use a moratorium when:

You have genuinely lost your primary source of income like job loss, business closure, or sudden illness, and have no alternative income to cover EMIs.

You are facing a short-term cash crunch like a medical emergency, but expect your situation to normalise within a few months.

You want to avoid defaulting on a loan and damaging your credit score permanently.

You have a clear plan for how you will manage your finances once the moratorium ends.

You have calculated the full cost of the moratorium and accepted it as a necessary expense.

Do not use a moratorium when:

You can manage your EMIs, even with difficulty. A tight month is not the same as a genuine crisis.

You are hoping the financial problem will somehow resolve itself without any action on your part.

You have not thought about what happens when the moratorium ends and payments resume at a higher level.

You have not explored other options like loan restructuring, EMI reduction, or debt consolidation, which might solve the problem without the added interest cost of a moratorium.

You are planning to take on new loans or credit card spending during the moratorium period.

The Simple Rule

Use a moratorium as a last resort for a genuine, temporary crisis, not as a convenience.

If you are unsure, talk to a financial expert before deciding.

A FREED Expert can look at your situation in detail and tell you whether a moratorium is the right move or whether there is a smarter option available.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions