Your go-to resource for financial wellbeing

Your resource for financial wellbeing

Our Latest Blogs

Latest Blogs

Debt Management

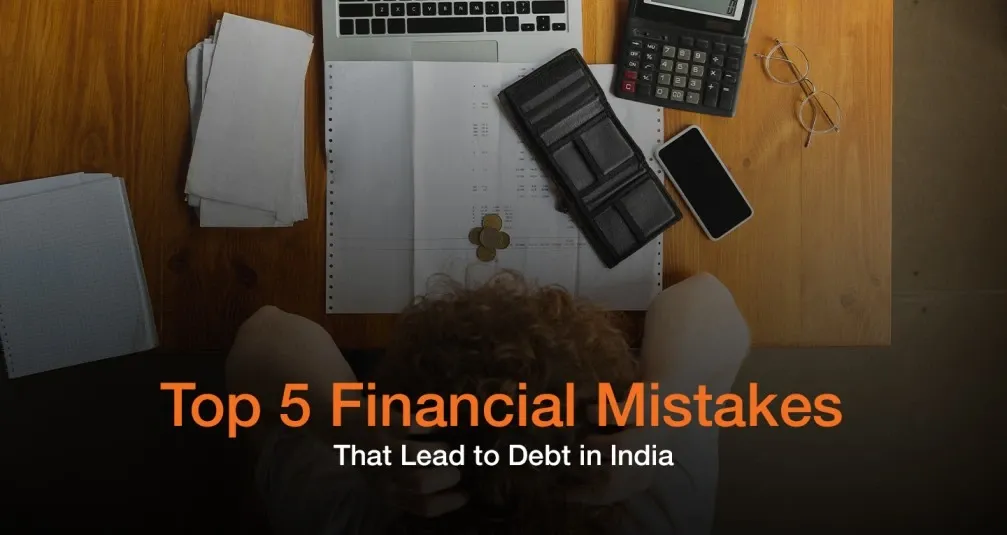

Top 5 Financial Mistakes That Lead to Debt in India

Most debt in India does not begin with one large, reckless decision. It builds through five specific, common financial mistakes that feel manageable at the time. Here is what they are, why they lead to debt so reliably, and how to avoid or reverse each one.

By FREED India | 11 August 2026

Debt Management

Top 12 Financial Mistakes Business Owners Often Make

Running a business and managing personal finances well are two different skills, and many business owners let the first one quietly damage the second. Here are 12 specific financial mistakes business owners commonly make, and what to do differently.

By FREED India | 11 August 2026

Debt Management

Top 10 Ways to Manage Your Debt

Managing debt well is not about one big fix. It is a set of specific, practical practices, prioritisation, tracking, negotiation, and knowing when to seek help, that together keep debt from controlling your finances. Here are the 10 that actually make a measurable difference.

By FREED India | 11 August 2026

Recommended Reads

Debt Management

Top 5 Financial Mistakes That Lead to Debt in India

By FREED India | 11 August 2026

Debt Management

Top 12 Financial Mistakes Business Owners Often Make

By FREED India | 11 August 2026

Debt Management

Top 10 Ways to Manage Your Debt

By FREED India | 11 August 2026

Debt Management

Top 10 benefits of good credit score

By FREED India | 11 August 2026

Debt Management

Things to Know About Credit Cards

By FREED India | 11 August 2026

Debt Management

The Urgent Need for Better Financial Planning

By FREED India | 10 August 2026

Debt Management

Who taught you to be scared of your debt load?

By FREED India | 10 August 2026

Debt Management

The Real Difference Between Savings and Investments

By FREED India | 10 August 2026

Debt Management

The Psychology of Overspending

By FREED India | 10 August 2026