6 Practical Ways to Control Overspending Right Now

Money gone before the month is half over? You are not spending too much on one big thing - you are likely leaking money in six small ways. Here is how to plug each one starting today.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Overspending is rarely caused by one large, obvious expense. It is almost always caused by multiple small, untracked expenses that together exceed income.

Tracking every rupee for one month - however uncomfortable - is the fastest way to identify where the leaks are. Most people find Rs 2,000 to Rs 5,000 of spending they were not fully aware of.

The 24-hour rule - waiting one full day before any non-essential purchase above Rs 300 - eliminates most impulse spending without any other change in behaviour.

If overspending has already created credit card debt or loan dependence, addressing the debt itself - not just the behaviour - is necessary for a real reset.

FREED helps people whose debt from overspending has grown beyond what budgeting alone can fix.

Why Overspending Happens - It Is Not About Willpower

Most people who overspend are not careless or irresponsible. They simply lack visibility into where their money is going.

When spending is untracked - no budget, no monthly review - small purchases accumulate invisibly. Rs 150 for food delivery today. Rs 200 for a cab instead of the metro. Rs 300 impulse purchase online. Rs 199 subscription that has been on auto-renew for a year. Individually, none of these feel significant. Together, they add up to thousands per month in unplanned spending.

The solution is not willpower. It is systems - simple habits that make good spending decisions automatic rather than requiring constant conscious effort.

These 6 ways are practical, immediate, and do not require significant sacrifice.

CTA - Transactional

Overspending has led to growing credit card debt? Talk to a FREED Expert for free - we will help you find a structured way out.

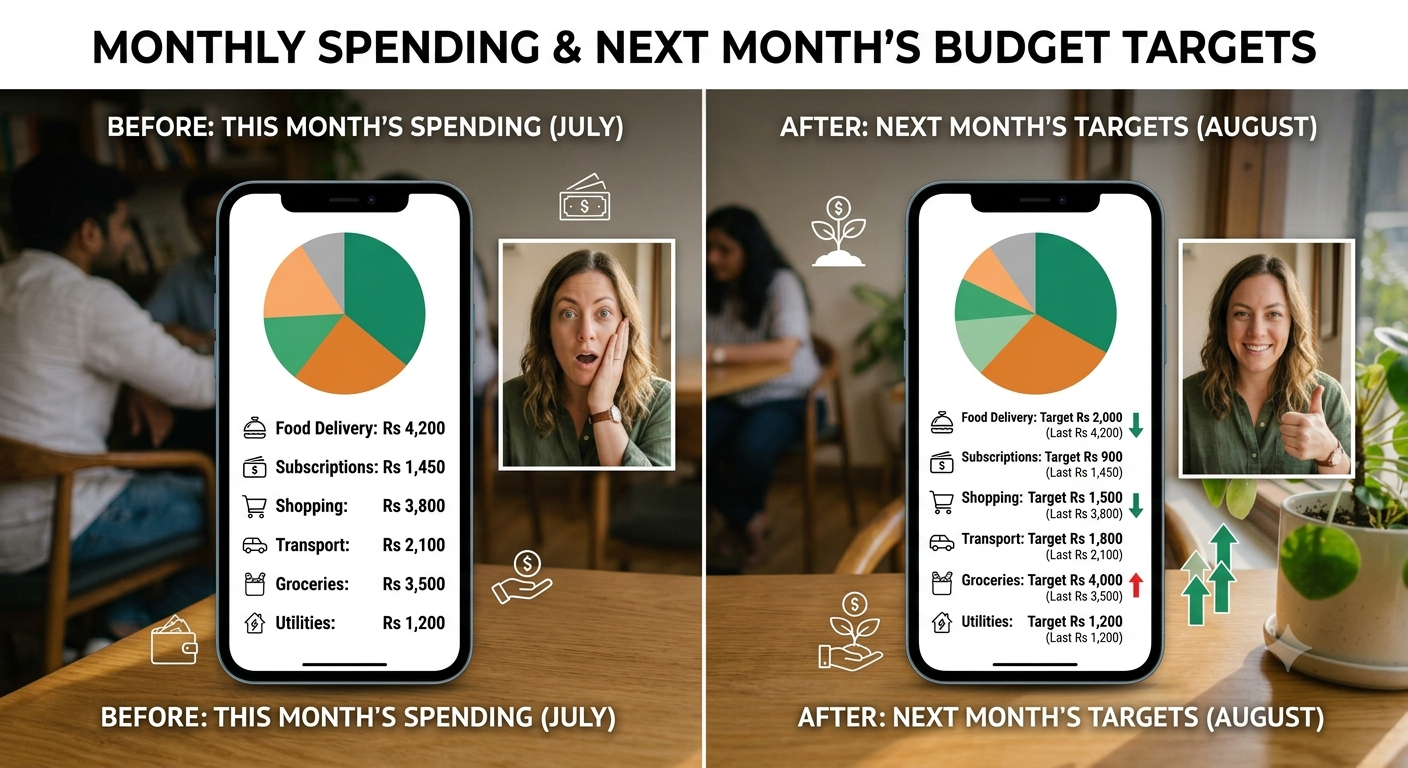

Connect with FREED ExpertWay 1: Track Every Expense for One Month

This is the most powerful thing you can do - and the step most people skip because it feels tedious.

Track every single expense for one calendar month. Every chai. Every auto ride. Every online order. Every subscription charge. Everything.

Use a notebook, the Notes app on your phone, or a free app like Walnut, Money Manager, or your bank's own spending tracker. The tool does not matter. The completeness does.

At the end of the month, categorise your spending: food, transport, entertainment, subscriptions, shopping, EMIs, utilities. Look at each category total. Compare to what you thought you were spending.

Most people are genuinely shocked. Food delivery alone is often Rs 3,000 to Rs 5,000 per month for people who did not realise they were ordering that frequently. Subscriptions total Rs 1,000 to Rs 2,000. Shopping is underestimated by 40 to 60%.

This single exercise changes spending behaviour for months afterwards - because the numbers are now visible and specific, not vague and abstract.

Way 2: Apply the 24-Hour Rule Before Every Non-Essential Purchase

Impulse spending is the single biggest driver of overspending for most people. The phone looks great. The sale ends tonight. The item is in the cart already.

The 24-hour rule is simple: before making any non-essential purchase above Rs 300, wait 24 hours. Sleep on it. Come back tomorrow.

Most impulse urges disappear within a few hours. The item that felt urgent at 9 PM feels unnecessary or postponable at 9 AM the next day. The research on impulse buying consistently shows that the desire to purchase peaks at the moment of exposure and declines significantly within 24 hours.

This one rule alone saves most people Rs 1,000 to Rs 3,000 per month - without any other change in behaviour or any meaningful sacrifice in quality of life.

Apply it to online shopping, in-store purchases, food delivery, and any subscription upgrade or new service. If it still feels worth it 24 hours later - buy it. If not, you just saved that money.

FREED Expert Tip

Delete shopping apps from your phone for one month — not the accounts, just the apps. The extra friction of reinstalling before a purchase is often enough to stop impulse buys. Most people see spending drop 40-60% in that month.

Check My Financial Health ScoreWay 3: Cancel Subscriptions You Are Not Actively Using

Subscriptions are the most invisible form of overspending because they are automatic. The charge appears on the credit card statement and is paid without thought.

Go through your last three months of bank statements and credit card bills. List every recurring charge. Ask for each one: have I actively used this in the last 30 days?

Common subscriptions people forget they have: streaming services they no longer watch, music apps they stopped using, news subscriptions opened for one article, fitness apps downloaded and abandoned, cloud storage plans larger than needed, software trials that converted to paid plans automatically.

Cancel everything you have not actively used in the last 30 days. You can always resubscribe when you genuinely want it again. The money saved is real and immediate - from the next billing cycle.

Most people find Rs 500 to Rs 2,000 per month in subscriptions they were not actively using.

Way 4: Reduce Food Delivery and Eating Out

Food is typically the largest controllable expense in a monthly budget. And the shift to food delivery apps in Indian cities has made it dramatically more expensive than eating the same food at a restaurant or cooking at home.

The average food delivery order in India includes a base food cost, a delivery fee, a platform fee, packaging charges, and a service fee. A meal that costs Rs 150 at a restaurant costs Rs 250 to Rs 350 delivered at home.

Cooking the same meal at home costs Rs 50 to Rs 80.

The calculation across a month is significant. Someone ordering food delivery 15 times per month at an average of Rs 300 per order spends Rs 4,500. Cooking those same meals at home costs approximately Rs 900 to Rs 1,200. Monthly saving: Rs 3,000 to Rs 3,600.

The goal is not to eliminate eating out or food delivery. It is to make them conscious choices rather than default behaviour. Cook at home Monday to Thursday. Reserve eating out or delivery for a specific number of occasions per week - decided in advance.

What the Law Says

Under RBI guidelines, banks must give you a detailed account statement free of charge on request, for savings, credit card, or loan accounts. If you spot charges you don't recognize (platform fees, auto-renewals, subscription debits), you can request an itemised statement and dispute them directly with the bank, or escalate to the RBI Banking Ombudsman if unresolved.

Talk to a FREED ExpertWay 5: Use Cash or Debit for Daily Spending - Not Credit Cards

Credit cards create a psychological distance from the money being spent. Tapping a card does not feel like spending money the way handing over physical cash does. This is not a personal failing - it is well-documented behavioural economics.

For daily expenses - groceries, auto rides, small purchases - switch to cash or UPI debit from your savings account. When the money comes directly from your account, you feel the impact immediately. Spending decisions become more considered.

Keep your credit card for planned, budgeted purchases that you know you will pay in full before the due date. Not for daily habitual spending.

If you already have credit card outstanding that is growing - stop using the card for any new purchases until the outstanding is brought to zero. Using a card with a growing balance adds to the interest being charged every month.

Way 6: Set a Weekly Spending Limit - Not Just a Monthly Budget

A monthly budget is valuable. But it has a practical problem: if you overspend heavily in the first two weeks of the month, you know about it only at month end - when the damage is done.

A weekly spending limit solves this. Divide your monthly variable spending allowance by 4. That is your weekly limit for food, transport, entertainment, and shopping combined.

Check it every Sunday. If you are within the weekly limit - continue as normal next week. If you overspent - reduce next week's spending to compensate.

Weekly visibility catches problems while they are still small and correctable. Monthly tracking shows you what went wrong after it has already happened.

When Overspending Has Already Created Debt

These 6 strategies prevent overspending and help reduce it. But if overspending has already resulted in significant credit card outstanding or personal loan debt - the tips above will help at the margin but will not solve the underlying problem.

At a certain level of debt, the interest being added every month outpaces what better budgeting alone can achieve. The debt itself needs to be addressed directly.

If your credit card outstanding is above 3 months of your monthly income - talk to FREED. We will assess your situation and tell you whether debt consolidation, settlement, or another approach makes the most sense for your specific circumstances.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions