Debt Settlement vs Wilful Default: What are your options?

Wilful default and debt settlement are often confused, but they are very different. One involves choosing not to pay despite having the means, while the other helps borrowers who genuinely cannot repay their debt.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A wilful defaulter in India is a borrower who has the ability to repay a loan but deliberately chooses not to or who diverts loan funds away from the stated purpose, or transfers assets to frustrate recovery.

Being classified as a wilful defaulter carries severe legal and financial consequences under RBI regulations.

Debt settlement, by contrast, is a negotiated resolution specifically for borrowers in genuine hardship who cannot repay the full outstanding.

If you are in genuine hardship, settlement is a legitimate path.

If you are considering strategic non-payment to force a better deal, understanding the consequences of wilful default classification is essential before proceeding.

What Wilful Default Actually Means in India

The term "wilful default" has a specific legal meaning in India, defined and governed by RBI Master Circular guidelines on wilful defaulters.

Under these guidelines, a borrower is classified as a wilful defaulter when one or more of the following conditions are met.

The first condition is deliberate non-payment despite the ability to repay. This is a borrower who has funds available in accounts, in assets, or through income and chooses not to service the loan. The bank assesses this through an examination of the borrower's financial position.

The second condition is diversion of funds. This applies when a loan was taken for a stated purpose business expansion, equipment purchase, working capital and the funds were used for a different purpose without the lender's knowledge or consent.

The third condition is siphoning of funds. This is the transfer of loan proceeds or business assets out of the borrowing entity in a way that frustrates the lender's ability to recover.

The fourth condition is disposal or removal of collateral. This applies when a borrower disposes of assets that were pledged as security for the loan without the lender's permission.

These categories are all defined by deliberate action, not by inability. The defining feature of wilful default is that the borrower could service the obligation but chooses not to, or takes actions specifically designed to prevent recovery.

In genuine hardship and not sure what your options are?

Talk to a FREED Expert It's Free.

Connect with FREED ExpertThe Legal Consequences of Being Classified a Wilful Defaulter

The consequences of a wilful defaulter classification in India are severe and extend well beyond the credit score impact that ordinary default produces.

Under RBI guidelines, once a borrower is classified as a wilful defaulter, the bank is required to report this classification to all credit information companies. This appears on the credit report as a wilful defaulter classification which is significantly more serious than a standard NPA or settlement remark.

Wilful defaulters are prohibited from obtaining credit from any bank or financial institution regulated by the RBI for a period of five years from the date of removal of the wilful defaulter tag which itself requires full repayment. In practice, this can mean a borrower who is classified as a wilful defaulter cannot access any institutional credit for many years.

Wilful defaulters are also prohibited from becoming directors of any company including companies they currently direct under Companies Act provisions. This affects business owners and executives significantly.

Banks are required to publish the names of wilful defaulters above certain thresholds. This makes the classification a matter of public record, which has reputational consequences beyond the financial ones.

Criminal proceedings under applicable sections of the Indian Penal Code are also possible for wilful default particularly where fraud, misrepresentation, or diversion of funds is involved.

These consequences are not comparable to ordinary loan default. They represent a qualitatively different legal and financial situation.

Legal Note

Under RBI Master Circular on Wilful Defaulters, a borrower must be given an opportunity to be heard before a wilful defaulter classification is finalised. If your bank is attempting to classify you as a wilful defaulter, you have the right to submit a representation and present your case before the bank's review committee. This right is protected under the circular. If you believe the classification is incorrect, engage a lawyer with expertise in banking law immediately.

Know your rights as a borrowerWhat Debt Settlement Means

Debt settlement is a voluntary, negotiated resolution between a borrower who cannot repay the full outstanding amount and a lender who agrees to accept less as complete and final payment.

The key word in that definition is cannot, not will not. Settlement is available to and appropriate for borrowers in genuine financial hardship. Job loss, income reduction, medical emergency, business failure, family crisis, circumstances that have fundamentally changed the borrower's ability to service the original obligation.

When a borrower's account has been in NPA status for 90 or more days and there is a documented hardship, banks are typically willing to negotiate settlement because recovering something through a voluntary agreement is better than recovering nothing through costly and uncertain legal proceedings.

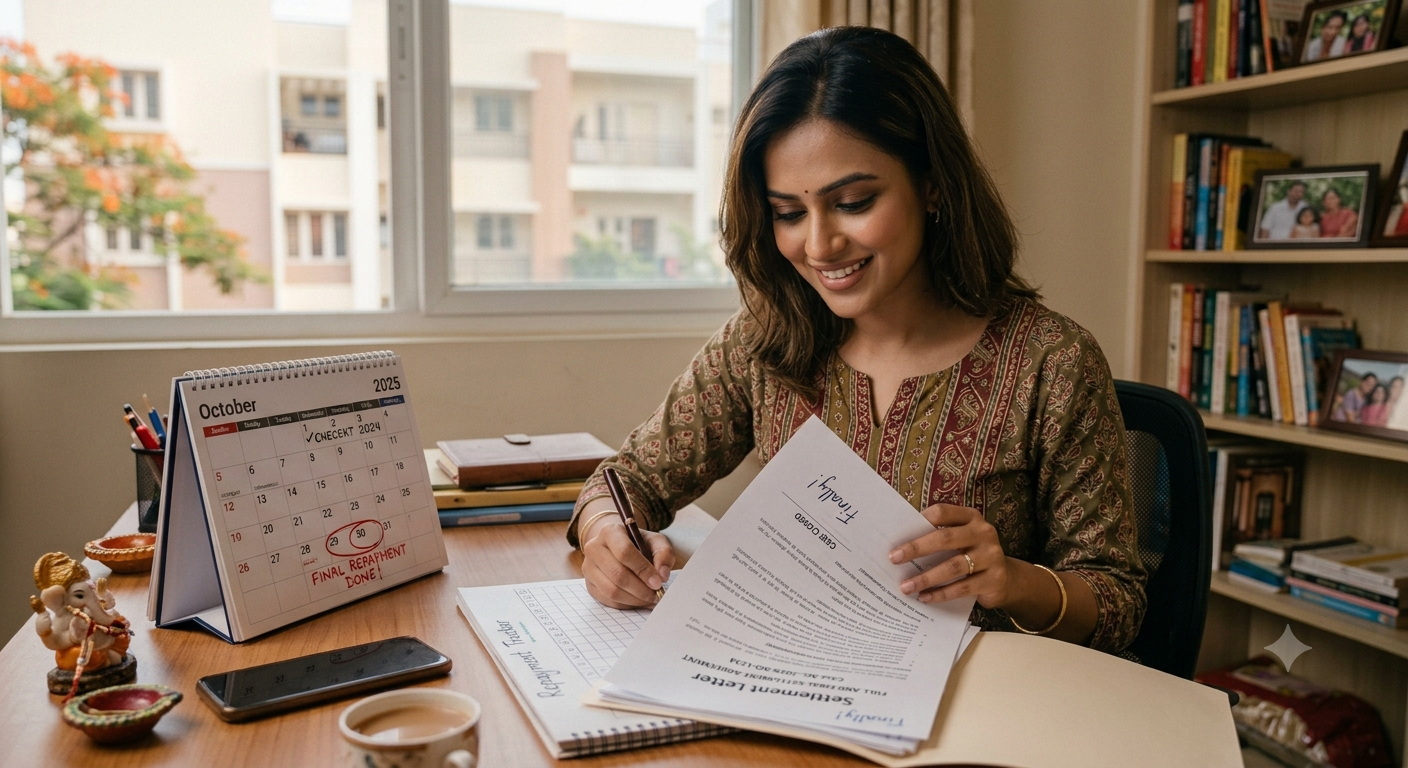

Settlement is legal, widely practiced, and specifically recognised in RBI guidelines as a legitimate resolution mechanism for NPA accounts. It produces a "Settled" remark on the CIBIL report, which is a consequence but a manageable and time-limited one. It does not result in the wilful defaulter classification, the prohibition on obtaining credit, the directorship restrictions, or the criminal exposure that wilful default can produce.

The Critical Difference Between the Two

The difference between wilful default and a situation that leads to debt settlement comes down to one question: can you repay, or can you not?

Wilful default is a choice. It is made by someone who has the means to repay but decides not to whether for strategic reasons, to force a settlement, or through deliberate diversion of funds.

Debt settlement is an acknowledgment. It is made by someone who has genuinely lost the ability to repay under the original terms, is acting in good faith, and is seeking a negotiated resolution with the lender rather than simply refusing to engage.

Banks and their internal investigations teams are experienced at distinguishing between these two situations. A borrower who stops paying while continuing to hold visible assets, maintaining an unchanged lifestyle, and making no attempt to communicate with the lender presents a very different picture from a borrower who lost employment, whose bank statements show materially reduced income, who has medical bills or other documented hardship, and who proactively seeks a resolution.

The distinction matters not just legally but practically in the settlement conversation. A bank is far more willing to offer a meaningful settlement reduction to a borrower who can demonstrate genuine hardship than to one who appears to be strategically withholding payment.

FREED Expert Tip

Some borrowers consider stopping payments as a deliberate tactic to force a settlement offer from the bank, without being in genuine hardship. This is risky for two reasons. First, it can lead to wilful defaulter classification if the bank assesses that payment capacity exists. Second, banks that identify strategic non-payment are less likely to offer favourable settlement terms and more likely to initiate legal proceedings. Settlement works when the hardship is real and documented. It does not work well as a negotiating tactic by someone who can pay.

Assess My Real HardshipWho Qualifies for Settlement and Who Does Not

Settlement is appropriate and accessible when genuine hardship exists when the borrower's financial circumstances have materially changed in a way that makes full repayment under the original terms impossible.

Qualifying situations include job loss with documented evidence such as a termination letter or reduction in Form 16 income; a severe medical event that has depleted savings and reduced income; a business failure where the business revenue has demonstrably collapsed; a family financial crisis that has fundamentally altered cash flow; or the gradual compounding of high-interest debt to a point where even restructured full repayment is mathematically impossible on the current income.

Settlement is not appropriate when the borrower has significant liquid assets or income that could service the debt. It is not appropriate when the intent is to reduce an obligation the borrower can actually meet. And it is not appropriate when the borrower has taken actions, transferring assets, diverting funds that constitute the conditions for wilful defaulter classification.

The assessment of whether someone qualifies is made based on documentation. Income evidence, bank statements, liabilities, and an explanation of what changed and when. This is why FREED's free consultation begins with a thorough review of the actual financial situation before any programme recommendation is made.

What Options Exist If You Genuinely Cannot Repay

For borrowers in genuine hardship whose ability to repay has been materially compromised, several options exist in sequence.

The first option is to approach the lender directly for restructuring before default if possible. A documented hardship conversation with the bank at this stage can produce an EMI reduction, a tenure extension, or a moratorium, without the account entering default.

If restructuring has not been possible or has not been sufficient, and the account is now in default, the next option is formal debt settlement through negotiation. At FREED, this is handled through the Debt Resolution Programme, the full process from hardship documentation through creditor negotiation to the final settlement letter and No Dues Certificate.

For borrowers with multiple accounts across multiple lenders, FREED's programme manages all creditors simultaneously, building the settlement fund through monthly contributions to a Special Purpose Account and negotiating account by account as the fund reaches the threshold for each.

Throughout this process, FREED Shield provides protection against recovery harassment, managing all creditor communications on the borrower's behalf and documenting any harassment for escalation to the RBI Banking Ombudsman where warranted.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What Options Exist If You Are Being Pressured Into Default

A different situation less discussed but real is where a borrower is being pushed toward default through predatory or aggressive collection practices, misleading representations from the lender, or circumstances where the borrower's legal rights are not being respected.

In these situations, the borrower's options include filing a formal complaint with the bank's Nodal Officer, escalating to the RBI Banking Ombudsman for regulatory relief, and seeking legal advice from a banking law specialist if the situation involves potential violations of consumer protection or banking regulation.

Being in default does not mean surrendering legal rights. RBI guidelines provide specific protections that remain in force regardless of the borrower's repayment status including limits on recovery agent behaviour, the right to restructuring conversations, and the right to accurate credit bureau reporting.

FREED's Shield service supports borrowers in these situations, providing documentation of harassment and guidance on the appropriate escalation pathways.

In genuine hardship and looking for a structured, legal way out?

FREED will assess your situation honestly and find the right path. Talk to a FREED Expert Free no pressure.

Connect NowFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions