Financial Security: Take the Step Toward Financial Independence

Financial independence is not a destination for the wealthy. It is a direction available to anyone willing to take the first step. This guide explains what financial security and independence actually mean in India, what the journey looks like in practice, and the specific steps that move a person from financial vulnerability toward genuine financial freedom.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Financial security means having enough to cover today's needs and absorb tomorrow's surprises without anxiety. Financial independence means having enough that work becomes a choice rather than a necessity.

Most Indians are closer to financial vulnerability than financial security, because of the absence of emergency savings, high-interest debt, and no long-term investment portfolio generating returns independent of employment.

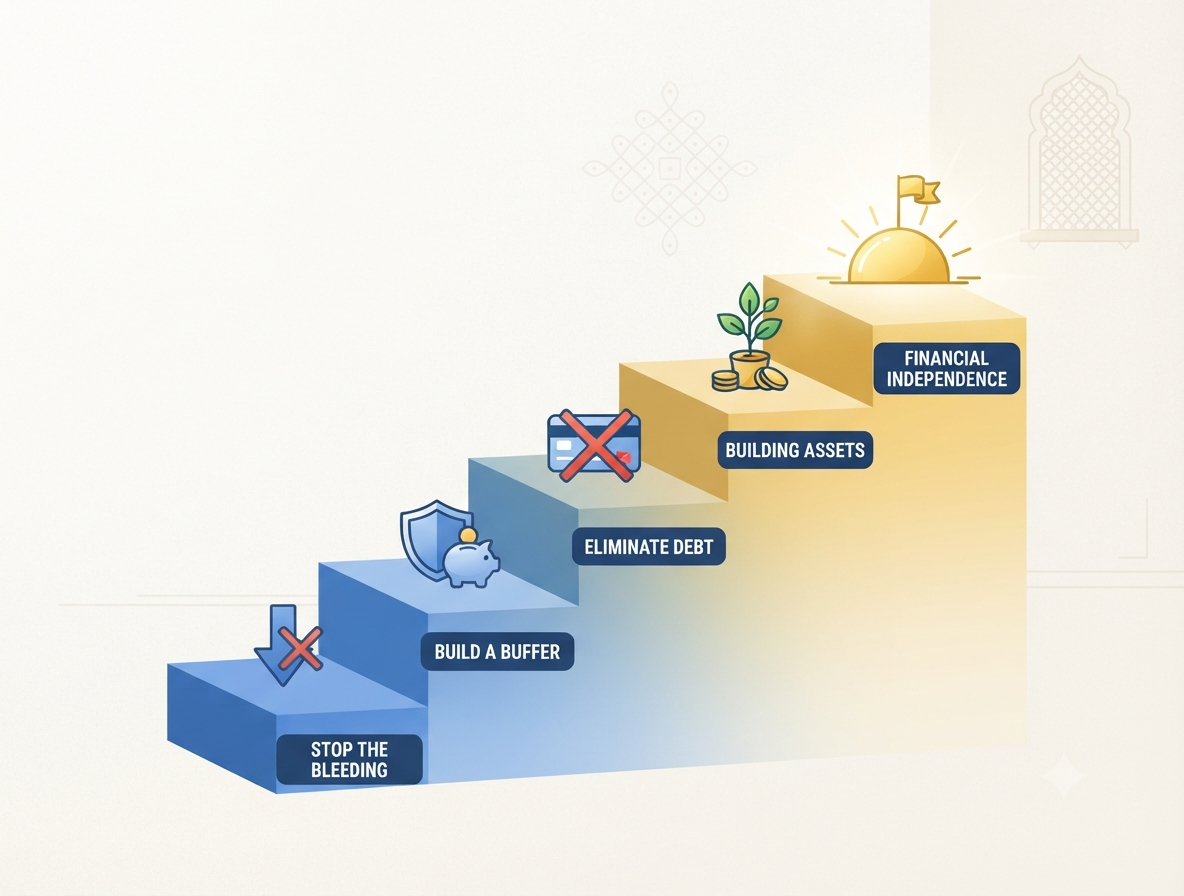

The journey from vulnerability to independence moves through five stages: stopping financial damage, building a buffer, eliminating high-cost debt, building income-generating assets, and reaching financial independence.

The most common reason people do not progress is not low income. It is the absence of a clear plan and the accumulated weight of debt consuming the margin that savings and investment require.

FREED helps address the debt so the plan can actually work, through Debt Consolidation or Debt Resolution, creating the breathing room where the journey toward financial independence can begin.

What Financial Security Means Versus Financial Independence

These two terms are often used interchangeably. They describe different points on the same journey, and the distinction is useful.

Financial security is the state in which monthly income reliably covers monthly obligations with some margin remaining, a buffer exists for unexpected expenses, and the immediate future does not feel precarious. It is not wealth. It is stability. The absence of the low-grade anxiety that comes from not knowing whether the month will end in the black.

Financial independence is a further stage. It is the state in which passive income, savings, and investments are sufficient to cover living expenses without requiring active employment. Work, at this stage, is a choice rather than a necessity. Financial independence is what most people mean when they say they want financial freedom.

The journey from where most Indians currently are to financial security is achievable within years, not decades, with the right priorities applied consistently. The journey from financial security to financial independence is longer and requires sustained investment growth, but it begins with the same first steps.

This guide focuses on both, with honest attention to what each stage actually requires.

Why Most Indians Feel Financially Insecure

Financial insecurity in India is not primarily caused by low income. It is caused by a combination of three things that appear at every income level: insufficient savings to absorb disruption, high-interest debt consuming income that could otherwise build assets, and no long-term investment portfolio generating returns independent of employment.

A family earning Rs. 1.5 lakh per month with Rs. 80,000 in combined EMIs, no emergency fund, and no investments is financially vulnerable. A disruption to income, even temporary, creates immediate crisis. This family does not feel financially insecure because they are poor. They feel insecure because the structure of their finances leaves no margin.

The solution is not more income, though more income helps. The solution is a different structure: obligations that fit within income with room remaining, savings that exist before spending begins, and assets that grow over time independent of monthly salary.

FREED Expert Tip

Financial security does not begin with a target amount. It begins with a habit shift: from spending what remains after obligations to saving what is required before spending begins. This one shift, implemented consistently, creates the margin that makes everything else possible.

Talk to a FREED CounsellorThe Journey in Stages: From Vulnerability to Independence

Financial independence is not a single leap. It is a sequence of stages, each one building on the previous. Trying to skip stages consistently produces failure, because each stage provides the foundation the next one requires.

- 1

Stage 1: Stop the Bleeding

No financial progress is possible while the financial situation is actively worsening. The bleeding takes several forms. Credit card debt that is growing through minimum payment dependency, with interest accruing faster than payments reduce the principal. New debt being taken to cover existing debt obligations. Discretionary spending consuming margin that could be redirected to savings or repayment. Auto-debit failures creating

- 2

Stage 2: Build a Buffer

The single greatest source of financial vulnerability is the absence of any savings buffer. Without one, any unexpected expense creates new debt. Any income disruption creates crisis. The financial position is dependent on nothing going wrong, which is an unsustainable condition. A buffer means an emergency fund: three months of total monthly expenses in a separate, accessible account that is

- 3

Stage 3: Eliminate High-Cost Debt

With the bleeding stopped and a basic buffer in place, the next priority is eliminating debt that is actively destroying wealth. High-cost debt means credit card balances at 36% to 42% annual interest, personal loans above 15% to 18%, and any BNPL obligations with high penalty rates. These products cost significantly more than any safe investment earns. Every rupee of

- 4

Stage 4: Build Income-Generating Assets

With high-cost debt cleared and a buffer established, the monthly income that was previously consumed by interest payments and debt servicing is now available for a different purpose: building assets that generate returns independent of employment. In India, this means a combination of EPF and NPS for retirement (tax-efficient, government-backed), equity mutual funds for long-term wealth growth through SIP, PPF

- 5

Stage 5: Financial Independence

Financial independence arrives when the income generated by accumulated assets, through dividends, rental income, EPF pension, annuity, or systematic withdrawal from a mutual fund corpus, is sufficient to cover living expenses without requiring active employment income. This is not retirement necessarily. Many financially independent people continue to work. What changes is that the work is chosen, not required. A bad

Legal Note

A dedicated emergency fund account does not require a separate bank. Most Indian banks allow multiple savings accounts or sub-accounts with customised labels. A recurring deposit with premature withdrawal facility earns interest while remaining accessible. Under RBI guidelines, banks cannot charge customers for premature closure of RDs beyond the notified penalty rates, which must be disclosed before opening.

Know your savings rights as a bank customer

The One Step Most People Skip

Every stage in this journey has a prerequisite: the willingness to know the actual numbers.

Most people who feel financially insecure have not sat down to calculate their actual FOIR, total outstanding, monthly surplus, or net worth. They have a rough sense, almost always more optimistic than the reality, and they make financial decisions based on that rough sense rather than the actual position.

The most important first step in the journey toward financial independence is a full, honest assessment of where things currently stand. Total income. Total fixed obligations. Total savings. Total outstanding debt. FOIR. Net worth.

This exercise is uncomfortable. The numbers are almost always worse than the estimate. But the actual position, however uncomfortable, is the only honest starting point for any plan that will work.

When Debt Is the Starting Point

For many people reading this, the journey toward financial independence begins from a position of existing debt that makes Stage 1 feel impossible and Stage 2 feel distant.

If monthly debt obligations consume 55% to 65% of income, stopping the bleeding and building a buffer simultaneously is genuinely difficult. The monthly margin is too thin for consistent progress on multiple fronts.

In these situations, reducing the debt load is the prerequisite, not for financial independence, but for the first step toward financial security. FREED helps people in exactly this position. Through Debt Consolidation, multiple high-interest EMIs are combined into one lower monthly payment, creating the margin that makes Stages 1 and 2 possible. Through Debt Resolution, outstanding dues are settled for less than the full outstanding, eliminating those obligations from the budget entirely.

Both approaches do not produce financial independence directly. They produce the breathing room in which the journey toward financial independence can actually begin.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions