6 Reasons Why Your Credit Score Is Not Increasing

Paying on time every month but your CIBIL score is still stuck? You're not alone - and the reason is probably not what you think. Here are the 6 hidden reasons holding your score back and exactly what to do about each one.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

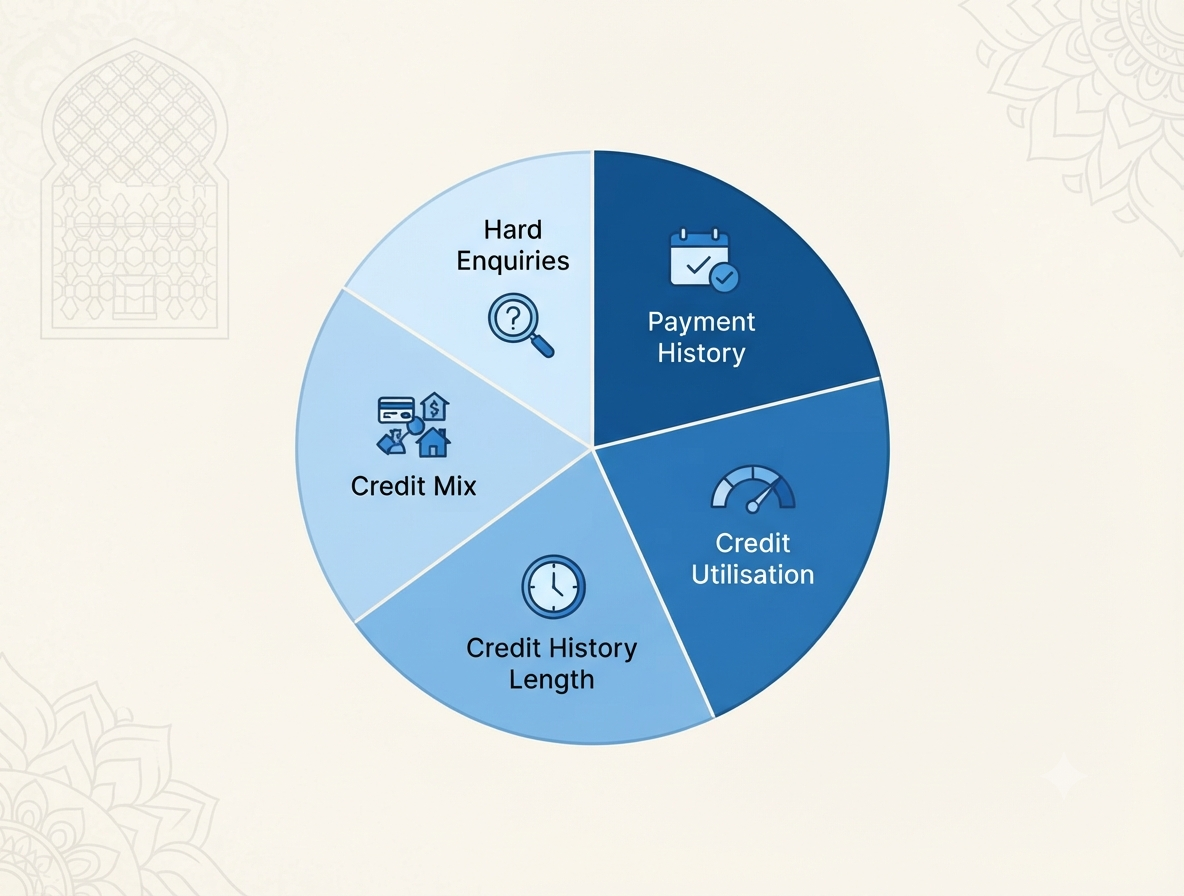

Paying on time is important but it's only 35% of your score. The other 65% comes from how much you owe, what type of credit you use, how long you've had it, and how often you apply for new credit.

Closing an old credit card or having only one type of credit can quietly drag your score down even if you've never missed a payment.

Errors on credit reports are very common and can silently pull your score down for months or years without you knowing.

Applying for multiple loans in a short time signals financial desperation to credit bureaus — and drops your score further.

If debt repayment is the underlying issue, FREED can help you address it so your score has a real chance to improve.

Why a Stuck Credit Score Is More Common Than You Think

According to CIBIL, the share of prime and higher-rated borrowers those with a score above 731 rose from 51% in June 2022 to 55% in June 2024. More Indians are taking their credit health seriously. Self-monitoring among borrowers went up by over 50% in FY24 alone.

But here's the frustrating reality many people face: you're doing the "right" things paying on time, not taking too many loans and yet your score just won't move.

The reason is almost always one of six hidden or misunderstood factors that quietly hold scores back. Most people fix the obvious things and miss these.

Let's go through each one clearly.

Reason 1: You're Paying on Time But Not the Full Amount

This is the most common one and the most misunderstood.

You pay your credit card bill before the due date every month. You think you're doing everything right. But if you're only paying the minimum due or leaving a balance your score is being quietly penalised.

Here's why.

Payment history is 35% of your CIBIL score. But credit utilisation how much of your credit limit you're using is 30%. Nearly as important.

When you carry a balance month after month, your outstanding is high relative to your limit. Your utilisation ratio stays elevated. And high utilisation tells credit bureaus that you are financially stretched even if you've never been late.

The fix: Always pay the full outstanding balance on your credit card not just the minimum. If you can't pay the full amount, pay as much above the minimum as possible and work towards bringing the outstanding down consistently.

The target: keep your credit card usage below 30% of your total limit. Below 10% is ideal if you're actively trying to improve your score.

Reason 2: You Closed an Old Credit Card

This one feels responsible. Fewer cards, fewer temptations, simpler life. But closing an old credit card, especially your oldest one can actually hurt your score.

Two things happen when you close a card:

Your credit history gets shorter. Length of credit history is 15% of your CIBIL score. The older your accounts and the longer you've managed credit well - the better your score. Closing your oldest card wipes out years of positive history from your active profile.

Your total available limit drops and utilisation rises. If your closed card had a ₹50,000 limit and you had ₹20,000 outstanding on another card with a ₹60,000 limit before closing, your combined utilisation was ₹20,000 ÷ ₹1,10,000 = 18%. After closing, it becomes ₹20,000 ÷ ₹60,000 = 33%. Your spending didn't change. But your score dropped.

The fix: Keep old credit cards open, especially those with no annual fee or significant outstanding. Use them for one small, planned purchase every 2–3 months. Pay in full. Let them quietly support your score.

The only valid reason to close a card is a high annual fee that genuinely isn't worth it.

Reason 3: You Only Use One Type of Credit

If your entire credit history is just one credit card and that's it your score may plateau even if you manage it perfectly.

Credit scoring models reward a mix of credit types. This is called credit mix and it's 10% of your CIBIL score.

Having both secured loans and unsecured credit (credit card, personal loan) shows lenders that you can responsibly manage different kinds of financial obligations. It signals financial maturity.

If your entire history is one product a single credit card the bureau has limited data to work with. Your score reflects responsible behaviour but lacks the breadth that a diverse credit profile shows.

The fix: You don't need to take loans just to improve this. But if you already need a loan, an FD-backed loan, a gold loan, or a two-wheeler loan, managing it responsibly adds to your credit mix and helps your score over time.

Never take a loan solely for the credit mix benefit. The cost of the loan must make sense for another reason.

FREED Expert Tip

If you want to improve your credit mix without taking a large loan — consider a secured credit card backed by a fixed deposit. It gives you active credit to manage and builds a track record of responsible credit use. Many banks offer these against FDs starting from ₹10,000. This is one of the easiest and cheapest ways to diversify your credit profile.

Talk to FREEDReason 4: You Don't Have Enough Credit Activity

This one feels deeply unfair. You're careful. You barely borrow. You've never defaulted. And your score is still low.

Why? Because the credit scoring system runs on data. If there is not enough recent credit activity, active EMIs, regular credit card usage, consistent repayments, there is not enough for the algorithm to judge you on.

A thin credit file with very low activity looks uncertain to lenders. They can't tell if you're responsible because there isn't enough data showing how you behave.

This is especially common among:

People who just started using credit

People who paid off all loans and stopped borrowing completely

People who use only debit cards and never credit

The fix: Use credit but use it responsibly. A secured credit card is the safest way to build credit activity without risk. Use it for one small planned purchase monthly. Pay the full bill. Keep utilisation low. After 6–12 months of this, your score will start responding.

As per updated RBI guidelines effective 2025, credit bureaus now update your data every 15 days. This means the positive impact of new responsible activity shows up faster than it used to.

Reason 5: There Are Errors on Your Credit Report

This is one of the most damaging and most overlooked reasons for a stuck or falling credit score.

Errors on credit reports are far more common than most people realise. A CIBIL study found that disputes were raised on millions of records, many involving incorrect payment statuses, wrong outstanding amounts, or accounts that were closed but still showing as active.

Common errors that silently drag your score:

A payment you made on time: showing as "missed" or "late"

A loan that is fully closed, still showing as "active"

An account you never took linked to your PAN (possible fraud)

Wrong personal details - name, PAN, date of birth, causing data mismatches

Every error that goes unfixed is silently pulling your score down and you're doing nothing wrong. The system is wrong.

The fix: Check your credit report from all four bureaus -

CIBIL (cibil.com), Experian (experian.in), Equifax (equifax.co.in), and CRIF High Mark (crifhighmark.com) once every 3 months. Each gives you one free report per year.

When you find an error, raise an online dispute with the bureau immediately. It is free. Under the Credit Information Companies (Regulation) Act, 2005, they must investigate and respond within 30 days.

One corrected error can improve your score immediately - without any other change in your behaviour.

What the Law Says

Under the Credit Information Companies (Regulation) Act, 2005, every Indian citizen has the legal right to dispute incorrect information on their credit report. Credit bureaus are legally required to investigate the dispute and respond within 30 days. If the error is confirmed - it must be corrected and your score updated. This process is completely free. If a bureau fails to respond within 30 days - you can escalate to the RBI Banking Ombudsman at cms.rbi.org.in.

Talk to FREEDReason 6: You're Applying for Too Many Loans at Once

You want a better deal. You apply to multiple banks to compare rates. Seems smart. But it can backfire badly on your credit score.

Every time you apply for a loan or credit card, the lender does a "hard inquiry" on your credit report. This temporarily drops your score by 5–10 points. One inquiry is fine. Two is manageable. But five hard inquiries in one month? That is a red flag.

To a credit bureau - multiple applications in a short period look like you are desperately searching for credit. It signals financial stress. Your score drops. And the very reason you were shopping to get better rates - becomes harder because your score is now lower.

The fix: Space out loan applications by at least 3–6 months. Before applying - use soft-check eligibility tools that don't affect your score to understand which lenders are likely to approve you. Apply only to one lender at a time.

If you are shopping for a specific product - like a home loan or car loan - multiple enquiries within a 14-30 day window are often treated as a single inquiry by bureaus. But for different product types applied simultaneously - each inquiry counts separately.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Why Your Credit Score Matters More Than Ever in 2026

Credit access in India is expanding rapidly. According to TransUnion CIBIL, credit penetration among Indian adults has been growing steadily across all age groups between December 2021 and December 2024:

Age 18–25: Penetration rose from 9% to 15%

Age 25–35: Jumped from 22% to 32%

Age 35–45: Increased from 26% to 35%

More people are entering the credit system. More people are applying for home loans, car loans, credit cards, and BNPL (Buy Now, Pay Later) schemes.

In this environment, your credit score is not just a number. It is your competitive edge. It determines whether you get approved, how much you can borrow, and what interest rate you pay.

The difference between a 700 score and a 750 score on a ₹20 lakh home loan can mean ₹50,000–₹1,00,000 in extra interest over the loan tenure. That's real money.

Understanding why your score is stuck and fixing it, is one of the most practical financial investments you can make right now.

What If Debt Is the Real Reason Your Score Is Stuck?

Sometimes - no amount of tip-following will meaningfully improve your score if the underlying debt load is the problem.

If your credit card outstanding is consistently high because you can't afford to pay it down, your utilisation will stay high and your score will stay stuck. If you have multiple loans and the EMIs are consuming most of your income, the system sees financial stress, not responsibility.

In these situations, the right step is not just better credit habits. It's addressing the debt itself.

If multiple EMIs are overwhelming - Debt Consolidation. FREED's Debt Consolidation Program combines all your loans into one lower monthly payment. Your outstanding reduces faster. Your utilisation improves. Your score has room to recover.

If you've already defaulted and can't repay the full amount - Debt Resolution. FREED's Debt Resolution Program negotiates with your lenders to settle for less than you owe. On average, clients settle at 56% less than the original outstanding. The accounts are closed. The score stops being pulled down by active defaults.

Both programs include FREED Shield protection from recovery harassment - trusted by over 15,00,000 Indians.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions