How to Win Over an Outstanding Credit Card Debt?

Outstanding credit card debt grows every month it is not addressed. Winning over it requires three things working together: stopping the growth, a clear repayment strategy, and the right exit for the situation. Here is how.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Outstanding credit card debt in India costs 36% to 42% annually. Every month the balance is not actively reduced, it grows, making the eventual clearance more expensive and more difficult.

Winning over the debt requires three phases: stopping new charges so the balance stops growing, choosing the right exit strategy based on the outstanding size and monthly income, and building habits that prevent the pattern from recurring.

The right exit strategy depends on the total outstanding, whether the account is current or in default, and what monthly income is available. Self-repayment works for manageable balances. Professional consolidation or settlement works for larger ones.

The mental shift that makes the difference: treating the outstanding credit card debt as the opponent, not the bank. The bank is a party to negotiate with. The debt is what needs to be defeated.

FREED helps people defeat credit card debt when self-directed strategies are not enough.

What "Winning Over" Outstanding Credit Card Debt Actually Means

The phrase "winning over" debt is deliberate. Outstanding credit card debt is not a passive obligation waiting to be repaid. It is an active, compounding force working against the person carrying it. At 3.5% monthly interest, a Rs. 50,000 balance that receives only minimum payments does not stay at Rs. 50,000. It grows. The interest added each month outpaces the principal reduced by the minimum payment. The balance persists and increases.

Winning over it means ending that dynamic. It means the outstanding balance is decreasing every month, not growing. It means there is a specific end date, a month when the last rupee is cleared and the account goes to zero. And it means the habits that created the balance have been replaced with ones that prevent it from returning.

This is achievable for every person carrying outstanding credit card debt in India. The path and the timeline vary by the size of the balance and the income available. But the destination is the same: zero balance, no interest charges, and a credit profile that reflects what was accomplished.

Step 1: Stop the Debt from Growing

No exit strategy works while new charges are being added to the balance.

Every purchase made on the card while a balance is carried is added to the outstanding and begins accruing interest immediately. Even small purchases, Rs. 500 for groceries, Rs. 200 for a meal, add to the base on which 3.5% monthly interest compounds.

The first action is removing the card from all spending contexts: unlink from food delivery apps, e-commerce accounts, and subscription auto-debits. Move all daily spending to UPI or a debit card. If the card is used for auto-paying a utility or subscription, redirect that payment to a bank debit.

Do not close the card account. Closing a card reduces total available credit limit and raises credit utilisation ratio, both of which suppress the CIBIL score. The account stays open. The card is simply no longer used for new purchases until the balance is zero.

From this point, the balance only moves in one direction.

FREED Expert Tip

The most reliable way to stop new charges is to physically remove the card from the wallet and delete it from all digital payment apps and websites. The friction of having to retrieve the card before using it creates a pause that prevents impulse spending. Out of sight, out of swipe.

Enroll NowStep 2: Know the Exact Outstanding

Before choosing an exit strategy, the exact, current, full outstanding balance needs to be known.

This is not the minimum due. It is not the approximate amount. It is the complete outstanding: principal, all accrued interest since the last statement, any late fees, any penalty charges, any annual fee added since the last payment.

Pull the current statement from the bank app or website. Note the full outstanding figure shown. Calculate what 3.5% of that figure is: this is the interest being added to the outstanding every month simply from the passage of time. This number is the cost of each month of delay.

Write it down. The specific number, uncomfortable as it may be, is the opponent. Knowing its exact size is what makes a plan to defeat it possible.

Step 3: Assess the Right Exit Strategy

The right exit depends on three variables: the total outstanding, whether the account is current or in default, and what monthly income can realistically be directed toward the balance above the minimum payment.

If total outstanding is below Rs. 1 to 1.5 lakh and monthly income allows paying Rs. 5,000 to Rs. 10,000 above the minimum: self-directed accelerated repayment clears it within 12 to 18 months.

If total outstanding is Rs. 1.5 to 5 lakh and the account is current: EMI conversion, balance transfer, or a personal loan at a lower rate restructures the debt more cost-effectively.

If total outstanding exceeds Rs. 5 lakh across multiple cards, or the account is in default with accumulated interest and penalties: professional debt consolidation or negotiated settlement is the appropriate path.

The sections below explain each strategy in detail.

Strategy 1: Accelerated Self-Repayment

For balances that are clearable within 12 to 24 months of disciplined above-minimum payments, self-repayment is the cleanest exit. No new products. No professional fees. Just consistent, automated payment significantly above the minimum every month.

The mechanics: calculate the monthly payment that clears the balance within the target timeline. Set up an auto-debit or standing instruction for this exact amount to leave the account on the 3rd of each month, before any discretionary spending. Track progress monthly.

On a Rs. 60,000 balance at 3.5% monthly interest: paying Rs. 5,000 per month clears it in approximately 14 months. Paying Rs. 8,000 clears it in approximately 9 months. Every Rs. 1,000 increase in the monthly payment shortens the timeline and reduces total interest paid meaningfully.

Direct any windfall, bonus, tax refund, or salary increment toward the outstanding. Each lump sum reduces the principal, which reduces subsequent interest charges from the following month.

Strategy 2: EMI Conversion

Many Indian credit card issuers allow the outstanding balance to be converted to a fixed EMI at a lower interest rate, typically 12% to 24% annually versus the standard 36% to 42%.

This converts the open-ended revolving balance into a structured instalment with a defined end date. Every EMI payment reduces the principal by a meaningful amount. The balance has a finish line.

Access this through the bank's mobile app or by calling customer care. Request to convert the full outstanding to EMI. Compare the offered interest rate, tenure, and processing fee before accepting. Request these terms in writing.

The condition: do not make new purchases on the card during the EMI tenure. New purchases would be charged at the standard revolving rate while the EMI runs simultaneously, creating two separate debt streams on the same card.

Strategy 3: Balance Transfer

A balance transfer moves the outstanding from the current high-rate card to a new card offering a 0% promotional rate or significantly lower standard rate.

This works when: the promotional period is long enough to make significant principal reduction (ideally 6 months or more), the new card's post-promotional rate is lower than the current card, and the repayment discipline is in place to pay aggressively during the promotional window.

Check the processing fee (typically 1% to 2% of the transferred amount) and calculate whether the interest saved exceeds this cost. Also check the CIBIL score requirement for the new card (typically 700 or above).

The risk: if the promotional period ends without the balance being cleared, the remaining balance starts accruing at the new card's standard rate. The balance transfer helps only when the promotional period is used aggressively, not as another minimum payment period.

Legal Note

Under RBI guidelines on credit cards, issuers are required to disclose the effective interest rate, all fees, and the post-promotional rate clearly before a balance transfer is accepted. Request this information in writing before proceeding. You have the right to full cost disclosure before agreeing to any restructuring of your credit card balance.

Know your rights as a credit card holderStrategy 4: Personal Loan Consolidation

A personal loan at 12% to 20% used to clear a credit card balance at 40% saves 20 to 28 percentage points in annual interest. On a Rs. 2 lakh outstanding, the first-year interest saving alone is Rs. 40,000 to Rs. 56,000.

The personal loan converts the revolving credit card balance into a fixed EMI with a defined end date at a significantly lower rate.

The condition: the credit card must not be used again after being cleared. The freed-up limit is available, and the spending pattern that created the original balance has not changed. A cardholder who clears the card with a personal loan and then accumulates a new card balance ends up with both the personal loan EMI and new card debt. The personal loan consolidation works only when the card spending habit changes alongside the balance change.

Check the CIBIL score before applying. A score above 700 typically qualifies for the best rates. Below 650, the personal loan may not be approved or may be offered at a rate that makes the consolidation less advantageous.

Strategy 5: Professional Debt Consolidation

When multiple credit cards are running simultaneously, each with different balances, different interest rates, and different due dates, managing them individually is both complex and expensive.

FREED's Debt Consolidation Programme combines all credit card balances into one lower monthly payment through negotiation with existing creditors, without requiring a new loan application. This is accessible even when the CIBIL score is too low for a personal loan consolidation.

The benefit: one payment, one due date, one relationship manager, and a lower effective monthly obligation that is actually manageable within current income. For people whose combined credit card minimum payments are consuming a large share of monthly income without making meaningful progress on any individual balance, this approach creates the breathing room that self-directed repayment cannot.

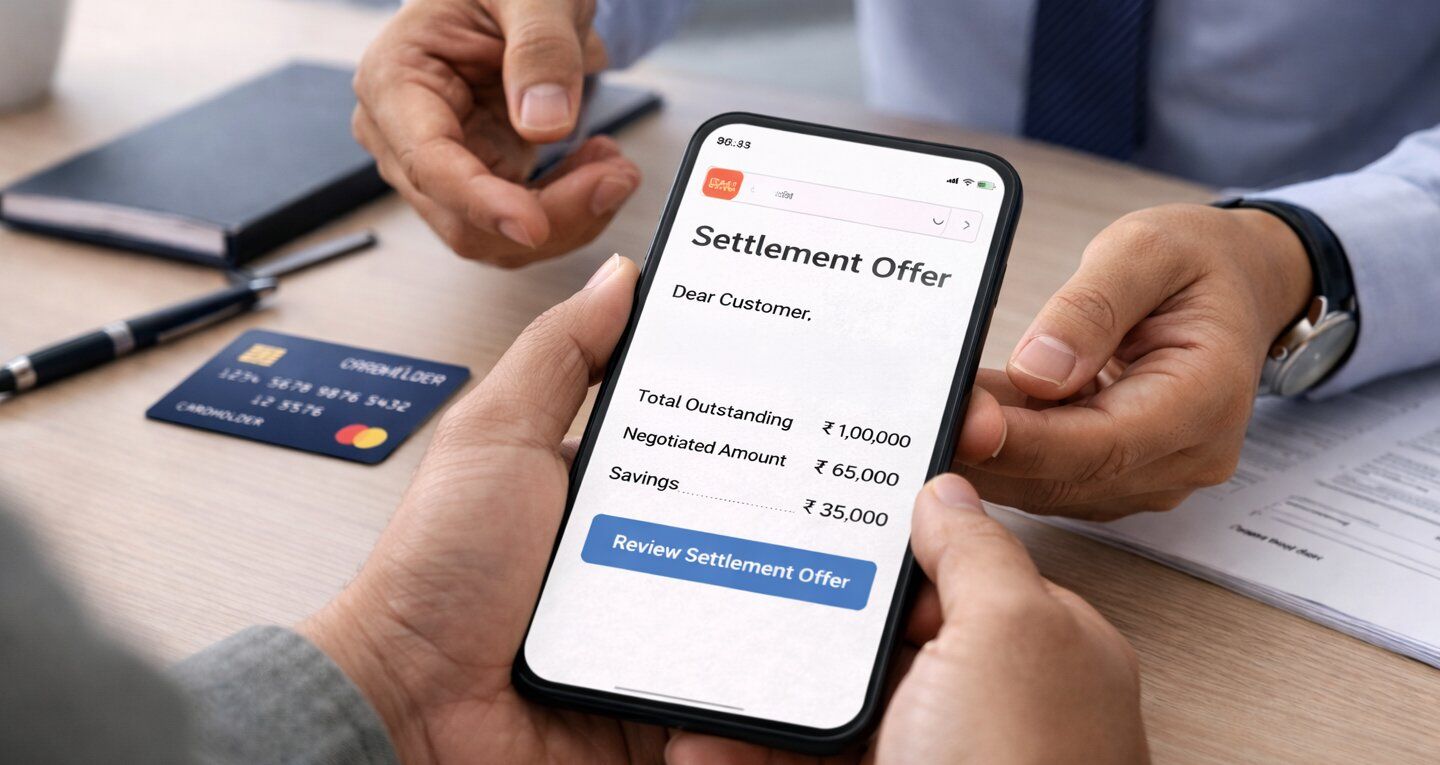

Strategy 6: Negotiated Settlement

For accounts that have been in default for 90 or more days, where the total outstanding including accumulated interest and charges has grown significantly beyond the original balance, and where full repayment is not realistic on current income, negotiated settlement is the direct path to being debt-free.

In a settlement, the bank accepts a negotiated lump sum of 40% to 70% of the total outstanding as complete and final payment. The account is permanently closed. The "Settled" remark appears on the CIBIL report for up to 7 years from the date of first default.

This is the right strategy when the outstanding has grown so large that even restructured full repayment would take 7 to 10 years at significant interest cost, and when the alternative is indefinite default with compounding charges and no defined end.

FREED's Debt Resolution Programme handles the entire settlement process: building the settlement fund through monthly contributions to a Special Purpose Account, negotiating with the card issuer, obtaining the written settlement letter before any payment is released, and following up on the credit bureau update.

Step 4: Build Habits That Prevent It from Returning

Clearing the outstanding credit card debt is winning a battle. Preventing the next one requires the habits that make the same debt pattern impossible to repeat.

Pay the full outstanding balance every billing cycle. Not the minimum. The full amount. This is the non-negotiable foundation.

Keep utilisation below 30% of the available limit at all times. Set up a spending alert in the bank app when the balance reaches 25% of the limit.

Automate the payment to leave the account 2 to 3 days before the due date. Remove the risk of a missed payment from the equation entirely.

Review the statement every month. Reconcile every transaction. Dispute anything unrecognised within 48 hours.

Build a small emergency fund of Rs. 15,000 to Rs. 25,000 specifically so that unexpected expenses do not go on the card. The emergency fund is what prevents the next emergency from becoming the next credit card balance.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

About FREED

FREED is India's leading debt resolution platform. We have helped over 60,000 Indians reduce, manage, and completely get out of debt, legally and without harassment.

We offer Debt Consolidation, Debt Resolution, Credit Score Rebuilding support, and FREED Shield protection against recovery harassment. Every first consultation is free.

Visit freed.care

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions