The Early Signs of Debt Trap and Solution

A debt trap rarely announces itself. It builds through small, familiar warning signs, minimum payments, rising balances, new credit covering old gaps, long before it feels unmanageable. Here is how to spot those signs early, and what to do the moment you notice them.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A debt trap is a self reinforcing cycle where borrowing is used to cover the cost of previous borrowing, rather than to cover a genuine new need, causing the total outstanding to grow even as payments continue.

The earliest signs are subtle: consistently paying only the minimum due, a credit card balance that never quite clears, and rising credit utilisation, none of which feel alarming individually.

A more advanced sign is using one form of credit to pay another, a BNPL plan to cover a credit card bill, a personal loan to clear multiple cards, which signals the cycle is actively compounding.

Catching these signs early gives access to far more options, restructuring, balance transfers, disciplined repayment, than waiting until the debt has grown significantly larger and multiple accounts are affected.

If several of these signs are already present, FREED can assess the situation and recommend consolidation or settlement before the trap deepens further.

What a Debt Trap Actually Is

A debt trap is a specific, self reinforcing pattern, not simply having debt. It occurs when borrowing is increasingly used to cover the cost of previous borrowing, interest, minimum payments, or a shortfall created by an earlier debt, rather than to cover a genuine new expense or investment.

In this pattern, the total amount owed grows even while payments continue to be made, because the payments are mostly or entirely servicing interest rather than reducing the actual outstanding principal. What makes it a trap, rather than simply a difficult financial period, is this self reinforcing quality, the debt itself generates the conditions that make it harder to escape, more interest, a lower credit score limiting better refinancing options, and less monthly income available to make real progress.

The earlier this pattern is recognised, the more options exist to interrupt it. The signs below are worth checking against honestly, since a debt trap in its early stages looks very different, and is far easier to address, than one that has been building for years.

Sign 1: You Are Only Ever Paying the Minimum Due

This is often the earliest and most common sign, and precisely because it feels responsible, "I am making my payment on time every month," it is also the one most likely to be missed.

Paying only the minimum due on a credit card, month after month, means the vast majority of the outstanding balance, typically 90 to 95%, continues to carry forward at full interest, 36 to 42% per year. The balance is not meaningfully shrinking. It is, in most cases, effectively remaining static or growing, even as payments are made consistently and on time.

The distinction that matters: making a payment is not the same as making progress. If several consecutive months have passed with only the minimum due being paid, and the outstanding balance has not visibly decreased, this is the first, quietest sign of the pattern beginning.

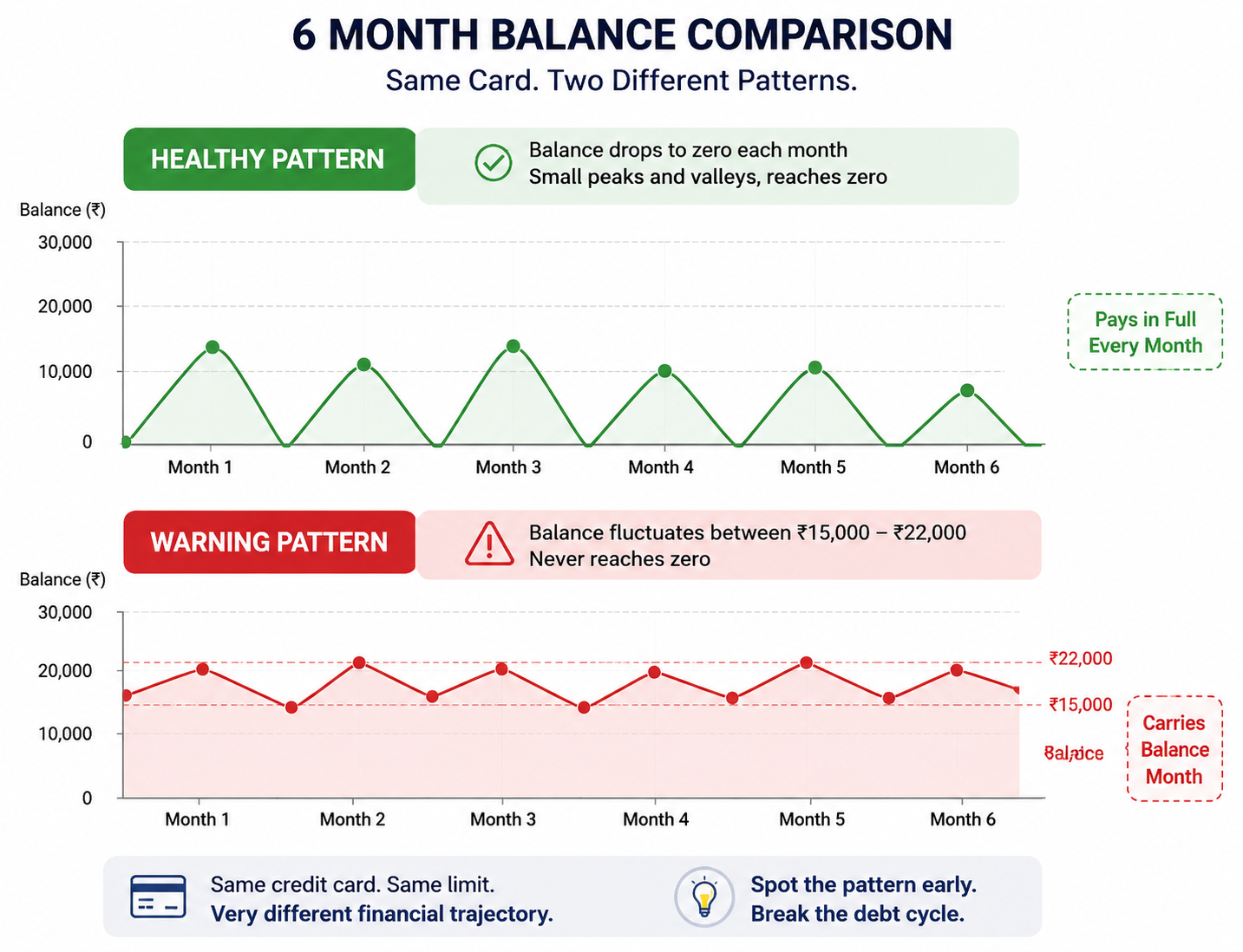

Sign 2: A Credit Card Balance Never Quite Reaches Zero

A credit card used well is cleared to zero, or close to it, every month. A specific early warning sign is a balance that persists, month after month, even if it fluctuates somewhat, sometimes a little higher, sometimes a little lower, but never actually returning to zero.

This persistent, non zero balance means interest is accruing continuously, since credit card grace periods only apply when the previous statement was paid in full. Once a balance carries over even once, interest typically applies to all new purchases immediately as well, not just the carried over amount, until the balance is fully cleared again.

A useful check: look back at the last 6 months of statements. If the balance has not returned to zero at least once in that period, this is a concrete, specific signal worth addressing directly, before it becomes a longer standing pattern.

Sign 3: You Are Using One Form of Credit to Pay Another

This sign represents a meaningful escalation from the earlier ones. It occurs when one credit product is used specifically to make a payment on another, a BNPL plan used to free up cash for a credit card bill, a cash advance taken to cover a loan EMI, a new credit card applied for specifically because an existing one is maxed out.

This pattern is significant because it indicates the debt cycle is actively compounding, rather than simply persisting. Each new credit product used this way typically carries its own interest, fees, or terms, adding a new layer of cost on top of the original debt, rather than resolving any of it.

If this pattern has occurred even once or twice, it is worth treating as a serious signal, not a one time convenience. It usually indicates that monthly cash flow has already become genuinely insufficient to service existing obligations, which is a fundamentally different, and more urgent, situation than simply carrying a balance.

Sign 4: Your Credit Utilisation Keeps Creeping Higher

Credit utilisation, the percentage of your total available credit limit currently in use, is worth tracking specifically because it tends to rise gradually and predictably as a debt trap develops, often before the person experiencing it consciously registers the trend.

A utilisation level below 30% is generally considered healthy. A rising trend, moving from 35% to 45% to 60% across consecutive months, even if each individual month's number does not feel alarming in isolation, is a clear, measurable early warning sign, and one that is also actively damaging your CIBIL score as it happens, independent of payment history.

Check utilisation specifically, not just whether payments are being made on time, since it can reveal a developing trap even when payment history still looks clean on the surface.

Sign 5: You Have Stopped Opening Your Statements

This sign is behavioural rather than numerical, and it is one of the most reliable indicators that a debt trap has moved from a financial pattern into an emotional one.

Avoiding statements, letting notification badges accumulate unread, delaying login to a specific banking app, are common responses to a growing sense that the actual numbers might be worse than they feel. This avoidance is understandable, but it also means the actual situation is no longer being tracked, which allows the underlying trend to continue unchecked and, frequently, to worsen.

If you notice a specific account or statement you have been actively avoiding opening, that avoidance itself is meaningful information, more meaningful, often, than the number would have been if you had simply looked at it directly.

Sign 6: New Purchases Feel Necessary Even When Money Is Tight

A subtler sign involves the framing used around new spending decisions during a period of financial strain. Purchases that would previously have been recognised as optional, a subscription, a dining expense, a non essential shopping item, start being mentally categorised as necessary, even while other obligations are being paid late or only partially.

This shift often reflects a specific psychological pattern where spending becomes a form of relief from the stress of the underlying financial situation, rather than a genuinely considered decision, which paradoxically deepens the situation that is causing the stress in the first place.

Noticing this shift, the mental reclassification of optional spending as necessary during a tight period, is a useful, honest check worth applying periodically, particularly during months where other financial obligations are already under strain.

Sign 7: You Are Losing Track of How Many Accounts You Actually Owe

A specific, concrete sign of an advancing debt trap is difficulty answering a simple question quickly and accurately: how many separate accounts, credit cards, loans, BNPL commitments, do you currently owe money on, and what is the total across all of them.

Someone with a small, well managed number of accounts can usually answer this within a few seconds. As a debt trap develops, the number of active accounts tends to grow, and awareness of the combined total, as opposed to each individual minimum due, tends to fade, since attention naturally narrows to whichever payment is due next, rather than the full combined picture.

If this question is genuinely difficult to answer without checking multiple apps and adding things up, that difficulty itself is a meaningful sign, and the exercise of actually calculating the answer is one of the most useful first steps available.

Sign 8: A Single Missed Payment Feels Catastrophic, Not Manageable

In a healthy financial position, a single missed payment, due to an oversight or a busy period, is an inconvenience, a late fee, a quick correction, a minor dip in a credit score that recovers within months.

In a developing debt trap, a single missed payment often feels disproportionately catastrophic, because it threatens to trigger a cascade, penalty interest that makes an already tight month tighter, a missed payment on one account reducing the ability to pay another. This disproportionate sense of risk around a single payment is itself informative, it suggests the underlying financial cushion has already worn thin enough that there is very little room for even a small disruption.

What the Law Says

Under RBI's Fair Practices Code, lenders and their recovery agents are required to follow specific, defined conduct standards when contacting borrowers about overdue payments, including restrictions on calling hours and a prohibition on abusive or threatening language. Recognising the early signs described above, and acting on them before an account reaches serious overdue status, also has the practical benefit of keeping interactions with lenders in the earlier, less adversarial stages of the relationship, where restructuring and hardship options are typically more readily available than they are once an account has moved into recovery.

Talk to FREEDWhy Catching These Signs Early Matters So Much

The single most important fact about a debt trap is that the options available to address it narrow considerably the longer it continues unaddressed.

In the early stages, when only one or two of the signs above are present, options include restructuring an existing loan, transferring a high interest balance to a lower rate option, or simply committing to a disciplined repayment plan targeting the debt directly, often without needing any external program or service.

Once several signs are present simultaneously, particularly using one credit product to pay another and losing track of the total across accounts, the situation has typically progressed to a point where these lighter interventions are no longer sufficient on their own, and a more structured approach, consolidation or formal settlement, becomes the more realistic and effective path.

This is precisely why this blog focuses on early signs specifically, rather than only on severe, advanced debt distress. The earlier the pattern is recognised, the wider the range of genuinely effective options remains available.

The Solution: What to Do the Moment You Recognise These Signs

If one or two of the earlier, milder signs are present, minimum payments only, a balance that has not reached zero in several months, credit utilisation trending upward, the most effective immediate response is a direct, disciplined one: calculate the actual total owed across all accounts, identify the highest interest debt, and direct any available extra payment towards it specifically, while maintaining minimum payments elsewhere.

If the more advanced signs are present, using one credit product to pay another, difficulty tracking the total across accounts, a single missed payment feeling catastrophic, self directed repayment alone is less likely to be sufficient, and this is the point at which a structured, professional approach becomes genuinely more effective than continuing to manage it independently.

FREED's Debt Consolidation Program combines multiple debts into one lower interest loan with a single, manageable EMI, directly addressing the situation where multiple accounts and rising utilisation have made independent management increasingly difficult.

FREED's Debt Resolution Program negotiates a reduced settlement for debt that has progressed to a point where full repayment is not realistic, on average 56% less than the original outstanding.

A free, honest consultation can assess exactly which stage your specific situation is at, and recommend the path that fits it, before the trap has a chance to deepen further.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions