10 Strategies to Avoid Getting into Debt

Debt does not happen overnight. It builds slowly - one missed saving, one impulse purchase, one loan taken without a plan. These 10 strategies help you stay ahead of debt before it starts.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Most debt does not come from recklessness - it comes from the absence of a plan. A budget, an emergency fund, and disciplined credit card use prevent the majority of debt situations.

Lifestyle inflation - spending more as you earn more - is one of the most common and least discussed causes of debt among working Indians today.

Understanding the true cost of borrowing before signing any loan agreement protects you from surprises that become unmanageable over time.

If debt has already begun, seeking help early gives you far more options than waiting until the situation becomes a crisis.

FREED helps people both prevent and resolve debt - through free counselling, debt consolidation, and debt resolution programs.

Why Do People Fall Into Debt in the First Place?

Understanding the cause is the first step to prevention.

Most people do not get into debt because they are irresponsible. They get into debt because they lack specific habits and systems - things nobody really taught them. A job loss comes and there are no savings to fall back on. A medical emergency happens and the credit card is the only option. Lifestyle spending creeps up month by month until the salary barely covers the minimum dues.

These situations are predictable. And most of them are preventable - with the right habits in place before the crisis hits.

Already in debt and looking for a way out?

Talk to a FREED Expert for free - we will look at your situation and tell you what is realistically possible.

Connect with FREED ExpertStrategy 1: Build a Monthly Budget

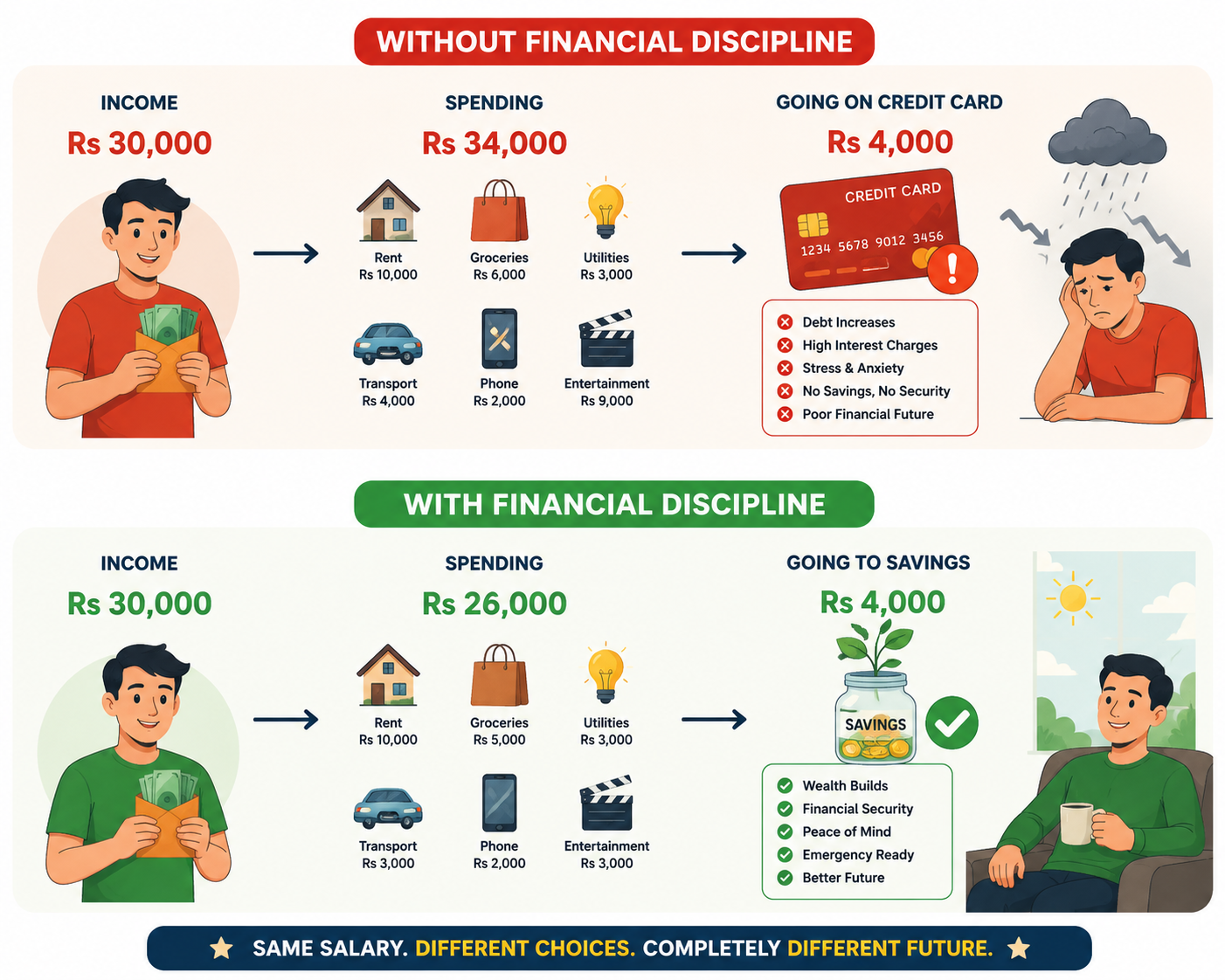

A budget is not a restriction. It is a plan. It tells your money where to go before the month begins - instead of you wondering where it went at the end.

Write your monthly take-home income. List all fixed expenses - rent, EMIs, school fees, utilities. List variable expenses - groceries, travel, eating out, entertainment. Whatever is left is available for savings and debt repayment.

Even a rough budget done once a month prevents the most common cause of debt - untracked spending that quietly exceeds income over several months.

The simplest budget framework is the 50-30-20 rule. 50% of income goes to needs, 30% to wants, and 20% to savings and debt repayment. If your EMIs are already consuming more than 50%, address the debt situation first before trying to apply this framework.

Strategy 2: Create an Emergency Fund

This is the single most powerful debt-prevention tool available.

Most debt situations start with one unexpected expense - a hospital bill, a job loss, a vehicle repair - and no savings to cover it. The credit card or personal loan becomes the only option. The EMI starts. If it overlaps with another EMI, the burden grows. The cycle begins.

An emergency fund breaks this chain at the source.

Start with a target of Rs 10,000. Save Rs 500 to Rs 1,000 per month in a separate account. Do not touch it unless there is a genuine emergency. Once you reach Rs 10,000, aim for one month of expenses. Then three months.

This fund is not exciting. But it is the difference between a difficult month and the beginning of a debt spiral.

Strategy 3: Never Spend More Than You Earn

This sounds obvious. It is harder than it sounds.

With credit cards, BNPL apps, and instant personal loans all available in seconds on a phone, spending more than you earn has never been easier. The consequences arrive later - in EMIs, in growing outstanding balances, in collection calls.

The rule is simple: if the money is not in your savings account, do not spend it. Use cash or debit for daily expenses. If the card is swiped, the full amount must be paid before the due date. No exceptions.

Strategy 4: Pay Credit Card Dues in Full Every Month

Credit card interest in India is 36 to 42% per year. That is the highest rate on any common financial product.

Every month you carry a balance - paying only the minimum - new interest is added. Your outstanding grows. The minimum due next month is slightly higher. The cycle is slow at first, and then very fast.

Paying in full every month means you pay zero interest. The card becomes a free short-term credit tool rather than an expensive debt trap.

Set up auto-debit for the full statement amount on every card. Not the minimum due - the full outstanding.

FREED Expert Tip

Before applying for any credit card or loan, ask the lender for the Annual Percentage Rate - not just the interest rate. The APR includes all fees and charges and shows the true cost of borrowing. It is almost always higher than the advertised rate. Knowing the real cost before you borrow changes how you think about whether the loan is actually necessary.

Enroll NowStrategy 5: Avoid Lifestyle Inflation

Lifestyle inflation is spending more as you earn more - and it is one of the most common hidden causes of debt among working Indians.

You get a raise. The rent goes up. The dining out becomes more frequent. The phone upgrade happens. The holiday gets booked. By the time the next year arrives, the higher salary feels just as tight as the old one - but with bigger financial commitments.

When income rises, the healthy response is to increase savings first, not spending. Routing 50% of every increment to savings before adjusting lifestyle preserves financial stability as earnings grow.

Strategy 6: Understand the True Cost of Borrowing

Before taking any loan, calculate the total amount you will repay - not just the monthly EMI.

A personal loan of Rs 3,00,000 at 18% interest over 3 years has an EMI of approximately Rs 10,850. That looks manageable. But the total repaid is approximately Rs 3,90,600. You pay Rs 90,600 in interest - 30% above what you borrowed.

Understanding this before borrowing changes the calculation. It makes you more selective about what you borrow for - and more motivated to repay quickly.

Always ask: is what I am borrowing for worth paying 20 to 30% more for over the loan tenure?

Strategy 7: Think Carefully Before Co-Signing a Loan

When you co-sign a loan for a family member or friend, you become equally responsible for the repayment. If they default, the EMI falls to you. The late payment marks go on your credit report. Your CIBIL score drops.

This is not hypothetical. It happens regularly to people who agreed to help a family member and did not fully understand the obligation.

Before agreeing to co-sign any loan, be completely certain that you are prepared and able to repay the full amount if the primary borrower cannot. If you are not - do not co-sign, regardless of the relationship or the pressure you feel.

Strategy 8: Build More Than One Source of Income

Relying on a single salary is a financial risk. If that income stops - through job loss, medical incapacity, or business failure - debt becomes almost inevitable without savings to bridge the gap.

A second income source does not have to be large. Rs 2,000 to Rs 5,000 per month from freelancing, tutoring, renting a space, or a small weekend business changes the equation significantly.

It accelerates savings, builds resilience, and reduces the pressure on a single salary to cover everything.

What the Law Says

Under RBI's Fair Practices Code, all lenders must disclose the Annual Percentage Rate - which includes the interest rate and all fees - before you sign any loan agreement. You have a legal right to this information before committing to any loan. Always ask for the APR in writing before signing. A loan that looks affordable based on the advertised rate may be significantly more expensive once all charges are included.

Enroll NowStrategy 9: Review Your Finances Every Month

A monthly financial review takes 15 minutes and prevents months of problems.

Once a month, check your bank account balance, your credit card outstanding on every card, your total EMIs as a percentage of income, and your savings balance. Compare to last month. Look for anything moving in the wrong direction.

Early detection makes everything easier to fix. A credit card outstanding that has grown by Rs 5,000 over three months is easy to address. The same Rs 5,000 grown to Rs 50,000 over two years - with compound interest - is a serious problem.

Strategy 10: Seek Help Early - Not After the Crisis

The most common mistake people make with debt is waiting too long to ask for help.

By the time most people contact a debt counsellor, they have been struggling for 6 to 12 months already. Options have narrowed. Scores have dropped. The stress has compounded.

Seeking help early - when debt first starts to feel uncomfortable - keeps more options open. Restructuring is easier before default. Settlement terms are better before the bank has written off hope of recovery. Consolidation is available before the CIBIL score has dropped too far.

If your total EMIs are more than 40% of your monthly income - that is the signal. Do not wait for it to become 70%.

FREED's first consultation is free. One call tells you where you stand and what your realistic options are.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions