The Do’s and Don’ts of Personal Finance: What Actually Works

Learn what truly works in personal finance and what silently wrecks your money game. Discover smart tips for budgeting, investing, debt management, and more.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Much personal finance advice fails not because it is wrong, but because it is generic, offered without regard for the specific financial situation it is being applied to.

The "dos" that consistently work share a common thread: they remove reliance on willpower and daily decision making, tracking, automating, and building a buffer before the next crisis, not during it.

The "don'ts" that consistently cause harm share a common thread: they treat available credit or comparison to others as a substitute for an actual financial plan.

High interest debt is treated separately from general advice because its cost, 36 to 42% per year on credit cards, outweighs the benefit of nearly any other financial action taken before it is addressed.

If the basics outlined here are not enough because existing debt is already too large to manage through better habits alone, FREED can help address it directly.

Why So Much Personal Finance Advice Fails in Practice

Search for personal finance advice and the volume is overwhelming, articles, videos, social media posts, each offering a version of the same handful of tips, often contradicting each other, or offering a rule so general that it fails to account for anyone's actual situation.

Some of this advice is simply wrong. Much of it is not wrong, exactly, but generic to the point of being unhelpful, "spend less than you earn" is true, but offers no specific guidance to someone trying to figure out which of their specific monthly expenses to actually change.

The list below is built differently. Each item reflects a pattern that consistently shows up, across income levels and situations, as either genuinely helpful or genuinely harmful, based on what FREED sees across a large number of real financial situations, not based on a generic rule that sounds correct in the abstract.

Do: Track Where Your Money Actually Goes, Before Trying to Change It

Most attempts to improve personal finances begin with a decision to spend less, without first understanding where the money currently goes. This usually fails, because the areas that feel like they need cutting are rarely the areas actually consuming the most money.

Track every expense, honestly and completely, for one full month, before making any changes. Most people discover at least one or two categories consuming significantly more than expected, often something that did not feel significant in the moment, several small food delivery orders, a handful of unused subscriptions, frequent small cab rides.

This single month of honest tracking, done before attempting to change anything, consistently produces more useful, targeted change than months of vague intention to "spend less" without ever knowing specifically where the money was going.

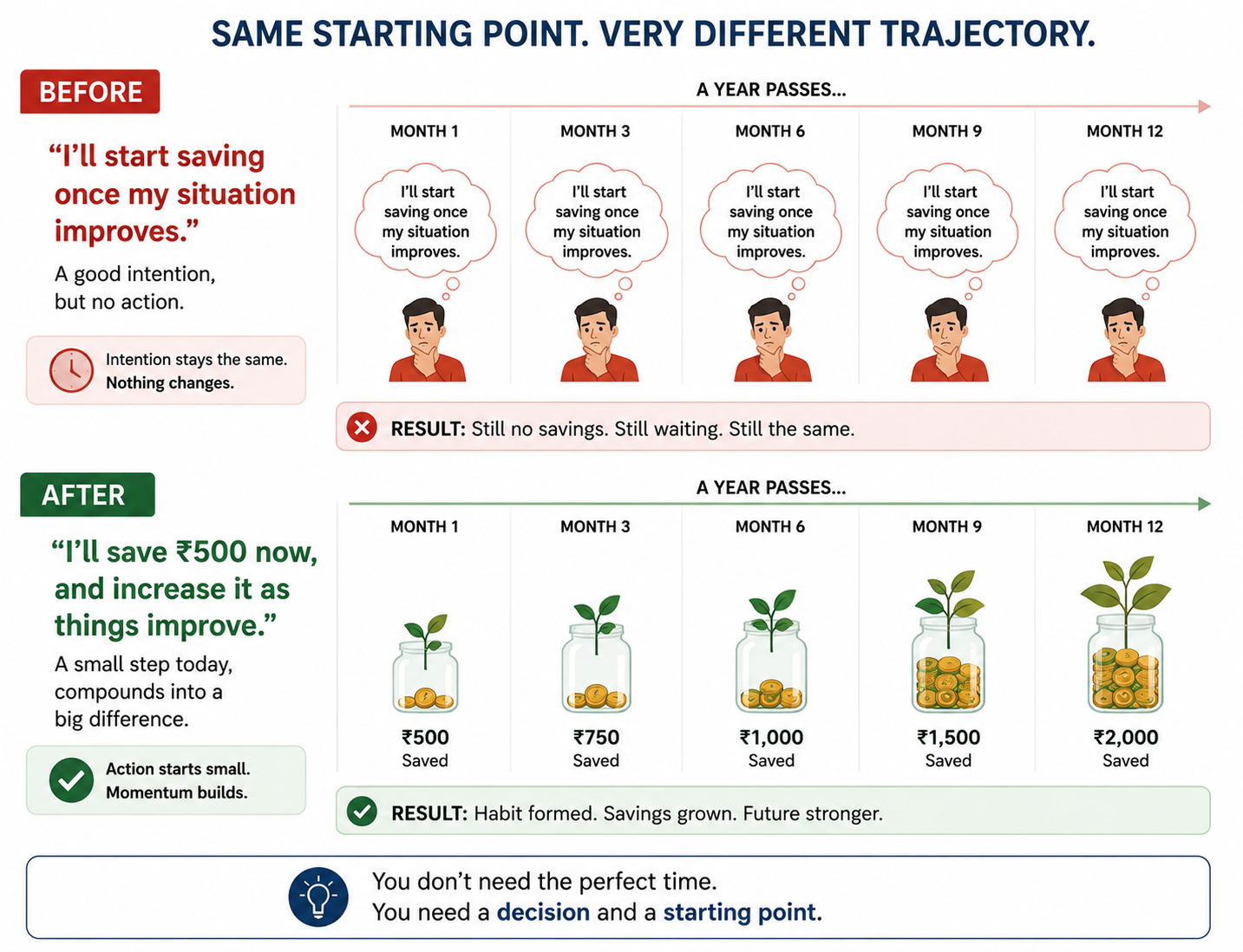

Don't: Wait for a "Good Time" to Start Saving

A consistent pattern across financial situations is the belief that saving will become easier once a specific condition is met, a raise, a bonus, a debt being cleared, a particular expense ending.

This belief is usually inaccurate. Spending reliably expands to match available income, regardless of how much that income is. Someone who cannot save Rs 1,000 a month on their current salary rarely finds it dramatically easier to save Rs 5,000 a month after a raise, unless the habit of saving first was already established before the raise arrived.

The alternative that consistently works: start saving something, even a small amount, now, regardless of how imperfect the current financial situation feels. The specific amount matters far less than establishing the habit before waiting for ideal conditions that, in practice, rarely arrive on their own.

Do: Build an Emergency Fund Before Investing Aggressively

A specific, common mistake is prioritising investment returns before building a basic financial cushion, motivated by the reasonable sounding logic that money sitting in a savings account is "wasted" compared to money that could be growing in the market.

This logic breaks down at the first genuine emergency. Without an accessible emergency fund, an unplanned expense typically has to be funded either by withdrawing from an investment at a potentially unfavourable time, or by taking on high interest debt, both of which usually cost significantly more than the modest return an emergency fund would have missed out on by sitting in cash.

Build a starter emergency fund of at least 1 month of essential expenses before directing significant money towards investments. This is not a permanent restriction on investing, it is a sequencing decision, cushion first, growth second, that consistently protects the growth once it begins.

Don't: Use Your Credit Limit as a Measure of What You Can Afford

One of the most consistently damaging patterns is treating an available credit limit as if it represents actual available money, "the card has Rs 80,000 available" functioning, mentally, as though it were Rs 80,000 in a savings account.

A credit limit is not income. It is borrowed money, set by a bank's assessment of lending risk, not by your actual budget or repayment capacity. Spending based on what a card allows, rather than what a bank account and budget genuinely support, is one of the most direct paths into debt that feels, in the moment, like it is not actually happening.

The reliable check: before any credit card purchase, ask whether the money to repay it is already available in a savings or checking account, separate from the card itself. If yes, the card is being used as a convenient payment method. If no, the purchase is being financed, whether or not it feels that way at checkout.

Do: Automate the Decisions You Don't Want to Make Every Month

Financial habits that depend on remembering and deciding every single month, transferring savings, paying extra towards debt, contributing to a long term investment, are reliably less consistent than the same habits set up to happen automatically.

This is not a matter of discipline or character. It reflects a well established pattern: any financial action requiring an active, repeated decision will eventually be skipped during a busy or difficult period, regardless of good intentions. Automated actions do not depend on that decision being made well every single time.

Set up automatic transfers for savings, extra debt payments, and investment contributions on salary day, before the money is available for discretionary spending. This single change consistently produces more reliable long term progress than any amount of willpower applied to manual, monthly decisions.

Don't: Compare Your Finances to What Other People Appear to Have

Financial comparison, to friends, colleagues, or social media, is one of the most consistent drivers of spending that outpaces actual income, because the comparison is almost always based on visible outcomes, a vehicle, a vacation, a lifestyle, rather than the underlying financial reality, which frequently includes debt that is not visible at all.

Someone financing a lifestyle through credit cards and loans can appear, from the outside, identical to someone genuinely affording the same lifestyle through income and savings. The comparison offers no actual information about which situation is true, and spending to match a visible lifestyle whose underlying finances are unknown is a decision made with incomplete information.

The more useful comparison is to your own goals and your own previous financial position, not to anyone else's visible spending. Progress measured against your own past position is both more accurate and more motivating than progress measured against an incomplete picture of someone else's.

FREED Expert Tip

If a specific comparison, a friend's new car, a colleague's vacation, is triggering a spending decision, pause and ask a specific question: would I make this purchase if no one else would ever know about it? If the honest answer is no, the decision is being driven primarily by comparison rather than genuine want or need, and is worth reconsidering on that basis alone.

Talk to FREEDDo: Understand the True Cost Before Taking Any Loan

Loan decisions are frequently made based on the monthly EMI alone, "can I afford Rs 9,000 a month," without calculating the total amount that will actually be repaid over the full tenure, which can be significantly higher than the amount borrowed, particularly at higher interest rates or longer tenures.

Before accepting any loan, calculate and compare the total repayment amount across a few different tenure and rate combinations, not just the monthly EMI. A loan with a lower EMI due to a longer tenure often costs meaningfully more in total interest than a shorter tenure with a higher monthly payment.

Always ask for the Annual Percentage Rate, which includes fees alongside interest, and compare loan offers using this figure rather than the advertised interest rate alone, since two loans with identical interest rates can have very different true costs due to processing fees and other charges.

Don't: Ignore Small, Recurring Charges

Individual small recurring charges, a subscription, a small monthly fee, a minor add on service, rarely feel significant enough to warrant attention on their own. Collectively, and over time, they consistently add up to a meaningfully larger amount than most people estimate without actually reviewing them.

Review recurring charges, subscriptions, memberships, auto renewing services, at least twice a year. Cancel anything that is not providing clear, ongoing value, and consolidate overlapping services where possible.

This review consistently uncovers forgotten or underused subscriptions that, once cancelled, free up a modest but genuine amount of monthly income, often enough to meaningfully contribute to an emergency fund or debt repayment goal without requiring any change to larger spending categories.

Do: Address High Interest Debt Before Almost Anything Else

Nearly every category of financial advice, saving, investing, building credit, comes with an important exception: it should generally wait behind addressing high interest debt, specifically credit card debt at 36 to 42% per year.

The mathematics are direct. No conventional investment reliably returns 36 to 42% annually. Paying down debt at this interest rate is, in effect, earning a guaranteed return equal to the avoided interest, a return that outperforms nearly every other financial action available. This is why high interest debt repayment is treated as a priority ahead of most other financial goals, not a competing goal to be balanced evenly alongside them.

Where multiple debts exist at different interest rates, direct extra payments towards the highest interest debt first, while maintaining minimum payments on the rest, a specific application of this same principle.

Don't: Let Shame Keep You From Asking for Help

A consistent, damaging pattern across financial situations, distinct from any specific financial mistake, is delaying seeking help, from a bank, a financial counsellor, or a service like FREED, out of a sense that asking means admitting failure.

This delay is costly in a very concrete way. Interest continues to accrue, options that were available earlier, restructuring before default, negotiating before an account reaches NPA, narrow over time, and problems that were manageable when addressed early frequently become significantly harder to resolve the longer they are left unaddressed.

Financial difficulty is common, and reflects circumstances and decisions, not a permanent judgement of character. Seeking help early, while more options are still available, consistently produces better outcomes than waiting until a situation has become severe enough to feel undeniable.

What the Law Says

Under RBI's Fair Practices Code, all lenders are required to disclose the full cost of credit, including the Annual Percentage Rate, fees, and charges, clearly and in writing before an agreement is signed. This requirement exists specifically so that borrowers can make loan decisions based on true, comparable costs rather than an advertised interest rate alone. If this information is not provided clearly, you have the right to request it directly from the lender before proceeding.

Know your credit rightsHow to Tell Which Advice Applies to You

Not every piece of general financial advice applies equally to every situation, and part of using this list well is recognising which items are most relevant right now.

If high interest debt currently exists, the "do" around addressing it first outweighs most other items on this list in terms of priority, this is not a suggestion to ignore the others, but a sequencing point, address the highest cost item first.

If no high interest debt exists but an emergency fund is not yet built, that becomes the next priority, ahead of aggressive investing or additional goals, for the reasons outlined earlier.

If both of these foundations are in place, the remaining items, tracking, automating, avoiding comparison, understanding loan costs, and reviewing recurring charges, function as ongoing maintenance rather than urgent priorities, valuable at any stage but not blocking further progress the way unresolved high interest debt does.

When the Basics Are Not Enough

Every item on this list assumes a financial situation where better habits alone can meaningfully change the outcome, where the gap between current behaviour and a genuinely healthy financial position can be closed through tracking, automation, and consistent decision making.

There is a specific situation where this assumption does not hold. If existing debt, particularly credit card debt, has already grown to a level where even disciplined minimum payments consume a large share of monthly income, better daily habits, however well followed, cannot close that gap on their own. The debt itself has become large enough to require restructuring, not just better management.

FREED's Debt Consolidation Program combines multiple high interest debts into one lower interest loan with a single, more manageable EMI, creating the room needed for the habits in this list to actually work.

FREED's Debt Resolution Program negotiates a reduced settlement for debt that cannot realistically be repaid in full, on average 56% less than the original outstanding, removing the obstacle entirely rather than working around it.

A free consultation can assess honestly whether your specific situation is one where better habits are enough, or one where the debt itself needs to be addressed first.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions