Key Summary

A loan trap is when your loans keep growing even though you keep paying- because interest and fees are piling up faster than your repayments.

The biggest warning sign is when you take a new loan just to pay off an old one. That is the trap closing in.

A home loan is not automatically a trap- but it can become one if you borrow more than you can actually afford to repay.

Payday loans and instant app loans are among the most dangerous money traps in India right now- their interest rates can go up to 300% per year.

Getting out of a loan trap is possible- with a clear plan, the right help, and no more new loans.

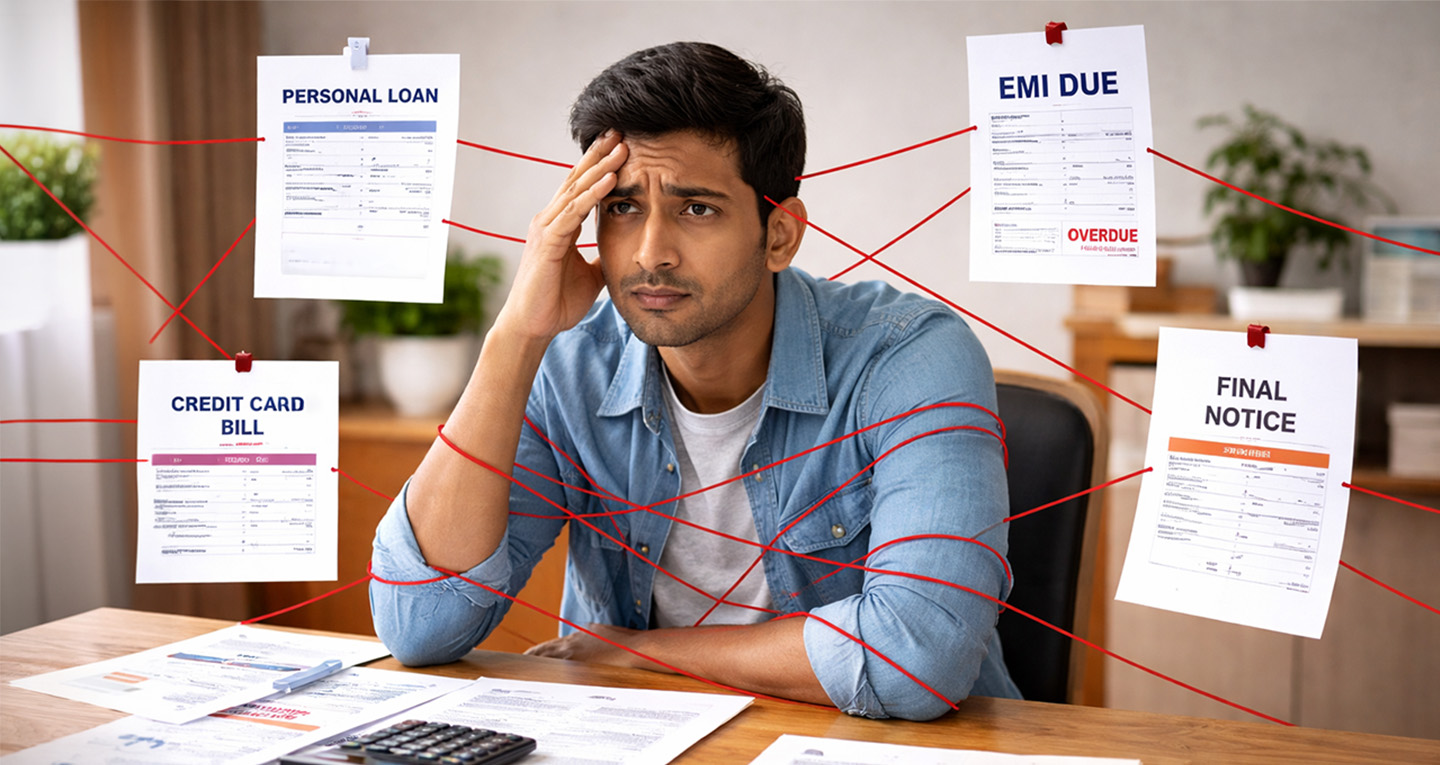

What is a Loan Trap?

A loan trap- also called a debt trap or money trap- is a situation where you keep borrowing money but your total debt never really goes down. You pay your EMI every month. But the interest keeps adding up. Fees pile on top. Before you know it, you owe more than when you started.

The clearest sign of a loan trap? You take a new loan to pay off an old one. That single action is how most people go from one loan to five.

It starts small. A credit card balance you couldn't clear. A personal loan to cover a medical emergency. An app loan to pay rent. Each one seemed necessary at the time. Together, they become a trap that is very hard to climb out of alone.

A loan trap doesn't happen because you are careless with money. It happens because the system is designed to make borrowing feel easy- and repaying feel impossible.

Warning Signs You Are in a Loan Trap

Most people don't realise they're in a loan trap until it's already serious. Here are the signs to watch out for:

1. Your EMIs add up to more than 50% of your monthly salary - If half your income is gone before you even buy groceries- something is wrong.

2. You are only paying the minimum due on your credit card - The minimum due keeps you from defaulting. But it barely touches the actual amount you owe. The rest keeps collecting interest- every single month.

3. You took a new loan to repay an old one - This is the textbook definition of a money trap loan. You are not solving the problem- you are moving it. And adding more interest on top.

4. You are hiding your loan situation from family - When you start avoiding the topic or hiding statements- that's a sign the stress has become serious.

5. Recovery agents are calling you regularly - This means you've already missed payments. The trap has closed. But it's still not too late.

How Do People Get Into a Loan Trap?

Nobody plans to get stuck in debt. But here are the most common ways it happens in India:

Taking loans for lifestyle expenses Buying a phone on EMI. Taking a personal loan for a wedding. Using a credit card for a holiday. These aren't emergencies- but they feel justified in the moment. The repayment pressure, however, is very real.

Borrowing from instant loan apps These apps approve money in minutes with no paperwork. But the interest rates are extremely high- sometimes 30% to 60% per year or more. What looks like quick relief quickly becomes a money trap loan.

Only paying the minimum on credit cards If your credit card bill is ₹50,000 and you only pay the minimum due of ₹2,500- the remaining ₹47,500 collects 3–4% interest every month. That is nearly ₹20,000 in interest per year on a single card.

Multiple small loans from different apps Many people have 5–6 small loans from different apps- ₹5,000 here, ₹10,000 there. Individually they feel manageable. Together, they drain your entire income.

No emergency savings When something unexpected happens- a job loss, a health issue, a family emergency- and there are no savings, the only option feels like another loan. That is how the cycle starts.

Is a Home Loan a Trap?

This is one of the most searched questions in India- and the honest answer is: it depends.

A home loan by itself is not a trap. In fact, it is one of the most structured and regulated types of credit in India. The interest rates are lower. The repayment tenure is longer. And at the end of it, you own an asset.

But a home loan CAN become a trap if:

You borrowed the maximum amount the bank was willing to give- without checking what you can actually afford to repay every month

Your EMI is more than 40% of your take-home salary

You took a personal loan or used credit cards to manage the down payment

Interest rates went up after you took a floating rate loan and your EMI increased significantly

You lost your job or your income dropped after taking the loan

The rule is simple. A home loan is a good debt when it fits your income comfortably. It becomes a trap when you stretch beyond your means to afford it.

What is a Payday Loan Trap?

A payday loan is a very short-term loan- usually meant to last until your next salary. These are typically offered by loan apps, fintech companies, and informal lenders.

They seem harmless. Small amounts. Quick approval. No paperwork. But the interest rates are where the real danger lies.

Here's a real example of how it works:

You borrow ₹5,000 from a loan app. The fee is ₹500 for 30 days. That sounds small. But ₹500 on ₹5,000 for 30 days equals an annual interest rate of around 120%. Some apps charge even more.

If you can't repay on time, the penalties kick in. You borrow again to repay the first loan. Then again. Within a few months, a ₹5,000 loan has become a ₹25,000 problem.

How to spot a payday loan trap before you fall in:

The app promises approval in under 5 minutes with no credit check

The repayment period is less than 30 days

The fees and charges are not clearly shown upfront

The app asks for access to your full contact list or photos

You have already borrowed from 2 or more such apps this month

If any of these apply to you- stop. Do not take another app loan. Speak to a debt counsellor first.

How to Get Out of a Loan Trap

Getting out of a loan trap is not easy. But it is absolutely possible. Here is a step-by-step approach that actually works:

Step 1 - Write Down Everything You Owe List every loan. The lender name, the outstanding amount, the interest rate, and the monthly EMI. Most people are shocked to see the full picture in one place. That clarity is where recovery begins.

Step 2 - Stop Taking Any New Loans Immediately No new credit cards. No new app loans. Not even a small "emergency" loan. Every new loan makes the trap tighter. This is the most important rule.

Step 3 - Talk to Your Lenders Many people avoid their lenders out of fear or shame. But most banks and NBFCs have hardship programs. They can restructure your EMI, give you a repayment holiday, or settle at a reduced amount. You just have to ask- or have someone ask on your behalf.

Step 4 - Prioritise High-Interest Loans First Pay the minimum on all loans. But throw every extra rupee at the loan with the highest interest rate first- usually credit card debt or app loans. Once that's cleared, move to the next one.

Step 5 - Consider a Debt Management Program If you have multiple loans and can't manage them alone, a Debt Management Program (DMP) with a company like FREED puts everything into one structured plan. One payment. Lower interest. A clear end date.

Step 6 - Build Even a Small Emergency Fund Once things start stabilising, save even ₹500–₹1,000 per month in a separate account. This small buffer is what prevents you from falling back into the trap the next time something unexpected happens.

About FREED India

FREED is India's leading platform for debt settlement and financial wellness. We have helped over 60,000 Indians reduce, manage, and get completely out of debt- the right and legal way.

Whether you are dealing with multiple personal loans, credit card debt piling up, recovery agent calls, or an app loan trap- FREED's certified financial counsellors build a plan that fits your exact situation. No hidden charges. No judgment. Just real results.

What we help with: Loan & Debt Settlement · Debt Management Programs · Credit Counselling · Loan Restructuring · CIBIL Score Recovery · Financial Planning

FAQ

Q1. What is a loan trap in simple words?

A loan trap is when you keep taking new loans to pay off old ones- and your total debt never actually reduces. The interest keeps growing faster than you can repay. It's a cycle that gets harder to break the longer it continues.

Q2. What is a money trap loan?

A money trap loan is any loan that looks easy to take but is very hard to repay- usually because the interest rate is very high, the fees are hidden, or the repayment period is too short. Instant app loans and payday loans are the most common money trap loans in India today.

Q3. Is a home loan a trap?

Not by default. A home loan can be a good, structured way to buy a property. But it becomes a trap when you borrow more than your income can handle, or when you use personal loans and credit cards to manage the down payment or extra costs. If your home loan EMI is more than 35–40% of your salary, it's time to re-evaluate.

Q4. How do I know if I'm in a loan trap?

The clearest signs are: your EMIs together add up to more than 50% of your income, you've taken a new loan to repay an old one, you're only paying the minimum due on your credit card every month, and you're getting regular calls from recovery agents. If two or more of these apply to you- you are likely in a loan trap.

Q5. How do I get out of a payday loan trap?

Stop borrowing immediately. Write down every app loan you have. Contact a certified debt counsellor- FREED offers this for free. Do not take another app loan to repay an existing one. In many cases, FREED can negotiate directly with lenders and app companies to reduce what you owe and create a manageable repayment plan.

Q6. Can I get out of a loan trap without affecting my CIBIL score?

It depends on how you exit the trap. Paying off loans fully- even slowly- keeps your score intact or improves it. A debt settlement (paying less than the full amount) will show on your credit report and affect your score for a few years. A debt management program, where you repay fully but in a restructured way, has the least negative impact on your score over time. FREED's counsellors will explain the best option for your situation.

Q7. What happens if I just ignore my loans and stop paying?

Ignoring loans makes things much worse. Your interest and penalties keep growing. Lenders report missed payments to credit bureaus, which damages your CIBIL score. Recovery agents begin calling you and your family. In serious cases, lenders can take legal action. The best thing to do is act early- even if you can't pay the full EMI, talking to your lender or a counsellor makes a big difference.

Q8. Is it legal for loan apps to threaten or harass me?

No. Under RBI guidelines and the Fair Practices Code, no lender- including loan apps- is allowed to threaten, abuse, or harass you during recovery. They cannot contact your family, colleagues, or employer without your permission. If any app is doing this, you can file a complaint with the RBI Ombudsman or your state's consumer court. FREED's team can also guide you through this process.