Debt Management 101: Snowball vs Avalanche - Which Is Better for You?

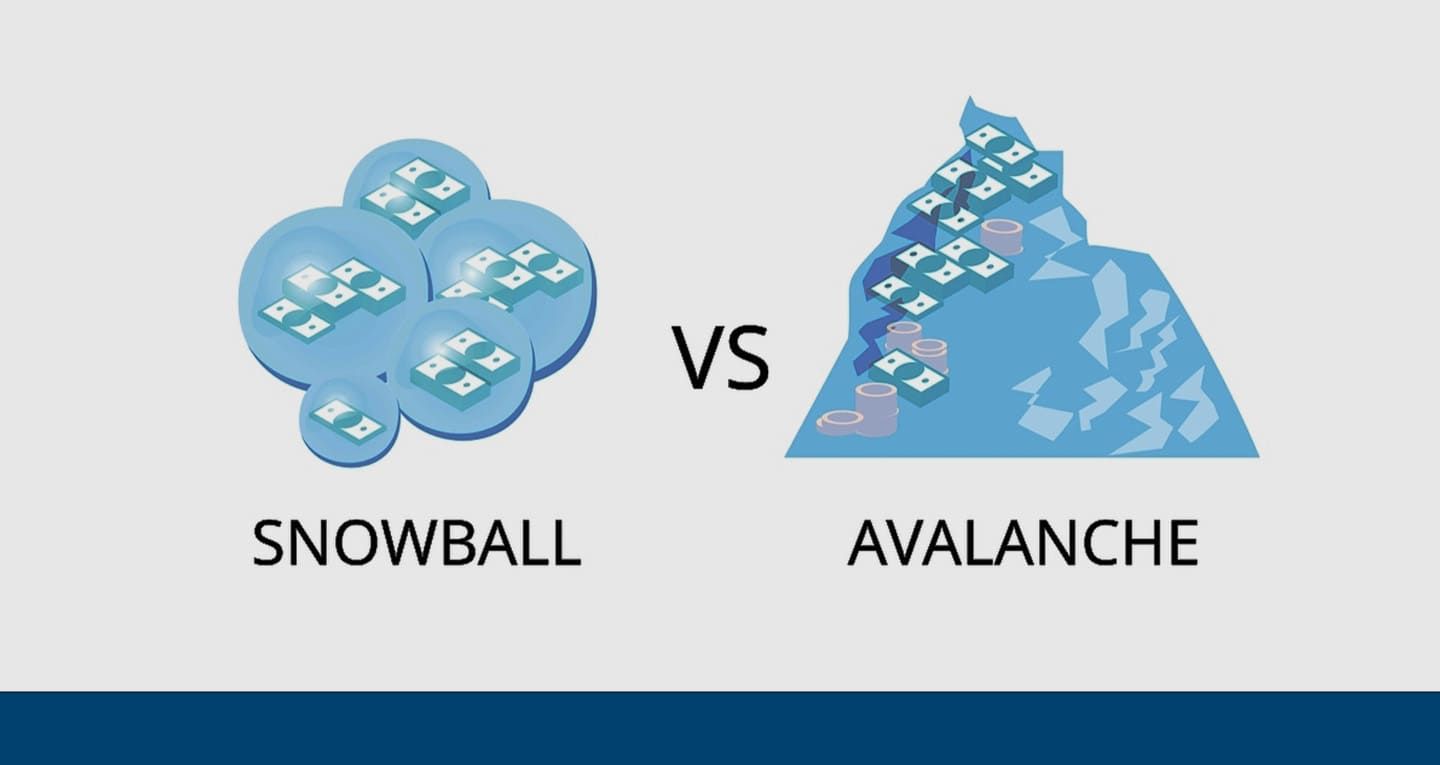

Two proven strategies. One goal: becoming debt free. The snowball method clears small debts first to build momentum. The avalanche method clears high interest debt first to save money. Which one you should use depends less on which is mathematically superior and more on which one you will actually finish.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

The debt snowball and debt avalanche methods are both structured repayment strategies for people who can make more than minimum payments on their debt.

Snowball clears the smallest balance first, producing quick psychological wins.

Avalanche clears the highest-interest debt first, minimising total interest paid.

Mathematically, avalanche wins. Psychologically, snowball keeps more people going until the end.

The best method is whichever one you will sustain consistently.

What Both Methods Have in Common

Before getting into the differences, it is worth being clear about what the snowball and avalanche methods share because this is where most people start on the wrong foot.

Both methods assume the same starting condition: you are making minimum payments on all your debts every month without fail. Neither method works if you are missing payments. The entire logic of both strategies is built on top of a foundation of consistent minimum payments, with additional money being applied to one specific debt at a time.

Both methods also require the same discipline: every rupee that is freed up when one debt is cleared gets immediately redirected toward the next target debt, rather than absorbed into general spending. This compounding of freed-up payments is what makes both strategies effective. Without it, neither works as intended.

If you are currently missing minimum payments or if your income is so tight that there is nothing extra at the end of the month after covering all obligations, then a repayment strategy is not the right starting point. The debt situation needs to be restructured or resolved first. That is a different conversation, and one FREED is equipped to have.

The Debt Snowball Method -- How It Works

The debt snowball method was made famous by American personal finance writer Dave Ramsey, but the underlying logic is simple enough to apply anywhere.

Step one: list all your debts from smallest outstanding balance to largest, regardless of interest rate.

Step two: pay the minimum due on every debt except the one with the smallest balance.

Step three: direct every available rupee above the minimum payments toward the smallest balance debt, as aggressively as possible, until it is cleared.

Step four: when that debt is cleared, take the full amount you were paying on it -- the minimum plus the extra -- and add it to the payment on the next smallest debt. The payment snowballs as each debt is eliminated.

Step five: repeat until all debts are cleared.

The defining feature of the snowball method is the psychological payoff of seeing individual debts hit zero. Clearing a debt, however small, produces a tangible sense of progress. It reduces the number of accounts you are managing. It proves that the plan is working. And for many people, this momentum is what makes the difference between following through and quietly abandoning the strategy after three months.

Research supports this. A study published in the Journal of Consumer Research found that people who focused on individual debt elimination -- rather than total debt reduction -- were more motivated and more likely to complete their repayment.

The Debt Avalanche Method - How It Works

The debt avalanche method optimises for total interest paid rather than number of debts cleared.

Step one: list all your debts from highest interest rate to lowest, regardless of outstanding balance.

Step two: pay the minimum due on every debt except the one with the highest interest rate.

Step three: direct every available rupee above the minimum payments toward the highest-interest debt, until it is cleared.

Step four: when that debt is cleared, redirect its full payment, minimum plus extra, toward the next highest-interest debt.

Step five: repeat until all debts are cleared.

In India, this typically means targeting credit card debt first, since credit cards charge 36% to 42% annual interest -- far higher than personal loans, vehicle loans, or home loans. Every rupee applied to a credit card balance eliminates the most expensive debt first.

The avalanche method saves more money in total interest paid. On large debt amounts or debts with widely different interest rates, the saving can be significant -- sometimes tens of thousands of rupees over the life of the repayment. This is why, purely in financial terms, the avalanche is the superior strategy.

Its limitation is psychological. When the highest-interest debt also happens to be the largest balance, progress can feel slow. Months may pass before any individual debt is cleared. Without the quick wins that the snowball provides, some people lose momentum and abandon the plan.

A Worked Example with Indian Numbers

Consider a person with three debts:

Credit card outstanding: Rs. 80,000 at 40% annual interest. Minimum due: Rs. 4,000 per month.

Personal loan outstanding: Rs. 1,50,000 at 16% annual interest. EMI: Rs. 5,000 per month.

Two-wheeler loan outstanding: Rs. 40,000 at 12% annual interest. EMI: Rs. 2,500 per month.

Total minimum payments: Rs. 11,500 per month. Available extra for debt repayment each month after all minimums: Rs. 5,000.

Under the snowball method, the extra Rs. 5,000 goes to the two-wheeler loan first (smallest balance: Rs. 40,000). This clears in roughly 6 to 7 months. Then the freed-up Rs. 7,500 (Rs. 2,500 original EMI plus Rs. 5,000 extra) goes to the credit card. Then everything goes to the personal loan.

Under the avalanche method, the extra Rs. 5,000 goes to the credit card first (highest interest: 40%). The credit card takes longer to clear given the higher balance, but the total interest saved over the full repayment period is meaningfully higher than under the snowball approach.

The key variable: the snowball clears one debt much faster and produces an early win. The avalanche saves more money over the full timeline. Neither is wrong.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Snowball vs Avalanche - The Honest Comparison

The honest answer to which method is better is: the one you will actually complete.

Both methods produce debt freedom if followed consistently. The avalanche produces it at a lower total cost. The snowball produces it with higher sustained motivation.

The relevant question is not which method is theoretically optimal. It is which method matches your psychological reality. If you have the discipline and patience to stay on track through months of progress that is invisible in terms of debt count, the avalanche rewards that discipline with meaningful interest savings. If you need to see debts disappear to stay motivated, the snowball keeps you in the game long enough for the later, larger wins to arrive.

For most people with multiple debts at very different interest rates -- particularly credit card debt at 36% to 40% alongside lower-rate loans -- a hybrid approach often makes the most practical sense: use the avalanche logic for the first target (clear the most expensive debt), but if a very small debt sits alongside a large high-interest one, clear the small one first to reduce complexity, then pivot to interest-rate priority.

Legal Note: Before aggressively paying down any loan in India, check whether it carries a prepayment penalty. Under RBI guidelines, prepayment charges on floating-rate retail loans have been restricted. However, most personal loans in India are fixed-rate products, which may carry foreclosure charges of 2% to 5% of the outstanding principal. Factor this into your calculation before deciding whether early payoff of a particular loan makes financial sense. [Know your rights as a borrower]

How to Choose the Right Method for You

Use the avalanche method if: your credit card debt carries significantly higher interest than your other debts, you have a track record of financial discipline even without visible short-term progress, and the total interest savings over the repayment period are substantial relative to your total debt.

Use the snowball method if: you have several small debts that can realistically be cleared within a few months, you find motivation difficult to sustain without visible wins, and the difference in interest rates between your debts is not dramatic enough for the avalanche to produce a significantly different financial outcome.

Use a hybrid if: one or two very small debts can be cleared quickly at minimal financial cost, after which you switch to interest-rate priority. This provides an early win without significantly compromising the overall strategy.

In all cases: stop adding to the debt while executing either method. A repayment strategy applied to a balance that keeps growing will never reach zero.

What to Do Before You Start Either Method

Neither method works without this foundation.

First, know the exact numbers. Total outstanding on every debt. The interest rate on each. The minimum monthly payment on each. Write them all down in one place. Many people are surprised by the total when they see it clearly for the first time.

Second, find the extra repayment capacity. Review last month's spending. Identify every discretionary rupee that can be redirected toward debt repayment without creating a new problem. This number may be small at first. Even Rs. 1,000 to Rs. 2,000 per month, applied consistently, makes a difference over time.

Third, set up auto-pay for all minimums. Every missed minimum payment damages your CIBIL score and adds late fees. Automating minimums removes the risk of accidentally derailing the strategy because of a forgotten due date.

Fourth, commit to not taking new debt. Both methods are built on a closed system -- the same debts being paid down month after month. Introducing new debt reopens the system and extends the timeline indefinitely.

When Neither Method Is Enough

Both the snowball and avalanche methods are debt repayment strategies. They work when there is enough income above minimum payments to make meaningful extra contributions. When that condition is not met -- when the minimum payments alone consume too much of income to leave any room for extra repayment -- neither strategy can function.

This is not a failure of discipline or motivation. It is a mathematical reality. When debt load exceeds what income can service, a repayment strategy is not the answer. The debt structure itself needs to change.

In this situation, debt consolidation, combining multiple obligations into one lower monthly payment -- can create the breathing room that makes a repayment strategy possible. Or, where total debt genuinely exceeds what can be repaid on any realistic timeline, debt resolution -- settling with creditors for less than the full outstanding amount, provides the only real path to becoming debt-free.

FREED helps people identify which situation they are actually in -- and then executes the right solution. The first consultation is free and requires no commitment.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions