3 Credit Card Facts That Can Change Your Life

Most people use credit cards without really understanding how they work. These three facts change that - and once you know them, you will never use your card the same way again.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Paying only the minimum due on a credit card is one of the most expensive financial mistakes a person can make. At 36 to 42% annual interest, the outstanding barely reduces while interest compounds month after month.

Your credit card outstanding balance is reported to credit bureaus every 15 days. High utilisation - using more than 30% of your limit - actively reduces your CIBIL score even if you pay on time.

The grace period - the interest-free window of up to 50 days - only works if you paid your previous month's bill in full. One month of partial payment cancels it entirely.

These three facts, once understood, change how most people use credit cards - and prevent the majority of credit card debt situations.

If credit card debt has already become unmanageable, FREED can help through consolidation or settlement.

Why Most People Misunderstand Credit Cards

Credit cards are designed to be easy to use. The application is instant. The limit feels like available money. The minimum due looks like a manageable monthly cost.

None of this is accidental. Credit card companies make money from the interest charged on balances that are not paid in full. The more convenient the card feels to use without fully repaying, the more interest is collected.

Understanding how credit cards actually work - not how they are marketed to work - is one of the most valuable pieces of financial knowledge available. And it comes down to three specific facts.

Fact 1: The Minimum Due is Not a Payment - It is a Trap

Every month your credit card statement shows two numbers.

Total Amount Due - what you actually owe. Minimum Amount Due - typically 5% of the total outstanding.

Most people pay the minimum and feel like they have done the right thing. They have not. They have done exactly what the bank designed the minimum to encourage.

Here is what actually happens when you pay only the minimum:

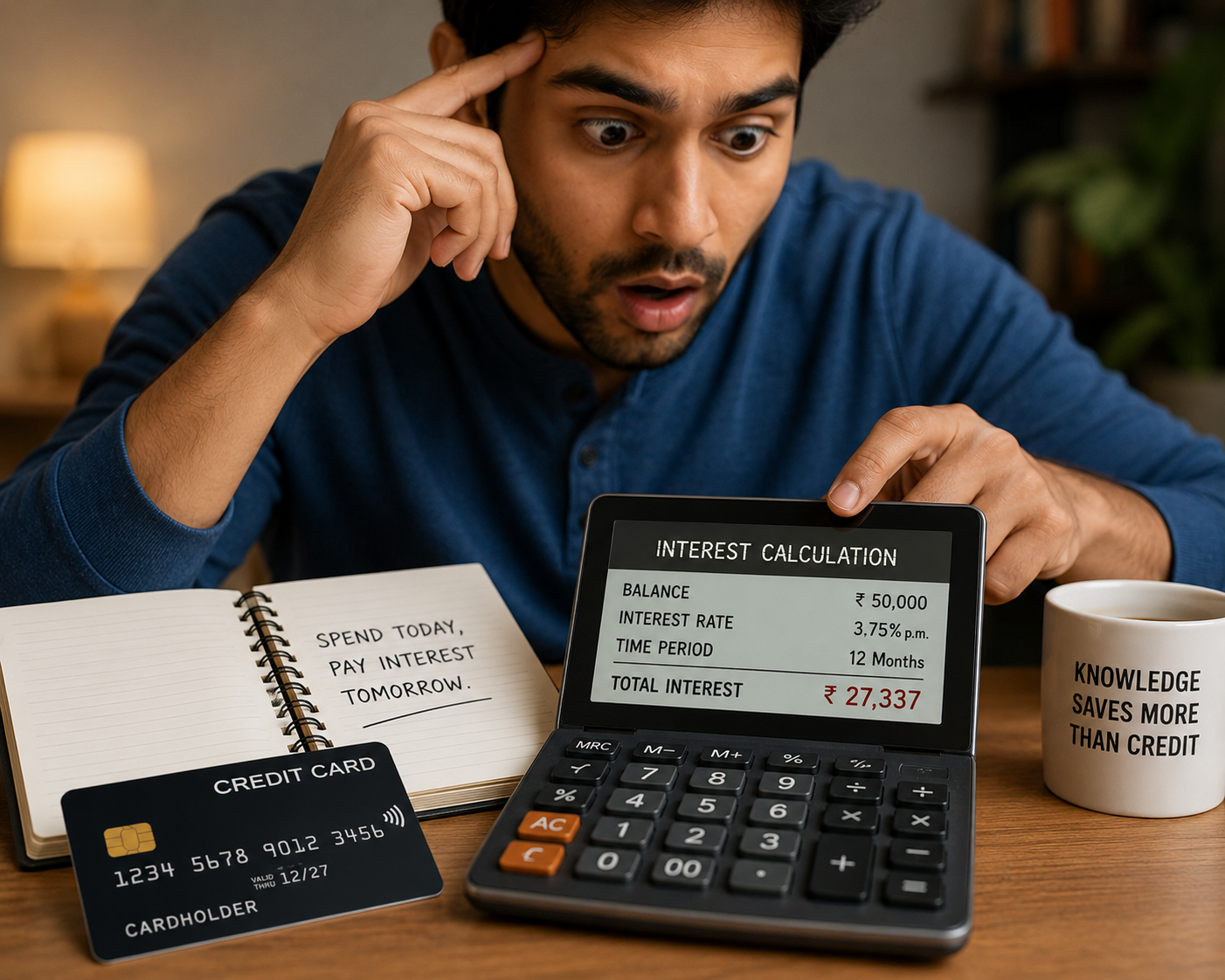

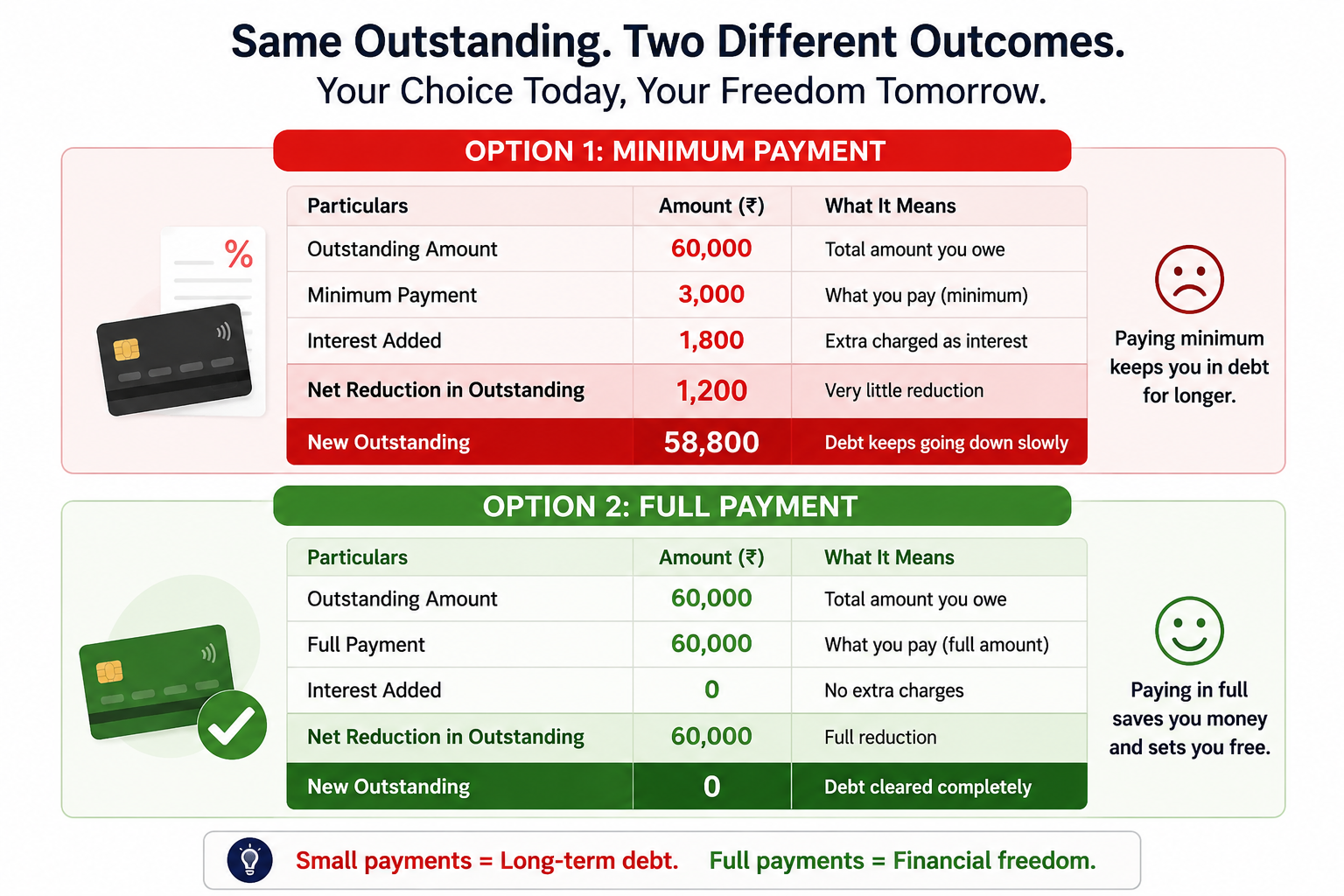

The remaining 95% of your outstanding carries forward with full interest - at 36 to 42% per year. On Rs 60,000 outstanding, that is approximately Rs 1,800 added in interest in a single month. Your next month's outstanding is Rs 59,800 before you even swipe the card again - because the Rs 3,000 minimum you paid was almost entirely consumed by the new interest.

At this pace, clearing Rs 60,000 of credit card debt by paying only the minimum takes over 10 years. And you end up paying close to Rs 1,80,000 in total - three times what you originally owed.

The minimum due exists to keep your account active. It was never designed to help you get out of debt. Always pay the full outstanding amount. Every month. Without exception.

Fact 2: Your Credit Card Affects Your CIBIL Score Every Single Month

Many people think their credit card only affects their credit score if they miss a payment. That is not true.

Your credit card outstanding balance is reported to credit bureaus by your bank every 15 days - as per updated RBI guidelines effective 2025. This means your credit utilisation ratio - how much of your credit limit you are using - is updated on your CIBIL report twice a month.

Credit utilisation is 30% of your CIBIL score. It is the second biggest factor after payment history.

If your credit card limit is Rs 1,00,000 and your outstanding is Rs 75,000 - your utilisation is 75%. That is actively hurting your score every single reporting cycle - even if you have never missed a payment in your life.

The recommended range is below 30%. At Rs 1,00,000 limit, that means keeping your outstanding below Rs 30,000.

This means two things practically. First, you should aim to pay down your outstanding as quickly as possible - not just manage the minimum. Second, you should never let your spending routinely approach your credit card limit.

A high outstanding on your credit card is not just a financial cost. It is a CIBIL score cost - and that affects your ability to get loans, at what interest rate, and on what terms - for years.

FREED Expert Tip

If you want to reduce your credit card utilisation quickly without paying more, call your bank and request a credit limit increase. If approved, your outstanding stays the same but your limit is higher - and your utilisation ratio drops immediately. This can improve your CIBIL score within one reporting cycle without paying a single extra rupee. Use this strategically - and do not increase spending to match the new limit.

Enroll NowFact 3: The Grace Period Only Works if You Paid Last Month's Bill in Full

This is the fact most credit card users in India do not know - and it costs them enormously.

The grace period is the interest-free window on your credit card - typically 20 to 50 days between your billing cycle end and your payment due date. During this window, if you pay the full outstanding, you owe zero interest on your purchases. The bank has effectively given you free short-term credit.

But here is the condition most people miss: the grace period only applies if you paid your previous month's bill in full.

If you paid only the minimum due last month - or any amount less than the full outstanding - you lose the grace period entirely for the current month. Every new purchase you make attracts interest from the very day of the transaction. Not from the due date. From day one.

This means that the moment you start paying only the minimum, every subsequent purchase becomes immediately expensive - even if you plan to pay it off soon. The bank starts charging interest from the moment you swipe.

This is why one month of minimum payment can set off a chain reaction. Month one: pay minimum, lose grace period. Month two: new purchases attract day-one interest, outstanding grows faster. Month three: the bill is even harder to pay in full. The cycle deepens.

Breaking this cycle requires paying the full outstanding - even if it takes one or two difficult months to do so. Once paid in full, the grace period is restored and the card becomes free again.

What the Law Says

Under RBI's Fair Practices Code, credit card issuers must clearly show on every monthly statement the total interest cost if you pay only the minimum due - including how long it will take to clear the balance at that rate. If your credit card statement does not include this information, your bank is not meeting RBI's transparency requirements. You have the right to request a full written breakdown of how your interest is calculated at any time.

Enroll NowHow to Use a Credit Card Correctly

These three facts together point to one simple operating principle for credit cards.

Use the card for planned purchases you have already budgeted for. Pay the full outstanding amount before the due date every month. Keep your total outstanding consistently below 30% of your credit limit.

That is it. Follow these three rules and a credit card costs you nothing in interest, builds your CIBIL score, and provides a useful 20 to 50 day float on your spending.

Set up auto-debit for the full statement amount. This single action makes all three rules automatic.

When Credit Card Debt Has Already Become Unmanageable

If you are reading this and realising that your credit card situation is already past the point where these tips apply - the outstanding has grown too large, the minimum payments are barely making a dent, the interest is compounding faster than you can pay - you are not alone.

This situation is very common. And there are real, structured solutions.

If you can still pay but the outstanding is large and growing: FREED's Debt Consolidation Program combines your credit card balances into one personal loan at 14 to 20% interest - dramatically lower than the 36 to 42% you are currently paying. One EMI. One due date. More of each payment reducing the actual debt.

If you have already missed payments and cannot repay the full amount: FREED's Debt Resolution Program negotiates with your credit card company to settle the debt for less than you owe. On average, FREED clients settle at 56% less than the original outstanding.

Both programs include FREED Shield - which stops recovery harassment the moment you enrol.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions