Understanding Wealth Management: Everything You Should Know

Wealth management" sounds like a phrase reserved for people with private bankers and inherited property. In practice, it describes a set of principles, protecting what you have, growing it deliberately, minimising unnecessary loss, that apply at almost any income level, just at a different scale. Here is what it actually involves, and how to start applying it honestly to your own numbers.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

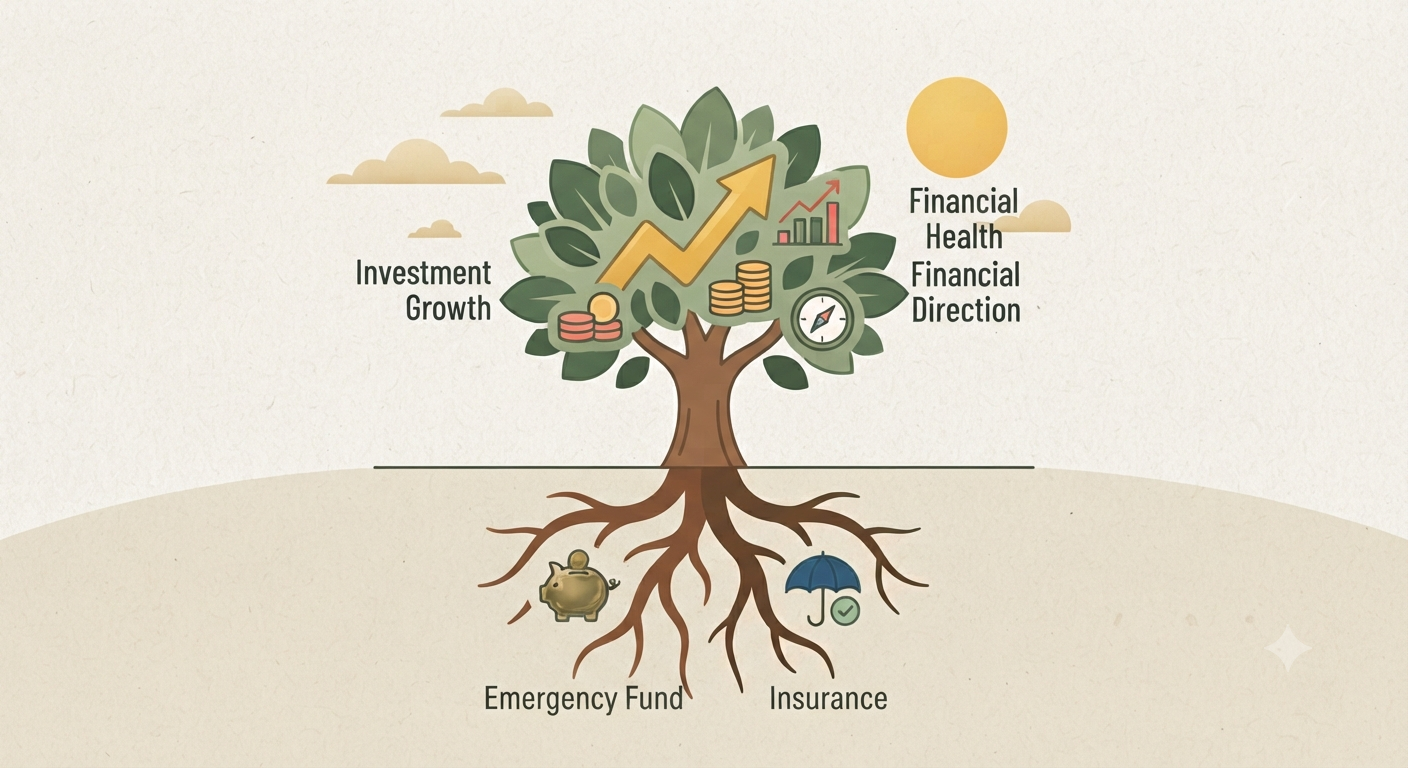

Wealth management is the coordinated management of your full financial position, assets, debts, protection, taxes, and future planning, together, rather than as separate, disconnected decisions.

The core components, an honest current picture, protection through insurance and emergency funds, debt management, goal aligned investing, tax efficiency, and basic estate planning, apply at nearly every income level, not only to high net worth individuals.

A common misconception is that wealth management requires a large portfolio to begin. In reality, the principles matter most early, when small, consistent decisions have the most time to compound.

Existing high interest debt is one of the few factors capable of undermining every other component of a wealth management plan simultaneously, which is why it deserves specific, early priority.

If debt is the reason a coordinated wealth management approach feels out of reach, FREED can help address that obstacle directly, creating the foundation the other components actually need to function.

Why "Wealth Management" Sounds More Exclusive Than It Actually Is

The phrase "wealth management" is most commonly associated with private banking services, dedicated relationship managers, and minimum portfolio sizes that put it firmly out of reach for most people. This association is not entirely wrong, formal, dedicated wealth management services do typically require a certain asset threshold to access.

But the underlying principles that these services apply on behalf of wealthy clients, an integrated view of assets and debts, protection against risk, tax efficient decisions, goal aligned investing, are not exclusive to any income bracket. They are simply principles that a formal advisor applies on your behalf if you can afford one, and that you can apply yourself, with somewhat more personal effort, at nearly any financial stage.

Understanding wealth management this way, as a set of principles rather than a service tier, is what makes it genuinely useful to someone building their first emergency fund, not only to someone managing an inherited property portfolio.

Want to build a coordinated financial plan around your specific situation?

Talk to a FREED Expert for free.

Connect with FREED ExpertWhat Wealth Management Actually Means

At its core, wealth management is the practice of managing your full financial picture, assets, debts, income, protection needs, and future goals, together, in a coordinated way, rather than making each financial decision in isolation without reference to the others.

A person who invests aggressively while ignoring high interest debt, or who buys insurance without any sense of their actual protection needs, or who saves diligently without any tax awareness, is making individually reasonable decisions that are not actually coordinated with each other. Wealth management is specifically the discipline of ensuring these decisions work together, rather than working against or independently of one another.

This coordination is valuable regardless of the actual amounts involved, a modest income managed with this coordinated approach generally produces a stronger financial outcome over time than a considerably higher income managed as a series of disconnected decisions.

Component 1: A Clear Picture of Your Current Financial Position

Every wealth management approach, formal or self-directed, begins with an honest, complete accounting of where things currently stand, every asset, savings, investments, property, and every liability, credit cards, loans, any other debt, listed with actual current figures.

Subtracting total liabilities from total assets gives your net worth, a single number that, tracked over time rather than calculated once, becomes one of the most useful indicators of whether your overall financial position is genuinely improving or quietly deteriorating, regardless of how any single account or investment happens to be performing in isolation.

This first component is foundational specifically because every other component depends on it, protection needs, investment decisions, and debt priorities are all calculated relative to this actual, current starting point, not to an estimate or a rough impression of where things stand.

Component 2: Protection Before Growth

A coordinated wealth management approach places protection, an emergency fund and adequate insurance, ahead of aggressive growth, even though growth often feels like the more exciting, more discussed part of managing wealth.

An emergency fund of three to six months of essential expenses, and adequate health insurance in particular, exist specifically to prevent a single disruptive event, a medical emergency, a job loss, from undoing months or years of careful, coordinated progress on every other component. Without this protection layer in place first, every other part of the wealth management picture remains vulnerable to being undone by a single, foreseeable category of event.

This sequencing, protection before growth, is not a conservative preference, it is a structural requirement, since an investment portfolio, however well chosen, provides little benefit if a large share of it needs to be liquidated at a bad time to cover an emergency that a modest cash reserve could have absorbed instead.

Component 3: Debt Management as Part of the Wealth Picture, Not Separate From It

A specific mistake in less coordinated financial approaches is treating debt as a separate problem, to be managed independently, rather than as a direct, active component of the overall wealth picture.

High interest debt, particularly credit cards at 36 to 42% per year, functions as a negative asset that grows faster than nearly any investment can offset, meaning it actively works against every other wealth building component simultaneously. A genuinely coordinated approach treats paying down this specific category of debt as itself a wealth building action, arguably one of the highest return actions available, rather than a separate obligation sitting outside the broader wealth strategy.

Lower cost, longer term debt, a reasonable home loan, for instance, is treated differently within this framework, understood as a structural part of the overall balance sheet rather than something to be eliminated at all costs ahead of every other goal.

Not sure how your existing debt fits into a broader financial plan?

Talk to a FREED Expert for free.

Talk to a FREED ExpertComponent 4: Structured Investing Aligned to Specific Goals

Once protection is in place and high interest debt is being actively addressed, investing becomes the component most people associate with "wealth management" specifically, though it is only one part of the fuller picture.

A coordinated approach ties each specific investment choice to a specific goal and its timeline, retirement contributions structured for growth over decades, a medium term goal like a home down payment structured more conservatively as its target date approaches, rather than applying one single investment approach uniformly across every goal regardless of when the money will actually be needed.

This alignment, matching investment risk and vehicle to the specific timeline of each goal, is a core wealth management principle precisely because a mismatch, aggressive investments for a near term goal, or overly conservative savings for a genuinely long term one, is one of the most common and costly errors even among people who are otherwise disciplined savers.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Component 5: Tax Efficiency Woven Into Every Decision

A coordinated wealth management approach considers the tax implications of financial decisions as they are made, rather than treating tax planning as a separate, once a year task disconnected from ongoing saving and investing decisions.

This includes using tax advantaged investment and savings instruments where appropriate for your specific goals and income level, understanding the tax treatment of different investment types before choosing between them, and timing certain financial decisions, when reasonable and appropriate, around tax considerations rather than incidentally.

Tax efficiency compounds over time in the same way investment returns do, a modest, consistent tax saving applied every year across a working lifetime represents a meaningful cumulative difference, even though any single year's saving may look unremarkable in isolation.

Component 6: Estate and Succession Planning, Even at a Modest Scale

Estate planning, deciding how assets will be distributed and managed in the event of death or incapacity, is often assumed to be relevant only to those with substantial property or wealth to pass on. In practice, a basic version of this planning is worthwhile at nearly any asset level.

A simple, updated nomination on every bank account, insurance policy, and investment, and a basic will reflecting your actual current wishes, however modest your current assets, prevents a specific, genuinely difficult situation for family members, unclear or contested access to accounts and assets during an already difficult period, that has nothing to do with the actual size of the estate involved.

This component is frequently the most neglected specifically because it deals with an uncomfortable topic, mortality, rather than because it genuinely requires substantial wealth to be worth addressing.

Component 7: Ongoing Review and Rebalancing

A wealth management approach is not a plan created once and left untouched. It requires periodic review, generally every six to twelve months, checking whether your net worth is trending in the right direction, whether protection levels remain adequate given any life changes, whether debt repayment is on track, and whether investments still align with each goal's updated timeline.

This review is also the point at which rebalancing happens, adjusting the specific mix of investments, savings, and debt repayment as circumstances change, income growth, a new dependent, a changed goal timeline, rather than allowing the original plan to drift silently out of relevance as life circumstances evolve around it.

Who Actually Needs Formal Wealth Management vs Who Can Self-Manage

Formal wealth management services, a dedicated advisor coordinating all seven components on your behalf, generally become genuinely valuable once your financial situation reaches a certain complexity, multiple income sources, significant investments across different asset classes, business ownership, or specific tax and estate complexity that benefits from professional expertise.

For many people, particularly earlier in their financial life, applying these same seven components independently, with periodic professional input for specific decisions, tax filing, insurance selection, is genuinely sufficient and considerably more cost effective than a formal advisory relationship, which typically charges a fee based on assets managed.

The principles in this blog are designed to be applied at either stage, whether you are working independently through each component yourself, or eventually working alongside a formal advisor once your situation's complexity genuinely warrants it.

What the Law Says

Under SEBI regulations, any entity offering formal investment advisory services in India is required to be a registered investment advisor, and must disclose their fee structure and any potential conflicts of interest clearly before providing advice. If you are considering formal wealth management services, confirming this registration directly is a reasonable, specific step before committing to any advisory relationship or fee arrangement.

Check My Credit Score FreeCommon Misconceptions About Wealth Management

A few specific misconceptions are worth addressing directly, since they prevent many people from applying these useful principles simply because the framing feels inapplicable to their situation.

"Wealth management is only for the wealthy" confuses a service tier with an underlying set of principles that apply at any asset level. "It is mainly about investing" understates the role of protection, debt management, and estate planning, each of which matters as much as, and sometimes more than, the investment component specifically. "It requires a large amount of money to be worth doing" overlooks that the earliest years of applying these principles, even with modest amounts, benefit the most from the additional time available for compounding and habit formation.

Curious whether a coordinated approach could help your specific situation?

Talk to a FREED Expert for free.

Talk to a FREED ExpertBuilding a Simple Wealth Management Framework at Any Income Level

Applying these seven components independently does not require sophisticated tools or a large starting portfolio. Begin with an honest net worth calculation, then build a starter emergency fund and confirm basic insurance coverage. Address any high interest debt directly and specifically, treating it as a wealth priority rather than a separate problem. Structure any existing or new savings and investments around specific, timed goals rather than a single undifferentiated pool. Stay aware of tax efficient options relevant to your income level. Update account nominations and consider a basic will regardless of current asset size. And commit to a review every six to twelve months to keep the whole picture current.

This framework, applied consistently, is the practical, self-directed version of what a formal wealth manager does on behalf of a client with a considerably larger portfolio, the scale differs, the underlying discipline does not.

When Debt Undermines the Entire Wealth Management Picture

Every component described above assumes a starting position where, after essential expenses, some genuine capacity exists to build protection, address debt, and invest towards goals simultaneously, even if modestly at first.

For some people, existing high interest debt is large enough that it consumes the entirety of this capacity, leaving no meaningful room for an emergency fund, insurance premiums, or any investment contribution, regardless of how well the other six components are understood in principle. In this situation, no amount of careful planning across the other components will produce genuine progress until this specific obstacle is addressed directly.

FREED's Debt Consolidation Program combines multiple high interest debts into one lower interest loan with a single, manageable EMI, freeing up the monthly capacity that the rest of a coordinated wealth management approach actually depends on.

FREED's Debt Resolution Program negotiates a reduced settlement for debt that cannot realistically be repaid in full, on average 56% less than the original outstanding, removing the obstacle rather than requiring the rest of the plan to work around it indefinitely.

A free consultation can assess your specific situation honestly and identify whether existing debt is the reason a coordinated approach has felt out of reach so far.

Want an honest starting point before building out your own wealth management framework?

Take the FREED Financial Health Score, free, 2 minutes.

Check My Financial Health ScoreFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions