Understanding the Difference Between Credit Score and Credit Report

"Check your credit score" and "check your credit report" sound like two ways of saying the same thing. They are not, and the difference matters, because one of them is a summary and the other is the actual evidence behind it, and only one of the two lets you catch an error before it costs you a loan approval.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

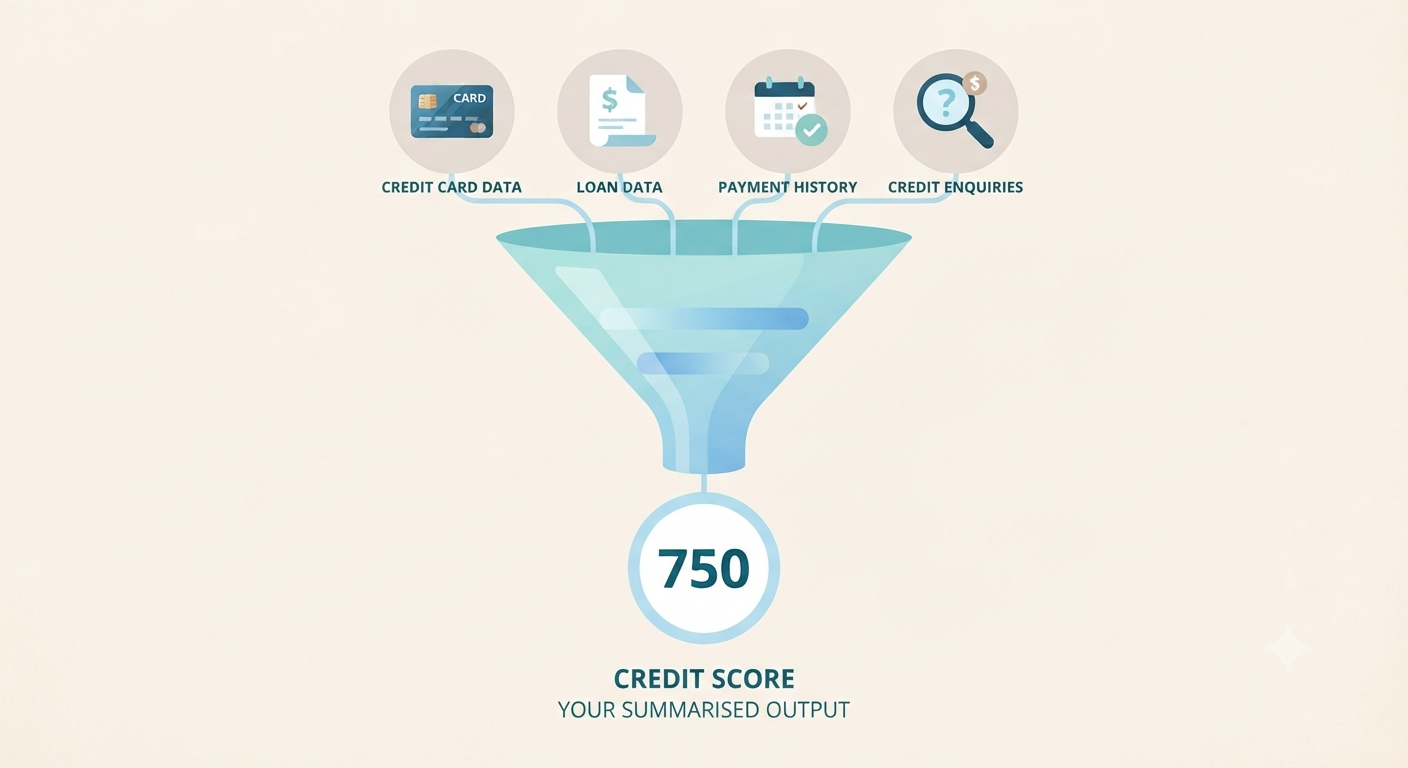

A credit score is a single, three digit number, typically 300 to 900, calculated from your credit history to summarise your creditworthiness at a glance. A credit report is the full, detailed document that number is calculated from.

Checking only your score gives you a summary. Checking your full report is the only way to see the specific accounts, payment history, and enquiries that produced that number, and to catch any errors hiding inside it.

An error in your credit report, an account that is not yours, a payment marked late that was actually on time, can silently lower your score for months before you notice, unless you review the full report directly.

Both the score and the full report can be checked without any cost to your score, since checking your own information is always classified as a soft enquiry.

If report issues reveal an ongoing, unresolved debt problem rather than simply an error to dispute, FREED can help address that debt directly so your report, and the score built from it, can genuinely begin to recover.

Why This Distinction Gets Blurred So Often

Most banking apps and score checking services show you a single number prominently, often with a colour coded gauge, green for good, red for poor, and this is frequently the only piece of credit information most people ever look at. This is not unreasonable, the number is genuinely useful and easy to understand at a glance.

But this convenience creates a specific blind spot. The score is calculated from a much larger, more detailed document, the credit report, and that report can contain specific errors, outdated information, or details worth understanding on their own terms, none of which the summary score alone reveals. Someone who only ever checks their score has, in a real sense, only ever seen the conclusion of a document they have never actually read.

Transactional, Placement: end of Key Summary, before the first section begins

Want a clear read on what your credit report and score actually show? Talk to a FREED Expert for free.

Connect with FREED ExpertWhat a Credit Score Actually Is

A credit score is a single number, generated by a credit bureau using a specific mathematical formula, intended to summarise your overall creditworthiness into one figure that lenders can quickly compare across applicants.

In India, this typically ranges from 300 to 900, with scores above 750 generally considered good, calculated using factors including payment history, credit utilisation, credit history length, credit mix, and recent credit enquiries, combined and weighted according to each bureau's specific model.

The score's entire value lies in its simplicity, it converts a complex, detailed history into one comparable figure. This simplicity is also its limitation, a single number cannot convey which specific factor is helping or hurting you, or whether a specific detail within your history might actually be inaccurate.

What a Credit Report Actually Is

A credit report is the full, detailed document maintained by a credit bureau, listing every credit account you have ever held, credit cards, loans, BNPL commitments, along with the date each was opened, the payment history for each account month by month, current and historical outstanding balances, credit limits, and a complete list of enquiries, both soft and hard, made against your file.

This is, in effect, the raw material the credit score is calculated from. Where the score gives you a single output, the report gives you every input that produced it, specific account names, specific dates, specific payment records, which is considerably more information than the score alone can ever convey.

The Core Difference in One Comparison

The clearest way to hold this distinction is: the score is the answer, the report is the working. A teacher checking only the final answer to a maths problem can tell you whether it is right or wrong. Checking the full working shows exactly which step, if any, went wrong, and lets you fix that specific step directly.

A credit score tells you where you generally stand. A credit report tells you specifically why, which account, which payment, which enquiry is contributing positively or negatively, information the score alone was never designed to communicate on its own.

Why Your Credit Report Deserves Its Own Attention, Not Just the Score

Relying solely on the score means you only find out something is wrong indirectly, through a lower than expected number, without ever seeing what specifically caused it. This becomes a real problem specifically when the cause is an error rather than genuine past behaviour, an account opened fraudulently in your name, a payment incorrectly marked late, an old settled debt that should have been removed from the report but was not.

None of these specific issues are visible in the score alone. They are only visible by opening and reading the full report directly, line by line, which is why relying exclusively on the summary number, however convenient, leaves a real, specific blind spot that only a small amount of additional effort, checking the full report periodically, is needed to close.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What Specifically Lives Inside a Credit Report

A complete credit report typically includes several distinct sections worth knowing about specifically. Personal information, your name, date of birth, and addresses on file, worth checking for basic accuracy. Account information, every credit account ever held, with its current status, open, closed, settled, and its complete payment history. Enquiry information, every soft and hard enquiry made against your file, with the date and the specific entity that made it.

And in some reports, a section listing any specific negative remarks, a written off account, a legal notice, or a formally disputed item, each with enough detail to understand exactly what it refers to, rather than simply seeing its aggregate effect reflected in a lower overall score.

What Specifically Lives Inside a Credit Report" section, roughly one-third through the article

Not sure how to read your own credit report or what to look for? Talk to a FREED Expert for free.

Talk to a FREED ExpertHow Errors in a Credit Report Can Silently Lower Your Score

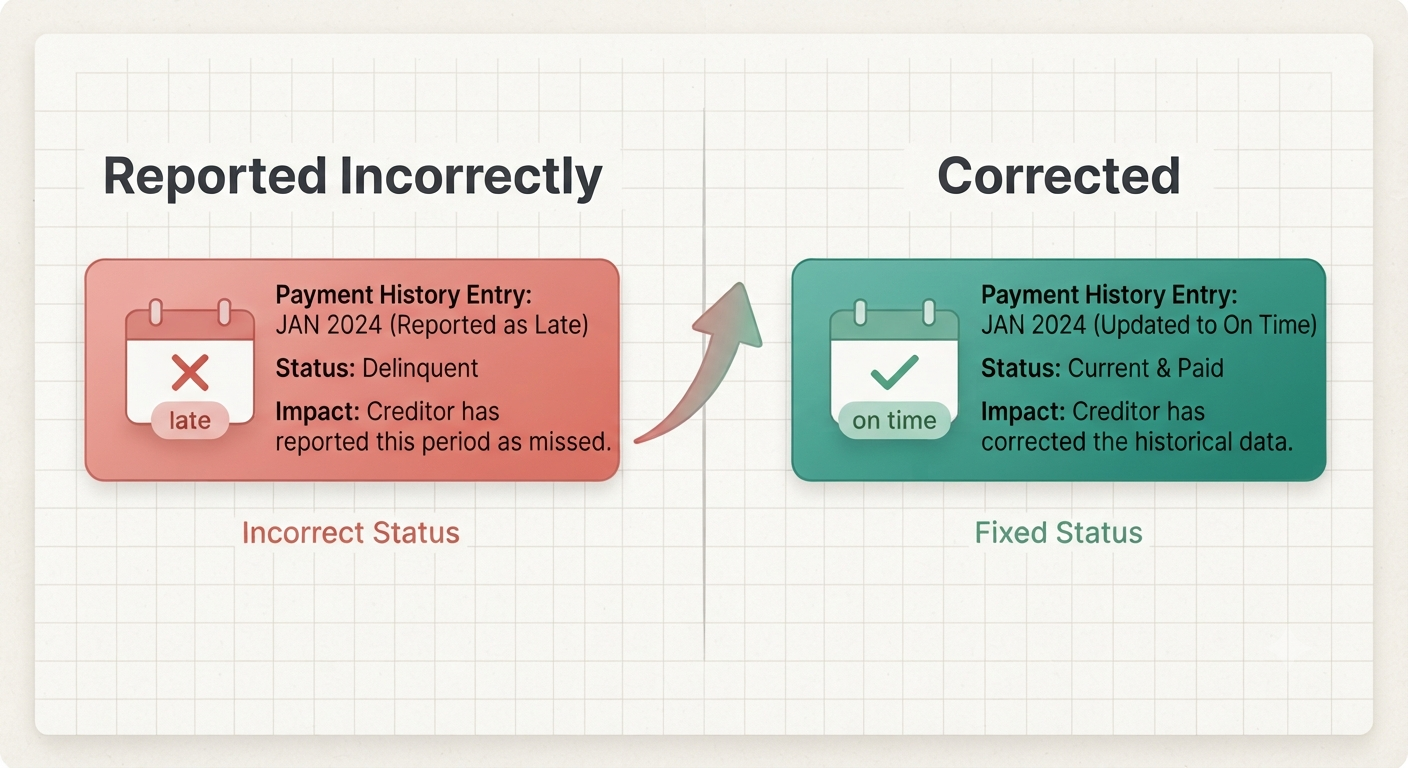

A specific, genuinely common scenario illustrates why this distinction matters practically. An account you closed and fully repaid years ago is still showing as open on your report, due to a lender's administrative delay in updating their records with the bureau. This single error can affect your calculated utilisation and account status, quietly lowering your score, without ever being visible if you only check the summary number.

Similarly, a payment that was genuinely made on time, but recorded late due to a processing delay on the lender's end, can lower your score for months until corrected, an error that is completely invisible in the score itself, and only identifiable by reviewing the specific account entry in the full report directly.

How to Access Both, and How Often

Under RBI regulations, every individual is entitled to one free, complete credit report per year from each of the four licensed bureaus in India, CIBIL, Experian, Equifax, and CRIF High Mark, which means up to four free full reports annually if requested directly from each bureau separately.

Many banking apps and financial platforms also offer a free, simplified score check, often more frequently than once a year, which is useful for quick, regular monitoring, but is not a substitute for periodically reviewing the full report directly, since the simplified view generally shows only the summary score and perhaps a few headline factors, not the complete, detailed account level information the full report contains.

A reasonable practice: check your summarised score through a convenient app whenever you like, since this carries no cost to your score, and set aside time at least once or twice a year to request and actually read through a full report from at least one bureau, specifically checking for accuracy.

What Changes Faster: The Score or the Report

An important, related distinction is that the score and the underlying report do not always move in sync in the way people expect. The calculated score can recover relatively quickly following a period of sustained, positive behaviour, sometimes within months. The underlying report, however, retains the specific historical detail, a past default, a settled account, for a defined period, generally up to 7 years, considerably longer than the score's own recovery timeline.

This means a lender reviewing your full report directly, as often happens for larger loan decisions, may still see and weigh a specific past event that your currently improved score no longer fully reflects, a distinction worth understanding so that score recovery is not mistaken for the complete disappearance of a past issue from your full record.

What the Law Says

Under RBI regulations, credit bureaus are required to investigate and correct any formally disputed inaccuracy in your credit report within a defined timeframe, generally 30 days. This right to dispute applies specifically to the full report, not the summary score, since the score itself cannot be directly disputed or corrected, only the underlying data it is calculated from, which is a further, specific reason the full report deserves direct, periodic attention rather than relying on the score alone.

Check My Credit Score FreeA Simple Habit That Uses Both Correctly

The most effective, low effort habit combines both tools for what each is actually good at. Check your summarised score through a convenient app monthly or whenever you like, since this costs nothing and gives a quick, general sense of direction, improving, stable, or declining.

Separately, request and carefully read a full credit report from at least one bureau once or twice a year, specifically checking the accuracy of every listed account, confirming there are no unfamiliar accounts or enquiries, and verifying that any previously resolved issue, a settled account, a corrected late payment, is accurately reflected as resolved.

This combination, frequent light monitoring through the score, periodic deep review through the full report, gives a considerably more complete and accurate picture than relying on either one alone.

Want help understanding what a specific entry in your credit report actually means?

Talk to a FREED Expert for free.

Talk to a FREED ExpertWhen Report Issues Point to a Deeper Debt Problem

For some people, reviewing a full credit report reveals a specific, isolated error, an outdated account status, an incorrectly recorded payment, that can be formally disputed and corrected directly with the bureau, resolving the issue without needing any broader financial intervention.

For others, a full report review reveals something more structural, several genuinely accurate negative entries, multiple accounts currently overdue, a pattern reflecting an ongoing, unresolved debt situation rather than a data error to dispute. In this second case, no dispute process will resolve the underlying issue, since the entries are accurate, the debt itself needs to be addressed directly.

FREED's Debt Resolution Program negotiates a reduced settlement for debt that cannot realistically be repaid in full, on average 56% less than the original outstanding, stopping the ongoing accumulation of new negative marks on your report and creating a clear point from which genuine recovery can begin.

FREED's Debt Consolidation Program combines multiple debts into one lower interest loan with a single, manageable EMI, supporting a return to the consistent, on time payment history that gradually improves both your report and your score over time.

A free consultation can review your specific situation and confirm whether what your report shows is a correctable error, or a debt issue that needs direct attention.

FREED Financial Health Score

Want an honest read on what your credit report and score currently reflect? Take the FREED Financial Health Score, free, 2 minutes.

Check My Financial Health ScoreFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions