Credit Card Application: What Do Too Many Rejections Mean?

Got rejected for a credit card — again? Each rejection hurts more than just your pride. It also hurts your CIBIL score. Here's exactly why banks say no, what multiple rejections signal, and how to fix it.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Every credit card application triggers a hard inquiry on your CIBIL report, which lowers your score slightly.

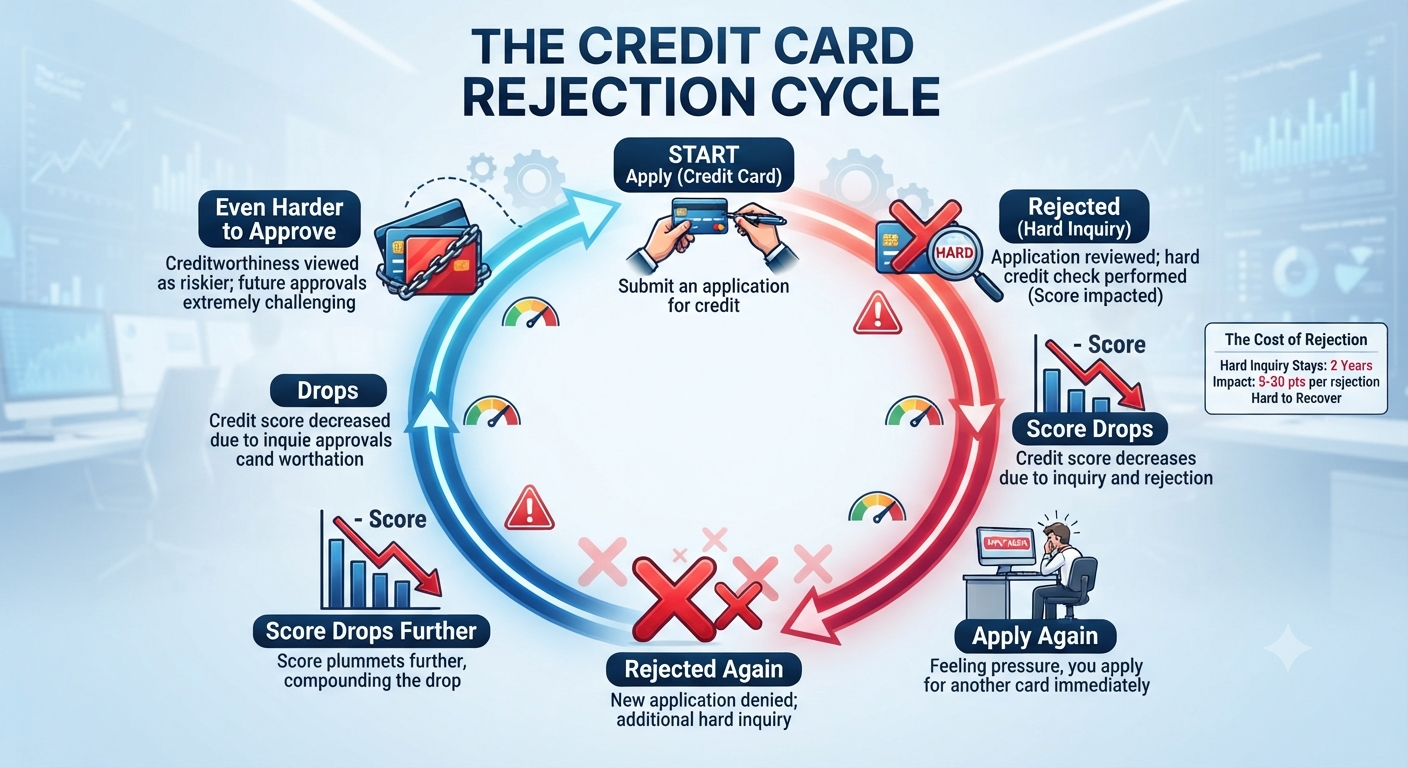

Multiple rejections in a short period create a damaging cycle: each rejection triggers another inquiry, which lowers the score further, making the next application more likely to be rejected.

A CIBIL score below 700 significantly reduces approval chances at most major banks.

No credit history (score of -1 or 0) is treated as high risk, the same as a poor score.

If existing debt is driving the rejections, addressing the debt is the only lasting fix. FREED can help.

Why Credit Card Applications Get Rejected

Applying for a credit card in India has never been easier. A few taps on a bank app and the application is submitted in minutes.

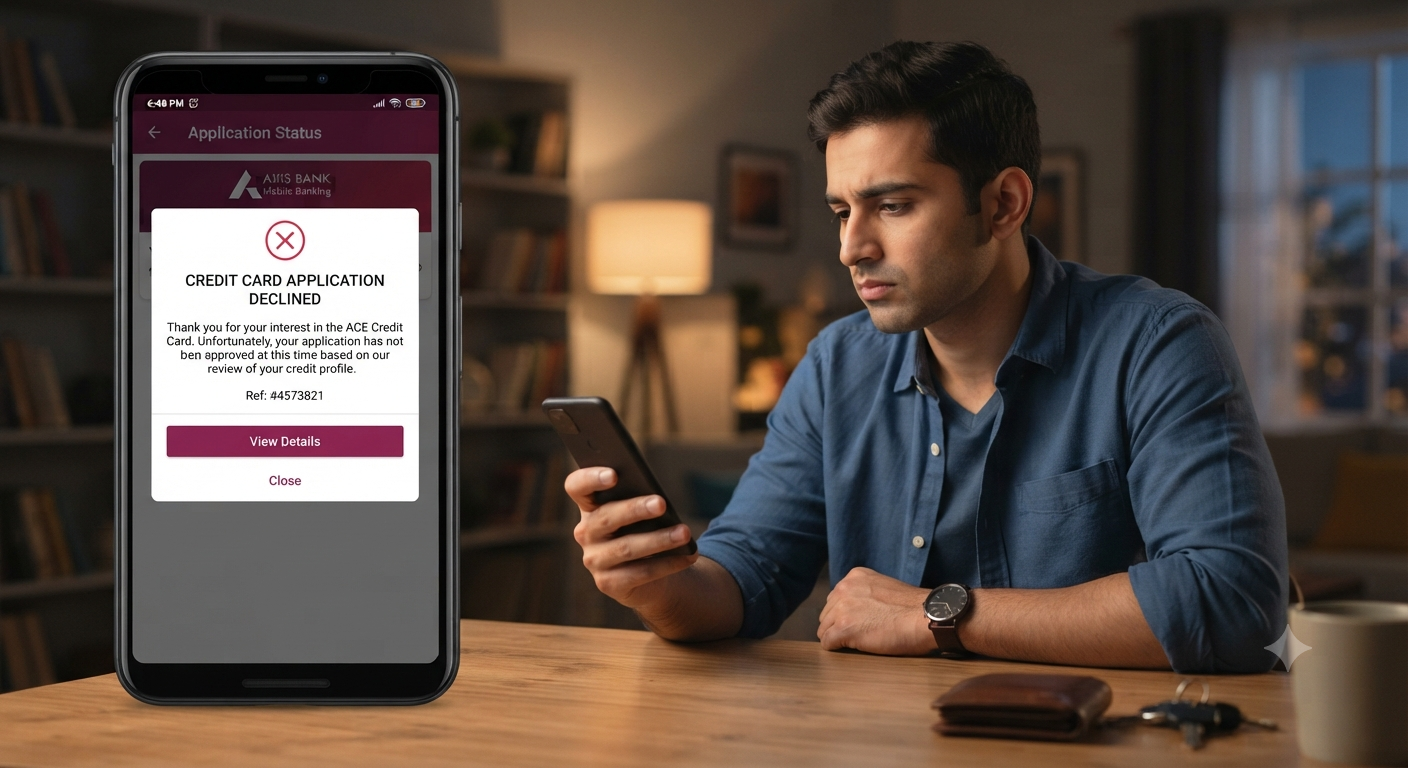

But easy to apply doesn't mean easy to approve. Banks run a detailed check before issuing any credit card and they can decline without giving you a detailed explanation.

What most people don't realise is that each rejection has two costs: the obvious one (not getting the card) and the hidden one (a hard inquiry on your CIBIL report that drops your score, making the next application harder).

Understanding why banks reject applications and what multiple rejections actually signal, is the first step to fixing the problem.

Debt or a poor CIBIL score blocking your credit card applications?

Talk to a FREED Expert It's Free.

Connect with FREED ExpertReason 1: Low CIBIL Score

Your CIBIL score is the first thing most banks check. It tells them in a single number, how reliable you've been with credit in the past.

Most major banks in India require a minimum score of 700–750 for credit card approval. Below 700, you're placed in the higher-risk category. Below 650, most mainstream card applications will be declined outright.

Your CIBIL score is influenced by five main factors:

Factor | Impact Level |

Payment history (on-time vs. late/missed payments) | High |

Credit utilisation (how much of your limit you're using) | High |

Credit age (how long you've had credit) | Medium |

Credit mix (types of credit — cards, loans, etc.) | Medium |

Credit enquiries (how many applications you've made) | Low–Medium |

If your score is low, a new credit card application is unlikely to succeed — and the hard inquiry from the attempt will lower the score further.

What to do: Check your CIBIL report before applying. If your score is below 700, focus on rebuilding it first — pay all dues on time, reduce outstanding balances, and avoid new applications for 6–12 months.

Reason 2: Too Many Credit Enquiries

Every time you apply for a credit card or loan, the bank runs a hard inquiry on your CIBIL report. This is recorded and each one causes a small drop in your score.

One or two inquiries spread across several months is normal. But if you've applied for three or four cards within a few months, perhaps after being rejected and trying again with a different bank, the pattern looks alarming to lenders.

Multiple hard inquiries in a short window signal something very specific to banks: financial stress. It suggests you urgently need credit, may be struggling financially, and are applying widely in the hope of getting approved somewhere.

This is exactly the profile banks try to avoid.

What to do: Stop applying immediately after a rejection. Each new application makes things worse, not better. Check your CIBIL report to understand why you were rejected, fix the root cause, and wait at least 3–6 months before your next application.

FREED Expert Tip:

Before applying for any credit card, check your CIBIL score yourself first this is a soft inquiry and does not affect your score at all. Only apply if your score is in a range where approval is realistic for that specific card. A targeted, well-timed single application is far better than multiple scattered ones.

Check Your Credit Score FreeReason 3: No Credit History

A CIBIL score of -1 or 0 means the bureau has no credit record for you, no loans, no credit cards, no history to evaluate.

Counterintuitively, this can be as problematic as a poor score. Banks have no data to assess your creditworthiness. With no track record, you're an unknown risk and many banks default to declining unknown risks.

This is a common problem for young professionals applying for their first credit card, or for people who have only ever used debit cards and cash.

What to do: Build credit history gradually. A secured credit card issued against a fixed deposit, is the most accessible entry point. Some banks also offer entry-level credit cards for salaried individuals with no prior credit history. Use the card for small, regular purchases, pay the full bill every month, and your credit history begins to build within 3–6 months.

Reason 4: Income Below the Bank's Threshold

Every credit card has a minimum income requirement. This varies by bank and card type, entry-level cards may require ₹15,000–₹20,000 per month; premium cards often require ₹50,000 or more.

If your declared income falls below the threshold, the application is declined regardless of your credit score.

There's a related issue: income that cannot be verified. Freelancers, self-employed individuals, and those in informal employment often struggle here not because their income is insufficient, but because they lack the documentation banks require (salary slips, Form 16, ITR filings, or bank statements showing regular salary credits).

What to do: Check the minimum income requirements before applying, most banks publish these. For self-employed applicants, maintain clean bank statements that clearly show regular income, file ITRs every year, and choose cards from banks or NBFCs that specifically serve self-employed or gig economy customers.

Reason 5: High Existing Debt or Too Many Cards

If your CIBIL report already shows multiple active credit cards, especially with high outstanding balances banks are reluctant to add another.

The reasoning is straightforward: you are already heavily exposed to credit. Adding another card increases the risk that you'll be unable to service the combined debt. If any existing card is maxed out or has a history of late payments, the concern is amplified.

Banks also look at your FOIR, Fixed Obligation to Income Ratio. If your existing EMIs and minimum credit card payments already consume 50–60% of your monthly income, your application for additional credit will almost certainly be declined.

What to do: Before applying for a new card, pay down existing card balances as much as possible. Aim to get your credit utilisation below 30% across all cards. If you have loans with high EMIs, assess whether any can be closed or consolidated before applying. A lower debt burden makes you significantly more attractive to card issuers.

What the Law Says:

Under RBI guidelines, credit card issuers are required to assess the repayment capacity of applicants before issuing a card — they cannot simply issue credit to anyone who applies. If you believe a card was issued to you irresponsibly (without adequate income or creditworthiness checks), you have the right to raise a complaint with the RBI Banking Ombudsman. Equally, if you're declined, issuers are not required to provide detailed reasons — but you can request your CIBIL report to understand what they saw.

Know your rights as a credit card applicant →Reason 6: Employment or Verification Issues

Banks verify employment status before approving a credit card and certain employment profiles are treated as higher risk.

Common verification-related rejection reasons:

Company not on the bank's approved list: Banks maintain internal lists of employers they consider stable. Working at a smaller company, a startup, or an unregistered business may result in rejection even with adequate income.

Irregular or short employment history: Frequent job changes, especially if you've been at your current employer for less than 6–12 months, raise concerns about income stability.

Address verification failure: If a field agent cannot verify your address (because you were unavailable, your address is incorrect, or you've recently moved), the application may be declined on this ground alone.

What to do: Ensure your address on the application matches your KYC documents exactly. Be available for verification visits if required. If your employer is a smaller company, consider applying to banks or NBFCs that serve a broader range of employers or build your case with a secured card first.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Reason 7: Errors in the Application Form

This is the most avoidable reason for rejection and more common than it should be.

Minor errors, a wrong PAN number, a mismatched name, an incorrect date of birth, an address that doesn't match your Aadhaar, can trigger automatic rejection. Incomplete fields, missing documents, or inconsistencies between what you've declared and what the bank finds in your CIBIL report also cause declines.

What to do: Fill application forms carefully and cross-check every field before submitting. Online applications allow you to review before submission use that opportunity. Ensure your declared income, employment details, and address match your supporting documents precisely.

What Multiple Rejections Actually Signal

Here is what banks see when they look at an applicant who has been rejected multiple times in a short period:

A string of hard inquiries. Each rejection left a mark. Multiple marks in close succession is a pattern that no bank wants to extend credit to.

A financial profile that wasn't approved elsewhere. Banks know other banks run similar checks. If three or four lenders declined you, the applicant is in a risk category that banks are collectively avoiding.

Possible financial stress. The most common reason people apply for multiple cards quickly is that they need credit urgently, which is the signal banks most want to avoid.

Multiple rejections do not just indicate a problem. They create one. Each hard inquiry makes the next application harder. The cycle compounds until the applicant stops applying entirely and focuses on rebuilding.

What to Do After a Rejection - Step by Step

If you've been rejected, once or multiple times, here's the right sequence:

Step 1: Stop applying immediately. Every new application is another hard inquiry. Give your score time to stabilise.

Step 2: Check your CIBIL report. Understand exactly what the bank saw. Look for errors, check your score, review your payment history and utilisation. FREED's Credit Insights tool can help you read and understand your report.

Step 3: Dispute any errors. If you find incorrect information, a payment marked late that was paid on time, a closed account still showing as open, raise a dispute with the bureau immediately. Errors can significantly suppress your score.

Step 4: Address the root cause. Low score? Pay dues on time for 6–12 months. High utilisation? Pay down balances. Too many enquiries? Wait it out while improving your profile.

Step 5: Consider a secured credit card. If you need a credit card for building history or daily use, a secured card (against an FD) is far easier to get approved for and serves the same credit-building purpose as a regular card.

Step 6: Apply again selectively only when ready. Once your score is above 700 and your profile is stronger, apply for one card at a time, choosing an issuer and product that matches your profile. Do not apply speculatively.

When Debt Is the Deeper Issue

Many people face credit card rejections not because of a single factor but because existing debt has damaged their entire credit profile - score, utilisation, FOIR, and payment history all at once.

In these cases, applying for more credit is not the answer. The debt itself needs to be addressed.

FREED helps people in exactly this position. Through Debt Consolidation, we reduce the monthly EMI burden so your FOIR improves and payments become manageable. Through Debt Resolution, we help settle outstanding dues — with proper documentation that supports credit report correction afterward. Both approaches improve the underlying profile that card issuers see.

Over 60,000 Indians have used FREED to get out of this situation. The first conversation is free.

Debt causing repeated credit card rejections?

Talk to a FREED Expert Free, no pressure.

Connect with FREED Expert →FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions