The Real Difference Between Savings and Investments

Savings and investments are often used interchangeably, but they serve fundamentally different purposes. Here is the real, practical difference between the two, when to use each, and the mistake of confusing one for the other.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Savings and investments are often used as interchangeable terms in everyday conversation, but they serve fundamentally different financial purposes, and treating them the same way leads to specific, avoidable mistakes.

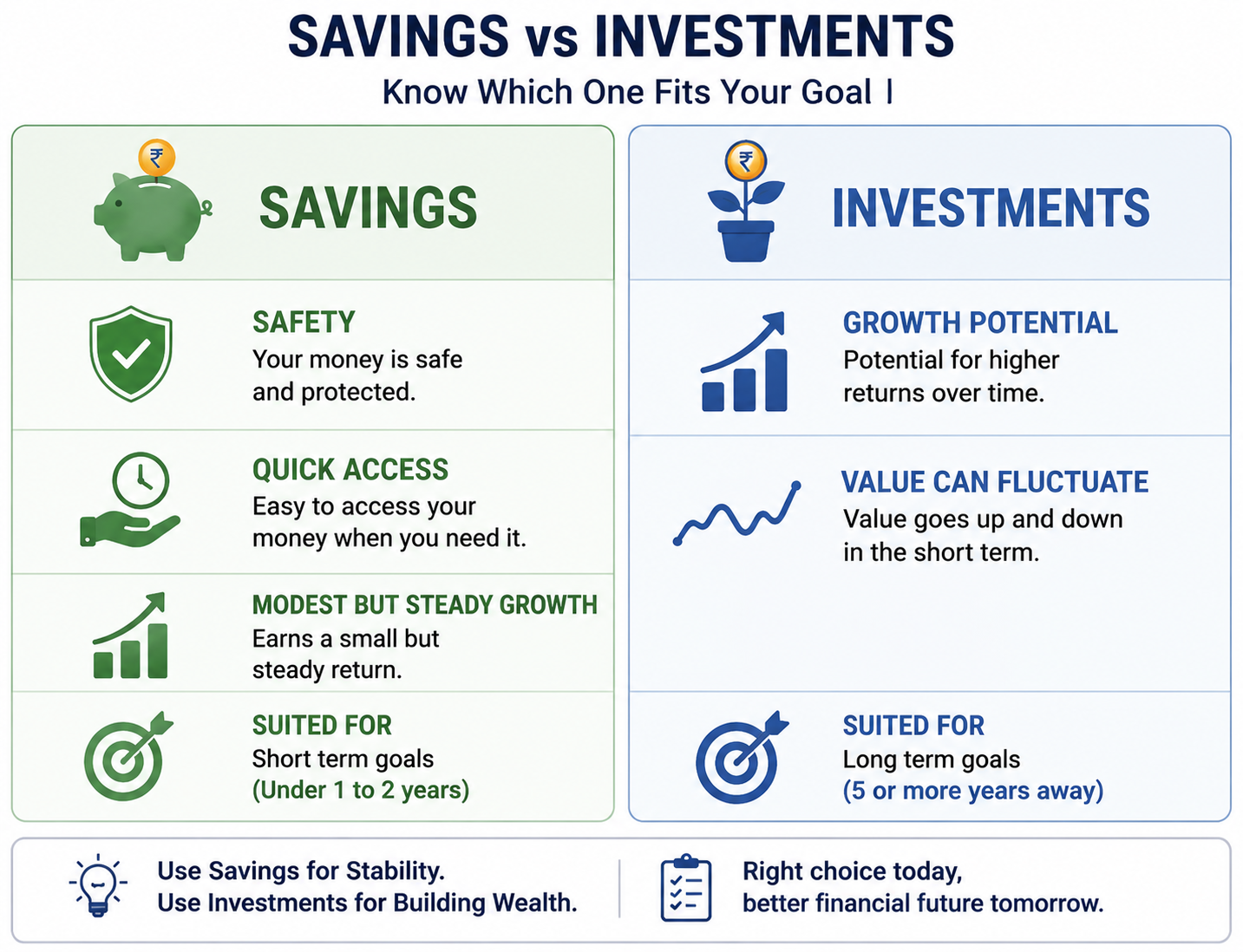

Savings prioritise safety and immediate access, and are meant for money you may need on short notice. Investments prioritise growth over time, and are meant for money you will not need for several years.

The most common mistake in one direction is using investments for an emergency fund, risking a forced withdrawal at a bad time. The most common mistake in the other direction is leaving long term money sitting in low interest savings for years, losing significant growth to inflation.

The right question for any specific goal is not "should I save or invest," but "what is the time horizon and risk tolerance for this specific money," which determines the answer directly.

Before either saving meaningfully or investing aggressively, high interest debt deserves priority, since it actively works against both, and FREED can help address it directly if it is standing in the way.

Why This Distinction Gets Confused So Often

In everyday conversation, "saving for a house" and "investing for a house" are frequently used to mean the same general idea, setting money aside now for a future goal. This casual overlap in language is understandable, but it obscures a distinction that has real, practical financial consequences.

Savings and investments are not simply two labels for the same underlying activity. They are two genuinely different financial tools, built around different priorities, safety and access for one, growth over time for the other, and suited to different kinds of goals depending on when the money will actually be needed and how much risk is appropriate for that specific purpose.

Confusing the two in either direction has a real cost. Using an investment account for money that might be needed next month risks having to withdraw it at a bad time, potentially at a loss. Using a savings account for money that will not be needed for fifteen years means missing out on years of growth that could have meaningfully changed the eventual outcome.

What Savings Actually Means

Savings refers to money set aside in a safe, easily accessible form, typically a savings account, a fixed deposit, or a similarly low risk instrument, specifically to preserve its value and remain available on short notice.

The defining features of savings are safety and liquidity. A savings account does not meaningfully lose value due to market movement, the amount deposited, plus modest interest, remains available essentially as deposited. And it can typically be accessed within a day or two, sometimes instantly, without penalty or a waiting period.

Savings are the right tool for money with a short time horizon, an emergency fund, a specific upcoming expense within the next year or two, or any amount where the priority is certainty that the money will be there, in full, exactly when it is needed, rather than the possibility of it growing significantly in the meantime.

What Investments Actually Mean

Investments refer to money placed into instruments, equity, mutual funds, bonds, real estate, that carry the potential for growth over time, but also carry a real possibility of the value fluctuating, including declining, particularly over shorter periods.

The defining features of investments are growth potential and risk. Over a sufficiently long period, historically, well diversified investments have generally outpaced the returns available from savings accounts by a significant margin. But this growth is not steady or guaranteed in the short term, the same investment that grows significantly over ten years may show a meaningful decline in any given six month or one year window.

Investments are the right tool for money with a longer time horizon, retirement savings, a child's education fund many years away, long term wealth building, where there is enough time for short term fluctuations to even out, and where the goal benefits meaningfully from growth that a savings account simply cannot provide.

The Core Difference: Purpose, Not Just Product

The most useful way to understand the difference between savings and investments is not by the specific product involved, a fixed deposit versus a mutual fund, but by the purpose the money is serving for you, right now, in your specific financial plan.

The same amount of money can, in principle, be placed into either a savings account or an investment product. What determines which is actually appropriate is not the product itself, but the question behind it: when will this money genuinely be needed, and what happens if its value is lower than expected at that specific moment.

If the money is needed soon, or if a lower than expected value at the moment of need would create real hardship, an emergency fund, a wedding six months away, this points clearly towards savings, regardless of how attractive an investment's potential returns might look. If the money will not be needed for many years, and short term fluctuation would have time to even out before it is actually needed, this points towards investments.

Risk: The Factor That Separates Them Most Clearly

Risk, specifically the risk that the money will be worth less than expected at a given point in time, is the single clearest factor separating savings from investments, and it deserves to be understood specifically, not just acknowledged in the abstract.

Savings carry minimal risk to the deposited amount itself. A rupee placed in a savings account today will still be a rupee, plus modest interest, next year. The risk with savings is different, and often overlooked: inflation risk, the possibility that the purchasing power of that money, what it can actually buy, declines over time even as the nominal amount stays the same or grows slightly.

Investments carry direct value risk, the amount itself can genuinely decline, sometimes significantly, over shorter periods, though historically it has tended to recover and grow over longer ones. This is not a flaw in investments, it is the specific mechanism by which they offer higher potential growth than savings, in exchange for accepting this shorter term uncertainty.

Neither type of risk is inherently better or worse. What matters is matching the type of risk you are willing to accept, and can genuinely afford to accept, to the specific time horizon of the money in question.

Liquidity: How Quickly You Can Actually Access the Money

Liquidity, how quickly and easily money can be converted back to cash without loss or penalty, is a second key distinction, and one that becomes critically important specifically in an emergency.

Savings accounts offer high liquidity, funds are typically accessible within a day, often instantly, with no penalty for withdrawal. This is precisely what makes savings suitable for an emergency fund, the defining feature of an emergency is that it is unplanned, and the money needs to be accessible immediately, not after a waiting period or at a potentially unfavourable moment in a market cycle.

Investments generally offer lower liquidity in a practical sense, even when technically possible to withdraw quickly, doing so during a market downturn means realising a loss that would not have occurred if the money could have remained invested longer. This is the specific danger of using investments for money that might be needed on short notice, the withdrawal itself may be technically possible, but the timing may be genuinely costly.

Time Horizon: Why the Same Goal Should Not Use Both Interchangeably

Time horizon, how many years remain before the money will actually be needed, is the practical factor that ties risk and liquidity together into a specific, actionable decision for any given goal.

For goals under 1 to 2 years away, an emergency fund, a planned expense, a short term goal, savings are almost always the appropriate choice, since there is not enough time for market fluctuations to reliably even out, and the priority is certainty over growth.

For goals 5 or more years away, retirement, a child's long term education fund, long term wealth building, investments are generally more appropriate, since there is sufficient time for short term fluctuations to average out, and the growth potential meaningfully outweighs the short term risk over that longer window.

For goals in between, 2 to 5 years, a more conservative, blended approach is often appropriate, weighted more towards capital preservation as the goal date approaches, since there is some time for growth but not necessarily enough to fully absorb a significant downturn right before the money is needed.

FREED Expert Tip

A useful practical rule: as any specific goal's target date gets within 12 to 18 months, gradually shift the money associated with that goal from investments into savings or similarly stable instruments, regardless of how the investment has performed up to that point. A goal that reaches its final year with funds still fully exposed to market risk is a goal that can fail at exactly the wrong moment, right when the money is actually needed.

Talk to FREEDCommon Mistake 1: Treating Investments as a Substitute for an Emergency Fund

A specific, consequential mistake is deciding to skip a dedicated emergency fund and instead relying on being able to withdraw from investments if an emergency arises, reasoning that this avoids the "opportunity cost" of money sitting in a low interest savings account.

This reasoning breaks down at the moment it is actually tested. Emergencies do not arrive on a schedule convenient to market conditions, an unplanned expense arriving during a market downturn means either withdrawing at a loss, realising a decline that would likely have recovered given more time, or being unable to access the needed amount at all if the investment is in a form with withdrawal restrictions or penalties.

A dedicated, separate emergency fund in savings, even if it earns a comparatively modest return, exists specifically to remove this risk. It is not a suboptimal use of money, it is the correct tool for a specific job that investments are not well suited to perform.

Common Mistake 2: Leaving Long Term Money Sitting in Savings for Years

The opposite and equally costly mistake is leaving money intended for a genuinely long term goal, retirement, a child's education many years away, sitting in a savings account for years, out of caution or a simple failure to move it into a more appropriate long term instrument.

Because savings prioritise safety over growth, the return offered is typically modest, often not meaningfully outpacing inflation over long periods. Money left in savings for a genuinely long term goal is not being protected in a meaningful sense, it is quietly losing purchasing power relative to what a longer term, growth oriented instrument would likely have achieved over the same period.

The cost of this mistake compounds specifically because of the length of time involved, a long term goal funded through savings rather than investments over fifteen or twenty years can result in a significantly smaller final outcome than the same contributions would have produced through appropriately invested growth over the same period.

How to Decide Which One a Specific Goal Actually Needs

For any specific financial goal, three questions determine whether savings or investments are the more appropriate tool.

When will this money actually be needed. Under 2 years points towards savings. Over 5 years points towards investments. In between calls for a more conservative, blended approach weighted increasingly towards savings as the date approaches.

What happens if the value is lower than expected right when the money is needed. If this would create genuine hardship, an emergency, an already committed expense, savings are the safer choice, regardless of the time horizon otherwise.

Is there sufficient time for short term fluctuation to reasonably even out before the money is needed. If yes, investments become appropriate. If no, savings remain the better fit, even if the goal itself is not urgent.

Applying these three questions specifically to each individual goal, rather than adopting a single, blanket approach across all financial goals at once, is what allows savings and investments to actually serve their distinct, complementary purposes.

What the Law Says

Under SEBI and RBI investor protection guidelines, financial institutions offering investment products are required to clearly disclose the risk profile of any product, including the possibility of loss, before a person commits funds. Savings products, including fixed deposits, are separately covered under deposit insurance up to a specified limit through the Deposit Insurance and Credit Guarantee Corporation, providing a further layer of protection specific to savings that investment products generally do not carry. Understanding which category of protection applies to a specific instrument is worth confirming directly with the institution before committing funds.

Talk to FREEDWhere Debt Fits Into This Picture

Any discussion of savings and investments is incomplete without addressing where high interest debt fits into the decision, since it changes the calculation directly.

Credit card debt at 36 to 42% per year outpaces the realistic return of almost any investment, and significantly outpaces the return of any savings instrument. This means that, for most people carrying this kind of high interest debt, paying it down is a more effective use of money than either saving aggressively or investing, since the "return" on debt repayment, the interest avoided, is higher and more certain than either alternative.

The practical sequencing that works well for most people: build a small starter emergency fund in savings first, address any high interest debt next, since it actively works against progress on every other goal, then build savings and investments in parallel according to the time horizons of specific goals, once the highest cost obstacle has been removed.

If high interest debt is currently large enough that it is preventing meaningful progress on either savings or investments, addressing it directly is usually the more effective next step, ahead of optimising the split between the other two.

How FREED Can Help

If existing debt is the reason meaningful savings or investing feels out of reach, regardless of how well the distinction between the two is understood, FREED can help address that underlying obstacle directly.

FREED's Debt Consolidation Program combines multiple high interest debts into one lower interest loan with a single, manageable EMI, freeing up monthly income that can then be directed towards savings and investments according to the goals in this blog.

FREED's Debt Resolution Program negotiates a reduced settlement for debt that cannot realistically be repaid in full, on average 56% less than the original outstanding, removing the obstacle rather than just reducing it.

A free consultation can assess your specific situation and tell you honestly whether your current debt load is standing in the way of building the kind of savings and investment plan outlined here.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions